Published on 14 May 2026

Setting up a family trust for your business: what your bookkeeping system must track is the key to getting the real benefits of this trust structure without creating future tax or compliance headaches. When a family trust is not supported by accurate records, even a well‑drafted trust deed cannot fix poor trust administration or missing paperwork. A clear, practical bookkeeping system helps your trustee stay on top of the trust’s tax affairs while protecting your business and family members.

What Is a Trust and Why Bookkeeping Matters from the Start

A family trust is commonly a discretionary trust created by a formal trust deed, where a trustee holds trust assets such as business assets or other assets for the benefit of a defined group of beneficiaries. For tax purposes, the ATO generally treats a trust as a family trust only where a valid family trust election has been made. In simple terms, a trust is a legal relationship, not a separate legal entity like a company, even though the trustee carries the legal title to the trust property. When the trust is set up and administered correctly, it may support asset protection and tax planning outcomes, subject to the trust deed, trustee conduct, tax law, anti-avoidance rules and the beneficiaries’ tax positions.

Struggling to keep trust records ATO‑ready?

Schedule a complimentary consultation with us today to set up compliant trust bookkeeping systems.

Understanding The Family Trust Structure for Your Business

A family trust is commonly used as a business structure where a person or a company acts as trustee and holds property, funds and income on trust for family members. The trustee holds legal ownership of the trust property, but the beneficiaries enjoy the benefit of income and capital according to the terms of the written document that created the trust. Unlike a sole trader, the person holding the assets as trustee is legally responsible for managing the trust under trust law and tax law.

This type of inter vivos trust is usually established during a person’s lifetime under a formal trust deed, rather than arising as a deceased estate or testamentary trusts that start on death. Once the trust is established, the trustee decides how to operate the business, manage assets and make trust distributions within the discretionary powers set out in the trust instrument. Your bookkeeping system must reflect this trust structure by clearly separating trust assets, funds and income from any personal or company affairs, and cloud‑based tools can make it easier to maintain real‑time, accurate bookkeeping records that support this separation.

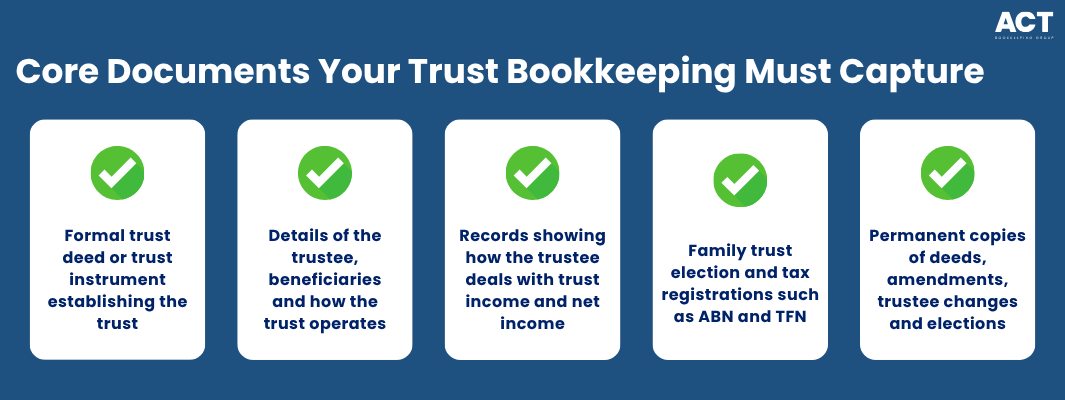

Key Documents Your Bookkeeping System Must Support

Before any transactions occur, the trust must be set up with a formal trust deed or similar legal document that explains who the trustee is, who the beneficiaries are and how the trust operates. This document is often called the trust instrument, and it governs how the trustee holds property, makes decisions and deals with trust income and net income. Your bookkeeping records should always be consistent with this document, because it defines what the trustee is allowed to do.

