Published on 30 Apr 2026

Discretionary trust bookkeeping basics: how to record capital and income distributions in your ledger starts with understanding how a discretionary trust works and how the trustee decides to allocate funds to different beneficiaries. When you clearly separate income and capital in your records, your trust income, capital gains and cash movements are easier to follow at the end of each financial year. This helps support clearer trust administration, tax planning and record keeping for family or business structures.

Why Clear Records Matter for Discretionary Trusts

In Australia, a typical family discretionary trust is a legal arrangement where a trustee holds trust property for the benefit of trust beneficiaries. The trust deed sets the rules, and the trustee or trustees manage the trust fund, trust assets and income of the trust in line with those rules. When the trustee exercises their discretion to distribute income and capital, your ledger needs to show who received what and when, as well as any unpaid amounts that remain in the trust.

The good news is that with the right trust structure and a clear chart of accounts, you can record income distribution and capital distribution in a consistent and practical way. You do not need complex language or special software to get the basics right, just clear accounts, an understanding of different types of bookkeeping systems and reliable bookkeeping steps. In this guide, we explain what a discretionary trust is in simple terms, then walk through how to record income and capital distributions for your own family trust or business trust.

Worried your unpaid beneficiary balances could trigger Division 7A issues?

Schedule a complimentary consultation with us today to check UPEs, corporate beneficiary loans and minimise Division 7A risk.

What Is a Discretionary Trust and Why Does It Matter for Bookkeeping?

A discretionary trust, often called a family trust, is a legal arrangement where a trustee holds trust assets for a group of beneficiaries who do not have fixed rights to income or capital. Each financial year, the trustee decides how to distribute income and capital under the terms of the trust deed. Your bookkeeping needs to follow these yearly decisions, rather than a set pattern, so the records match what the trustee has actually decided.

In many family businesses, the trustee is a company (a corporate trustee), which acts as the legal owner of the assets held in the trust. The trust itself is not a separate legal entity in the same way as a company, but for tax purposes it is treated as a separate trust structure with its own tax obligations. For bookkeeping, that means you record income derived, expenses, assets and distributions in the trust ledger as if the trust was its own set of books, separate from personal assets of family members.

Why Does the Trust Deed and Trustee’s Discretion Matter in Your Ledger?

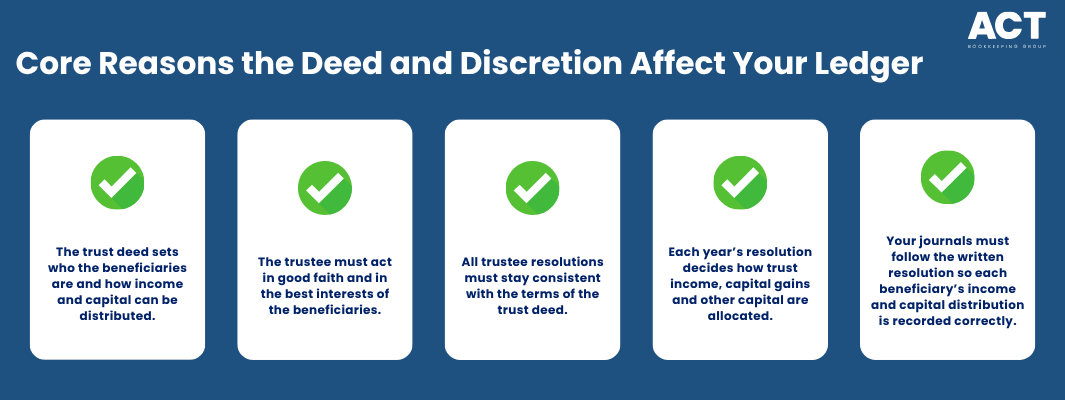

The trust deed is the key legal document that sets out how the trustee holds property, who the primary beneficiaries and general beneficiaries are, and how income and capital can be distributed. When the trustee exercises their discretion, they must act in good faith and in the best interests of the beneficiaries generally, and their resolutions must be consistent with the trust deed. Your bookkeeping must reflect such action, matched to the wording in the deed and any later variations.

Each financial year, the trustee decides how to distribute income of the trust and, where allowed, capital gains and other capital. This decision is usually recorded in a written resolution or minute that sets out how to distribute income and capital distribution between individual beneficiaries, a corporate beneficiary or other eligible family members. Once the trustee decides, your journals should follow that resolution, showing the income distribution and capital distribution amounts for each beneficiary.

How Should You Separate Income and Capital in a Discretionary Trust Ledger?

