Published on 07 May 2026

Family trust vs company bookkeeping and distribution records differ significantly in how you document income allocations, maintain compliance records, and manage ongoing reporting obligations. Understanding these differences helps you choose the right structure for protecting family assets while meeting your wealth management goals.

What is a Family Trust?

A family trust is a legal arrangement where a trustee manages assets for beneficiaries, usually family members. The trust deed sets out who can receive benefits, how income gets distributed, and what the trustee can do. This lets you distribute income flexibly among family members while keeping control of the assets.

The discretionary trust structure allows trustees to decide each year how much income each beneficiary receives, based on their individual circumstances and tax positions. Many Australian families use this arrangement for running a family business, holding investments, or managing property, as it combines asset protection with tax planning opportunities that benefit multiple generations. Some trusts may also make a family trust election, which locks in a specific family group eligible to receive distributions and affects how certain tax rules apply.

Struggling to get family trust resolutions signed by 30 June?

Schedule a complimentary consultation with us today to set up clear processes and on‑time distribution minutes.

What Are the Core Differences Between Trust and Company Structures?

A family trust (also called a discretionary trust) operates as a legal relationship where a trustee holds assets and income for beneficiaries. This popular structure among many Australian families allows flexible income distribution to family members while keeping family control over assets. Companies exist as separate legal entities owning assets in their own right, providing different asset protection benefits.

In a discretionary family trust, the trustee generally makes valid resolutions by 30 June to appoint or distribute trust income to beneficiaries, who are then assessed on their share of trust income at their individual marginal tax rates. Companies that qualify as base rate entities generally pay tax at 25%, while companies that do not qualify for the lower company tax rate generally pay tax at 30%. Companies can retain profits after paying tax. These differences create distinct bookkeeping obligations around distribution minutes, beneficiary records, and annual tax returns.

How Do Distribution Records Differ for Family Trusts?

Family trusts generally require valid trustee resolutions to be made by 30 June each financial year, documenting how the trust’s income will be appointed or distributed. The trust deed establishes strict rules around who can receive distributions and how decisions get made. These minutes must identify each beneficiary receiving distributions, specify amounts allocated, and confirm Tax File Number collection to avoid withholding obligations.

Written records prevent disputes and provide evidence during ATO reviews requested as early as the first week of July. Failing to make valid resolutions by 30 June can result in the trustee being assessed on trust income at the highest marginal tax rate plus Medicare levy, currently 47%. Your trustee or trustees need systems ensuring timely preparation and proper documentation of all trust distributions.

Essential elements your distribution minutes must include:

Names of all beneficiaries receiving distributions, with Tax File Number (TFN) details collected and recorded securely where the closely held trust TFN withholding rules apply.

Specific dollar amounts or percentages allocated to each person

Date of the trustee resolution (on or before 30 June)

Trustee signatures confirming distribution decisions

Details of any Capital Gains Tax or franking credits streamed to specific beneficiaries

What Distribution Records Do Companies Need to Maintain?

Companies prepare formal dividend resolutions when declaring dividends to shareholders. These resolutions require director approval specifying the dividend amount per share, eligible shares, payment date, and record date. Unlike the Australian family trust structure requiring annual distributions, companies have flexibility timing dividend payments and can retain profits for business interests.

Each shareholder receives a dividend voucher serving as their payment receipt, essential for completing annual tax returns. These simpler distribution requirements mean less time pressure compared to the strict 30 June deadline family trusts face. However, companies must maintain permanent records and pay annual ASIC fees, adding to ongoing costs.

Understanding Ongoing Bookkeeping Obligations for Family Trusts

Trustees maintain accurate records for each beneficiary and keep all relevant documents for at least five years, typically using robust bookkeeping systems and services to manage growing volumes of financial data. Beyond distribution minutes, you need copies of your trust deed, all trustee resolutions, detailed statements showing trust assets and liabilities, and current trustee contact details. This documentation proves the trust structure operates according to its legal document requirements.

The trustee lodges annual trust tax returns and provides each beneficiary with distribution statements used to complete their own income tax obligations, which will later be reflected in their ATO Notice of Assessment. The beneficiaries pay tax on their share of trust income at their marginal rate, which can mean significant tax advantages when distributions go to family members in lower tax brackets. Your tax agent needs these records to prepare accurate returns and maximise tax effectiveness.

What Are Company Bookkeeping Compliance Requirements?

Companies maintain written financial records accurately explaining transactions, financial position, and performance under the Corporations Act 2001. These records enable preparation of true and fair financial statements. Companies lodge annual company tax returns, maintain current registers, and pay annual ASIC fees around $310 for standard proprietary companies.

Records can be kept electronically if accessible to the ATO, but you must produce hard copies when requested and regularly back up important documents. The seven-year retention period for company financial records exceeds the five years required for family trusts.

How Do Tax File Number Requirements Differ?

Family trusts face specific withholding obligations when beneficiaries fail to provide Tax File Numbers. For closely held trusts, if a beneficiary does not quote their TFN before receiving a payment or becoming presently entitled to an unpaid amount, the trustee may need to withhold tax at the highest marginal rate plus Medicare levy. Where TFNs are quoted, the trustee must lodge a TFN report for the relevant quarter by the last day of the following month, and any withheld amounts must be reported through the required annual TFN withholding reporting process. This makes TFN collection critical for tax purposes and keeping beneficiaries from paying unnecessary tax.

