Published on 18 Jun 2026

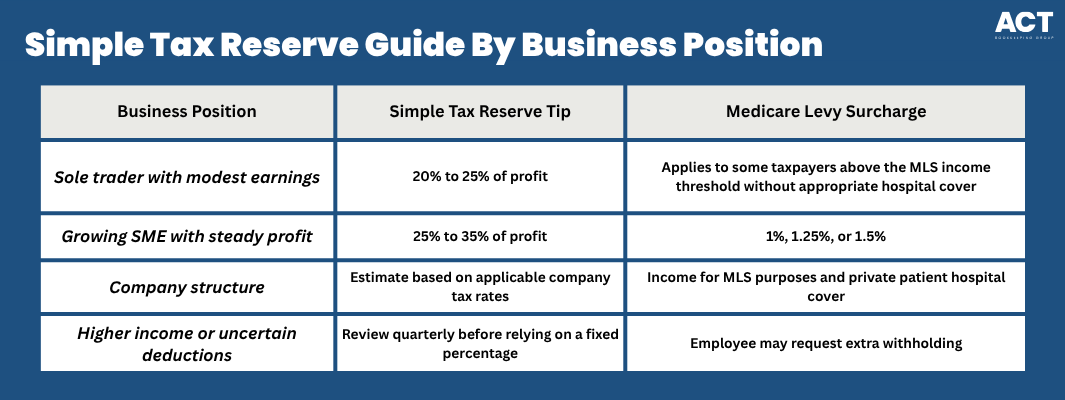

How much percent is tax is one of the first questions Australian Small and Medium Enterprises (SMEs) ask when business income starts to grow. As a simple planning rule, many SMEs should consider setting aside 25% to 35% of estimated taxable profit for income tax, plus a separate amount for net Goods and Services Tax (GST) that may be payable if the business is GST registered. This percentage is only a guide for illustrative purposes because tax payable is calculated based on your structure, income, deductions, tax rates, and circumstances.

What Percentage of Business Income Should Go to Tax?

Most SMEs should start by estimating tax on profit, not total income. Profit is what remains after business expenses and allowable deductions are taken into account for tax purposes. For companies, tax rates are usually easier to estimate than for individuals because company tax is calculated at the applicable company rate. For sole traders, personal income tax rates, resident tax rates, tax brackets, the tax-free threshold, the Medicare levy, the Medicare levy surcharge, and tax offsets can all affect how much tax is payable.

Unsure how much tax to set aside?

Schedule a complimentary consultation with us today to estimate your correct tax percentage.

Profit Is the Number That Matters

Business income is not the same as taxable income. Taxable income is generally calculated after business expenses, tax deductions, and other allowable claims are considered.

Example:

If your business receives $300,000 in income and has $190,000 in deductible business expenses, the starting point for tax planning is closer to $110,000, not $300,000. The final taxable income tax outcome may still change depending on your structure, timing, deductions, and whether certain expenses are allowed.

Sole Traders Need to Think Like Individuals

Sole traders pay personal income tax on business profit because the business income forms part of their individual tax return. This means the marginal tax rate can increase as earnings rise. Australian residents may also be entitled to the tax-free threshold and, in some cases, the low-income tax offset. However, a low-income tax offset does not mean tax will always be nil, and it should not be relied on without checking your full income, work related expenses, salary, wages, allowances, and other factors.