In a discretionary trust structure, income and capital serve different purposes and should not be mixed in one catch‑all account. Trust income generally includes business profits, rent, interest and dividends, while capital can include capital gains on sale of investments and other trust property. Some trust deeds treat certain capital gains as part of trust income for distribution purposes, so always check how the deed defines net income and distributable amounts.

In your ledger, it is helpful to keep separate accounts for income distribution and capital distribution so you can see clearly how much of the benefit each beneficiary receives is income and how much is capital. This matters for capital gains tax, tax benefits and future estate planning or succession planning, as past capital gains and other capital amounts can be distributed later. Clear separation of income and capital also makes it easier to answer questions such as “what is a discretionary trust actually paying to each person this year?” without digging through every transaction.

How Do You Set Up a Chart of Accounts for a Discretionary or Family Trust?

A trust that manages assets for a family or business group needs a chart of accounts that supports both everyday transactions and end‑of‑year distributions. At a minimum, you will want income accounts for trading income, rent, interest, dividends and other income derived, plus expense accounts, a bank account, equity accounts and beneficiary accounts. Equity accounts often include settled sum, capital profits reserve, retained earnings and other accounts that track movements in trust assets and capital.

For each beneficiary, we recommend setting up separate ledger accounts to track allocations and unpaid balances, for example: “Income Distribution – [Beneficiary Name]” and “Unpaid Distribution/Loan – [Beneficiary Name]”. Where a corporate beneficiary is used as part of a tax effective structure, you would add similar accounts in that name. This layout gives you a clear view of how the trustee holds and allocates funds to each person or company and supports later reporting on family assets and tax obligations.

How Do You Turn the Trustee’s Resolution into Practical Journal Entries?

Once the financial year ends and the accounts are ready, the trustee passes a resolution that sets out how to distribute income and capital. This resolution might say, for example, that 40% of trust income goes to one beneficiary and 40% to another, and may separately deal with capital gains if the trust deed allows streaming and the beneficiary is made specifically entitled. Your first step is to calculate the dollar amounts for each beneficiary based on the trust deed, distributable income, taxable net income and any capital gains or franked distributions that have been specifically dealt with.

After you know the actual figures, you record journals to move trust income and capital from profit and loss into the relevant beneficiary accounts. This usually means debiting a “profit appropriation” or similar account and crediting “unpaid distribution – [Beneficiary]” or “beneficiary loan – [Beneficiary]” if the funds remain in the trust fund. If some or all of the amounts are actually paid out to a bank account of the beneficiary, you instead credit the trust bank account and reduce the unpaid balance.

What Are the Basic Income Distribution Journal Entries?

Income distribution journals move the net income amount from the trust’s profit accounts into beneficiary accounts. A simple pattern is to debit a “current year earnings” or “profit appropriation” account for the total income of the trust, then credit each beneficiary’s unpaid distribution account based on the trustee’s resolution. This shows that the trustee has allocated that income in the ledger, but the tax outcome still depends on the trust deed, the trustee resolution, present entitlement and the relevant trust tax rules.

If the trustee decides to pay some or all of the income to beneficiaries during the year or shortly after year‑end, you post a second journal to debit their unpaid distribution account and credit the trust bank account. This ensures that the ledger shows both the trustee’s decision to distribute income, and the later cash movement out of the assets of the trust. The same approach applies whether the beneficiary is one beneficiary, several family members or a corporate beneficiary.

How Do You Record Capital Gains and Capital Distributions?

Capital gains may arise when the trust sells assets such as investment property or shares. If a beneficiary is specifically entitled to a trust capital gain, the gain is generally taken into account in working out that beneficiary’s net capital gain. In your accounts, you record the capital gains in separate income accounts so they can be identified for tax purposes and later capital distribution. Whether these gains are treated as income or capital for distribution depends on the trust deed and the way the trustee structure is used in practice.

If capital gains form part of trust income, the resolution and ledger should clearly identify the capital gain component and any specific entitlement. Capital gains that are not specifically entitled are generally allocated proportionately based on beneficiaries’ present entitlements to trust income. If capital gains are treated as capital, you may choose to move amounts from a capital profits reserve or similar equity account to each beneficiary’s capital distribution account. This helps track how capital gains and other capital amounts have been applied over time, which is valuable for estate planning, succession planning and managing family assets.

How Do Discretionary Trusts Support Asset Protection and Estate Planning?

One of the key advantages of a family discretionary trust is asset protection, when used and managed correctly. Because the trustee holds property as legal owner for beneficiaries, there may be a level of separation between personal assets and assets held in the trust, depending on the deed, control arrangements, guarantees, loans and how the trust is managed. This can help protect trust assets from certain personal claims, although the trustee may be personally liable if they act outside the deed or the law.