Companies collect TFNs from shareholders primarily for dividend payments, but withholding obligations differ. Companies paying unfranked dividends to shareholders without TFNs may need to withhold at specific rates, though fully franked dividends typically don’t trigger requirements. Trust TFN withholding applies to all distributions regardless of the trust’s tax position, and some family groups may instead use unit trust structures with different tax rules where investors hold fixed entitlements.

Why Capital Gains Tax Treatment Creates Different Record Requirements

Family trusts may be eligible for the 50% Capital Gains Tax (CGT) discount on eligible assets held for at least 12 months, and should maintain detailed records showing acquisition dates, cost bases, capital losses, and disposal proceeds to correctly apply rules such as the 6-year main residence CGT rule where relevant. When a trust realises a $200,000 capital gain, the discount reduces taxable income to $100,000, distributed among beneficiaries at their marginal tax rates for significant tax benefits compared to companies, particularly when combined with small business CGT concessions.

Companies cannot access the 50% CGT discount and include the full capital gain in taxable income at the corporate rate. This means family trust bookkeeping systems track income and capital transactions more meticulously to maximise tax advantages. Streaming capital gains to specific beneficiaries requires additional documentation in distribution minutes showing the trustee’s intention to allocate gains separately.

We’re more than bookkeeping experts

As part of ACT Tax Group, we offer complete accounting and business advisory services tailored to your needs.

Managing Profit Retention and Future Planning

Family trusts commonly make annual resolutions to appoint income to beneficiaries, so the trustee is not assessed at the highest marginal tax rate plus Medicare levy, currently 47%. Trustees should also distinguish between trust income and capital amounts when considering what can be retained within the trust. Your bookkeeping clearly separates capital (which can be retained) from income (which must be distributed), requiring careful classification throughout the financial year. This affects succession planning as trust assets eventually reach a vesting date when the trust must wind up or continue under different terms.

Companies enjoy greater flexibility retaining profits after paying the 25% corporate rate, allowing reinvestment for business growth. This benefits business interests requiring capital accumulation and provides asset protection through the separate legal entity structure. However, companies face different challenges around accessing funds personally, as profits must be formally distributed as dividends triggering additional tax at individual marginal rates, or structured carefully through Division 7A compliant loans to avoid deemed dividends.

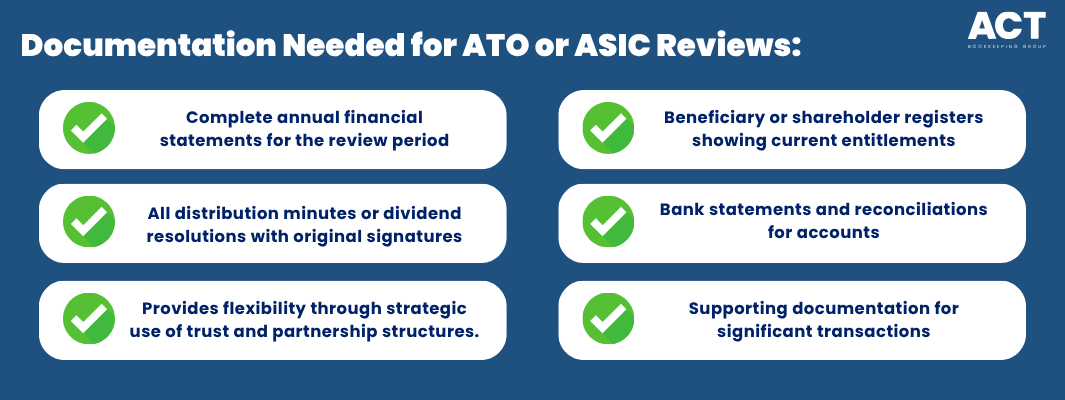

What Happens During ATO Audits and Reviews?

The ATO requests copies of distribution minutes for review as early as the first week of July. Trustees produce all books relating to trust administration, with records maintained so processes and decisions are readily traceable. The person responsible for record-keeping faces serious consequences when documentation is inadequate or missing.

Companies face ASIC and ATO reviews requiring access to financial records, director resolutions, shareholder registers, and annual financial statements, and may at times need to negotiate or manage ATO payment plans for overdue BAS obligations if cash flow becomes tight. Directors carry personal liability for record-keeping failures under the Corporations Act. The five-year retention period for trusts extends to seven years for company financial records.

Choosing the Right Structure for Your Needs

Your ability to maintain detailed, timely records should influence your structure choice. Family trusts demand meticulous record-keeping around beneficiary distributions, Tax File Number collection, and annual resolution preparation within strict 30 June deadlines. Many Australian families choose this structure for tax planning flexibility and the ability to protect assets while distributing income to family members in lower tax brackets.

Companies require ongoing compliance with ASIC regulations, higher ongoing costs, and more extensive financial record retention, but offer simpler profit distribution documentation since dividends can be declared anytime. Set up costs also differ, with family trusts typically requiring more comprehensive legal documentation through the trust deed, while companies involve corporate trustee appointments and ASIC registration.

Consider getting advice from a professional adviser or tax agent who understands your specific situation. A properly structured family trust offers tax benefits through income splitting and Capital Gains Tax advantages, while companies provide stronger asset protection and simpler profit retention for business interests. The family control test, potential benefits for future generations, and how you plan to hold assets all factor into which structure works best for your family business or investments.