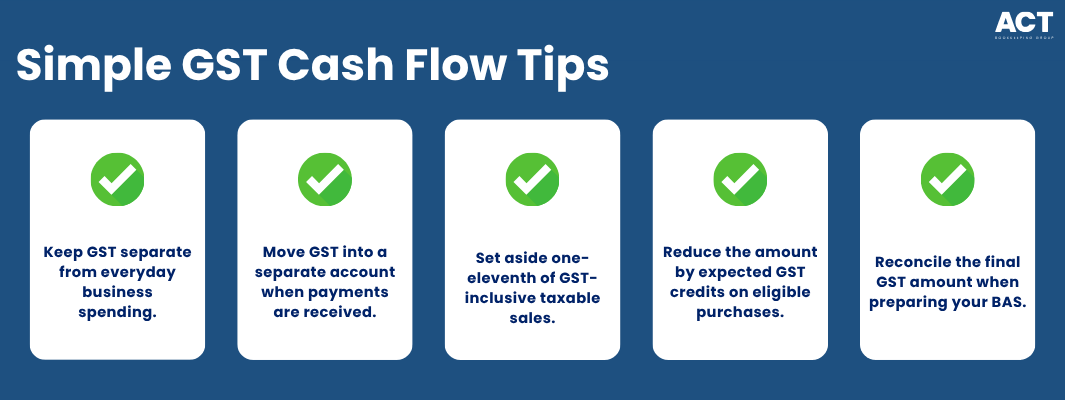

GST Should Be Kept in a Separate Account

If your business is registered for GST, the GST collected from customers should not be treated as available spending money. It is better to move that amount into a separate account as payments are received. A practical tip is to set aside one-eleventh of GST-inclusive taxable sales, less GST credits you expect to claim on eligible business purchases, then reconcile the final amount when preparing the BAS. This helps with managing tax affairs because GST, PAYG withholding, and income tax can otherwise become mixed with operating money.

ATO Instalments Can Affect Cash Flow

Pay As You Go (PAYG) instalments can help taxpayers spread income tax across the year. They are not an extra tax, but advance payments towards the expected tax payable for the year. If your income changes, the instalment amount may need to be reviewed. Understanding how the PAYG instalment system works can help you decide when to vary instalments, because underestimating tax may leave you with extra tax to pay and could result in general interest charge or later cash flow pressure.

How A Tax Calculator Can Help

A tax calculator, income tax calculator, or calculator on the ATO website can help you estimate tax for individuals, especially where salary, wages, resident status, tax brackets, and Medicare levy settings apply. These tools can be useful for planning, but they do not replace advice. For SMEs, even a detailed income tax calculation guide for Australians may not fully capture business structure, timing differences, appropriate private patient hospital cover for Medicare levy surcharge purposes, superannuation contributions, charitable donations, business expenses, and deductions. Use calculator results as a guide only, then seek further information before making decisions that affect your tax affairs.

Tax Deductions Can Reduce Tax Payable

Tax deductions can reduce taxable income when they are directly connected to earning business income and supported by records. Common examples include software costs, accounting fees, vehicle expenses, insurance, supplies, and the business portion of home-based business expenses where the claim is applicable and supported by records.

Do Not Compare Your Tax Percentage to Another Business

Two businesses can earn the same dollar amount but pay different tax because their costs, structure, employer obligations, deductions, and owners’ personal circumstances are different. One may have employees, wages, superannuation, and PAYG withholding, while another may have fewer costs but higher profit.

We’re more than bookkeeping experts

As part of ACT Tax Group, we offer complete accounting and business advisory services tailored to your needs.

How ACT Bookkeeping Can Help with Business Tax Planning

ACT Bookkeeping helps SMEs in Canberra and across Australia manage tax affairs with clear, practical advice. We can review your income, taxable income, deductions, GST, PAYG instalments, business expenses, and expected tax payable so your tax reserve percentage is based on your actual position. You can arrange a consultation with our team to review how much tax your business should set aside, whether your current system is working, and what records you need to keep. Our goal is to reduce stress, support compliance, and help you make confident decisions with money that is truly available.

Keeping Your Tax Planning Simple

A simple tax rule is a starting point, not a final answer. For many SMEs, setting aside 25% to 35% of profit for income tax, plus separating GST, creates a safer and clearer cash flow system. Review your percentage each quarter, especially when income rises, expenses fall, tax rates change, or new obligations are announced. With organised records, practical tips, and timely advice, tax becomes easier to plan for and less likely to interrupt business growth.