Discretionary trusts can also support estate planning and succession planning by helping control of trust decisions pass to the next generation. Any change of trustee, appointor, control or underlying ownership should be reviewed carefully for tax, duty and legal consequences before action is taken. For example, changing control of a trustee company or appointor can allow control to pass on from a deceased estate to family members, while the assets stay in the trust. Because these areas are complex and depend on personal circumstances, it is important to seek professional advice before making changes.

We’re more than bookkeeping experts

As part of ACT Tax Group, we offer complete accounting and business advisory services tailored to your needs.

How Do Tax Planning and Tax Benefits Affect Distribution Decisions?

A major reason people choose a discretionary trust structure is the flexibility to distribute income and capital across several beneficiaries each financial year. By distributing trust income and capital gains to eligible beneficiaries in line with the trust deed and tax law, a trust may improve tax efficiency, but trustees must consider present entitlement, Section 100A risk, family trust election rules and the real benefit provided to beneficiaries. Using a corporate beneficiary may help manage tax outcomes in some structures, but unpaid present entitlements can raise Division 7A issues and the applicable company tax rate depends on whether the company qualifies as a base rate entity.

For tax purposes, the way you distribute income and capital must align with the trust deed, tax laws and the real flow of benefits. It is not enough to record an income distribution if the arrangement does not reflect the trustee resolution, present entitlement, beneficiary benefit and relevant anti-avoidance rules, including Section 100A where applicable. Because the rules around capital gains tax, trust income definitions and corporate beneficiary arrangements can be detailed, it is wise to seek professional advice before relying on a tax effective structure.

What Practical Steps Should You Follow Each Financial Year?

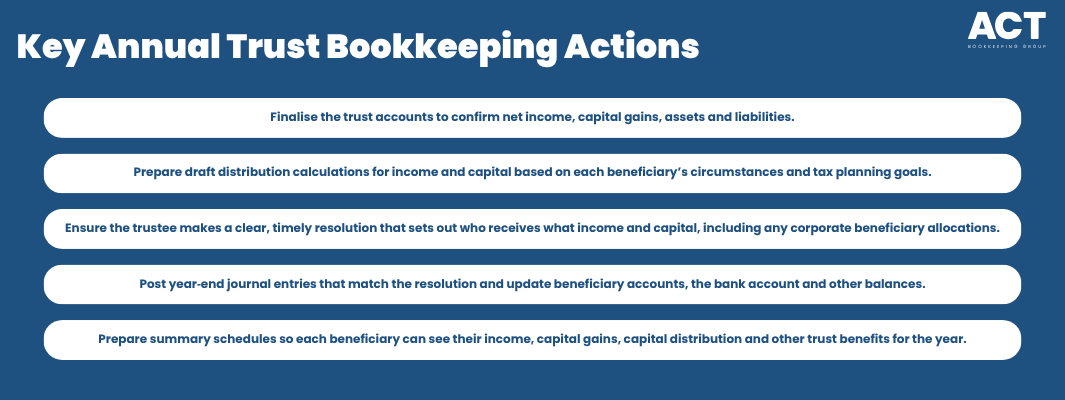

To keep your discretionary trust bookkeeping clean and compliant, it helps to follow the same steps each year. First, finalise the trust accounts so you know the net income, any capital gains and the position of the assets held and liabilities, supported by organised record keeping for tax compliance. Second, prepare draft distribution calculations that show how you plan to distribute income and capital, considering the personal circumstances of each beneficiary and your broader tax planning and asset protection goals.

Third, support the trustee or trustees to make a clear resolution by the required time that sets out who will receive what income and capital, including any allocations to a corporate beneficiary where allowed. A corporate trustee should not be confused with a corporate beneficiary. Fourth, post year‑end journal entries that reflect the resolution, moving trust income and capital into beneficiary accounts and updating the bank account and other asset balances as needed. Finally, prepare summary schedules for each beneficiary so they understand their share of income, capital gains, capital distribution and other trust benefits for the year.

Why Is Expert Advice So Important for Discretionary Trust Distributions?

Although the bookkeeping entries for a discretionary trust can be explained in simple terms, the underlying trust structure, tax rules and asset protection issues are complex. Getting income and capital distribution wrong can affect tax outcomes, expose personal assets and cause disputes between family members or other beneficiaries. It can also create problems if the trust is later involved in a legal dispute or forms part of a deceased estate.

That is why it is strongly recommended to seek professional advice from a bookkeeping and tax team that understands how discretionary trusts, family businesses and estate planning fit together. An experienced adviser can help you design the right chart of accounts, match journals to trustee resolutions, and make sure your records support both day‑to‑day management and longer‑term goals. With the right support, your trust can manage assets, distribute income and protect family wealth in a calm and organised way, year after year.