When a trust is created, the trustee may apply for a TFN for the trust and, if the trust carries on an enterprise, an ABN in the trustee’s capacity as trustee. A family trust election should only be made where appropriate, because it can provide access to certain tax concessions but may also expose the trustee to family trust distribution tax if distributions are made outside the family group. All of these steps create legal obligations, and they should be stored with the trust’s core records, so they are easy to find when you prepare accounts or tax returns. Your system should keep permanent copies of the trust deed, any amendments, trustee appointment documents and elections so that you can always show how and when the trust was established, much like a sole trader must follow a disciplined record keeping guide for tax compliance.

Separating Business Assets and Trust Assets

In a family trust that operates a business, the bookkeeping file must clearly show which assets belong to the trust and which assets belong to individuals or any company in the group. The trustee holds legal title to trust assets and business assets on behalf of beneficiaries, so combining personal and trust transactions in one bank account makes it hard to prove who owns what. Clear separation makes it easier to show that the trust, not a natural person, holds property, income and funds for the benefit of others.

Your bookkeeping system should track each asset the trust holds, including property, equipment, vehicles, stock and other assets used in the business. This helps protect your asset protection goals by showing that the business and its assets sit inside the trust structure, not in your personal name. Good records help keep the trust’s affairs separate from the corporate trustee’s own affairs where a company acts as trustee. However, limited liability is not absolute, and exposure may still arise through director obligations, personal guarantees, tax liabilities, payroll obligations or limits on the trustee’s right of indemnity.

Tracking Trust Income and Net Income

Trust income is the amount of income the trust earns according to the trust deed, while net income is the amount worked out under income tax rules. Your bookkeeping system needs to track both the underlying business income and the adjustments needed for tax so you can correctly calculate net income. This is important because beneficiaries are generally assessed on their share of the trust’s net income based on present entitlement to trust income, unless specific rules apply.

The system should record all income from trading, investments, rent and other sources in separate accounts so that reports clearly show what the business earns. It should also capture expenses, depreciation, interest and other items that affect taxable income and net income. When you do this well, you make it easier to prepare accurate tax returns and avoid surprises when you meet your income tax obligations.

Recording Trust Distributions to Beneficiaries

One of the most important things your bookkeeping system must track is trust distributions to beneficiaries. Each year, as part of the trust’s formal administration, the trustee should make a valid distribution resolution in accordance with the trust deed, generally by 30 June or any earlier date required by the deed. These decisions should be documented and then recorded in your accounts through journals or specific beneficiary accounts.

Your bookkeeping should show clearly which beneficiaries receive distributions and how much each person or entity is entitled to, because proper documentation of trust distributions under Section 100A is critical to avoid unexpected tax consequences. This might include family members, a company beneficiary or even a unit trust in more complex structures. Recording distributions accurately helps ensure that beneficiaries include the correct trust distribution amounts in their tax returns and that the trust return, trustee resolutions, beneficiary accounts and trust deed are consistent.

Handling Loans, Drawings and Funds Between Related Parties

Many family trust groups have loans, unpaid present entitlements, reimbursements and payments between the trust, beneficiaries, related companies and family members, and deciding whether in‑house staff or an external firm will manage these records raises the usual in‑house versus outsourced bookkeeping considerations. Your bookkeeping system should classify each movement according to its legal and tax character. Some amounts may be loans, some may be beneficiary drawings, some may reduce unpaid present entitlements, and others may be income, expenses, wages, dividends or reimbursements. Each related party should have a separate account showing money going in and out, including repayments and interest if applicable.

You also need to record any drawings or payments the trustee makes on behalf of beneficiaries, such as paying a personal expense from the trust bank account. These amounts may reduce a beneficiary’s unpaid present entitlement or increase a loan balance, and your system should handle them in line with the trust instrument and tax law. Where a private company beneficiary has an unpaid present entitlement, Division 7A may need to be considered. Keeping a clear record of these movements reduces confusion and helps show that the trustee is legally responsible and acting within their powers.

Capturing Capital, Property And CGT‑Related Information

If your family trust holds property or other long‑term assets, your bookkeeping file should keep full details of purchase costs, improvements, selling costs and sale proceeds, similar to how trustees of a super fund follow an SMSF compliance checklist for trustees to ensure all key records are captured. This information supports capital gains tax calculations and shows how trust property has changed over time. It is especially important when the trust is used for estate planning and long‑term asset protection.

Your system should track each property or major asset separately, with enough detail to show when it was acquired, what was paid, and any major changes made during ownership. When assets are sold, you can then see the full picture from purchase to sale, including any capital gains or losses. This level of detail helps confirm that the trustee holds and deals with trust property correctly and that tax outcomes are accurate.

Understanding Other Types of Trusts and Why Family Trusts Are Different

There are many types of trusts, including fixed trust, unit trust, bare trusts, testamentary trusts, trusts created for charitable purpose and inter vivos trusts created during a person’s lifetime. In a fixed trust or unit trust, the units held by each beneficiary define their share of income and capital, and the trustee has less discretion. Bare trusts, by contrast, often have a sole beneficiary who is effectively treated as the legal owner for many purposes.

A family trust is usually a discretionary trust where the trustee has wide discretionary powers to decide who benefits and when, within the terms of the trust deed, and this flexibility needs to be reflected in any Xero‑based cloud bookkeeping package you use to track income and distributions. Unlike a company with fixed shares, there is more flexibility but also more responsibility for correct trust administration. Your bookkeeping system needs to reflect this by tracking the decisions the trustee makes each year and how those decisions affect income, funds and distributions to beneficiaries.

We’re more than bookkeeping experts

As part of ACT Tax Group, we offer complete accounting and business advisory services tailored to your needs.

Everyday Bookkeeping Processes That Support Trust Administration

Day‑to‑day, a family trust that runs a business still needs all the normal bookkeeping tasks you would expect from any business. This includes recording sales, purchases, wages, superannuation, GST, PAYG withholding, STP reporting and bank reconciliations where those obligations apply. The difference is that you must always remember that the trustee holds and operates everything for the benefit of others.

To support this, you should build routines around coding transactions correctly, attaching supporting documents and regularly reviewing accounts that relate to beneficiaries and related entities. These habits form part of trust administration and help you show that the trustee carries out their obligations properly. Done consistently, they also make it easier to respond if questions arise about the trust’s tax affairs or the way trust assets and income have been applied.

Using Bookkeeping to Manage Risk and Protect Your Family

When a trust structure is used for business and investment, its benefits depend on careful management of liability, records and decisions. Accurate bookkeeping helps demonstrate that the trustee is acting as legal owner of trust assets, and that beneficiaries receive income and other benefits in line with the trust instrument. This may support asset protection goals by helping evidence that assets are held by the trustee for the trust, rather than blending into personal affairs. Asset protection outcomes still depend on the trust deed, trustee conduct, insolvency law, personal guarantees, tax liabilities and other legal factors.

Good records also make it easier to navigate changing circumstances, such as new family members, changes in business activity or future estate planning decisions. Over time, the trust may hold a mix of business, investment and other assets, and your bookkeeping becomes the map that explains how these are owned and used. With clear, consistent processes, the trust can operate smoothly and meet its obligations without unnecessary stress for the trustee or the family.

How Professional Support Fits into Your Trust Journey

Setting up and running a family trust involves legal obligations, formal yearly administrative tasks and tax rules that go beyond basic business bookkeeping. While your bookkeeper can help you record and explain transactions, they do not constitute legal advice and cannot replace guidance from a qualified legal or tax adviser. It is important to get proper advice when you first set up the trust and whenever major changes are planned.

Your bookkeeping system then becomes the practical tool that turns that advice into day-to-day action. Clear records of income, assets, funds and distributions give your adviser the information they need to check how the trust operates and to prepare tax returns and reports. With the right support, your family trust can be a practical, flexible way to hold and grow your business while looking after the people who matter most.