Published on 10 Apr 2026

Salary Sacrifice and HELP/HECS: What Employers and Employees Need to Watch Out For is about how salary packaging can reduce income tax while still increasing the income used to calculate student loan repayments. If this balance is off, employees can face unexpected HELP or HECS bills at tax time even when their payslips show less tax.

Why Salary Sacrifice and HELP/HECS Matter Now

With cost‑of‑living pressures rising, more employees are using salary sacrifice arrangements to turn pre-tax salary into useful benefits instead of wages alone. At the same time, changes to HELP thresholds and repayment rates mean these arrangements can affect how much tax and HELP you pay. Without a clear view of how total remuneration packaging works, it is easy to save income tax on the surface but still end up paying more towards student loans.

We regularly help small and medium businesses in not-for-profit organisations and the private sector set up salary packaging in a way that supports long‑term goals. Our focus is always on keeping things simple, practical and compliant with the Australian Taxation Office while still delivering real tax savings. Clear communication between employers, payroll, and employees is the key to avoiding surprises.

Are your salary sacrifice arrangements pushing up staff HELP repayments?

Schedule a complimentary consultation with us today to review packages so PAYG and HELP stay in balance.

What Is Salary Sacrifice and How Does It Interact With HELP/HECS?

Salary sacrifice, also known as salary packaging, is an agreement where employees give up part of their pre-tax income in return for other benefits of similar value. Instead of receiving all income as wages, you may package certain expenses like extra superannuation contributions, a novated lease or other benefits into a salary sacrifice arrangement. This can reduce the income tax you pay, depending on the type of benefit and how the arrangement is structured.

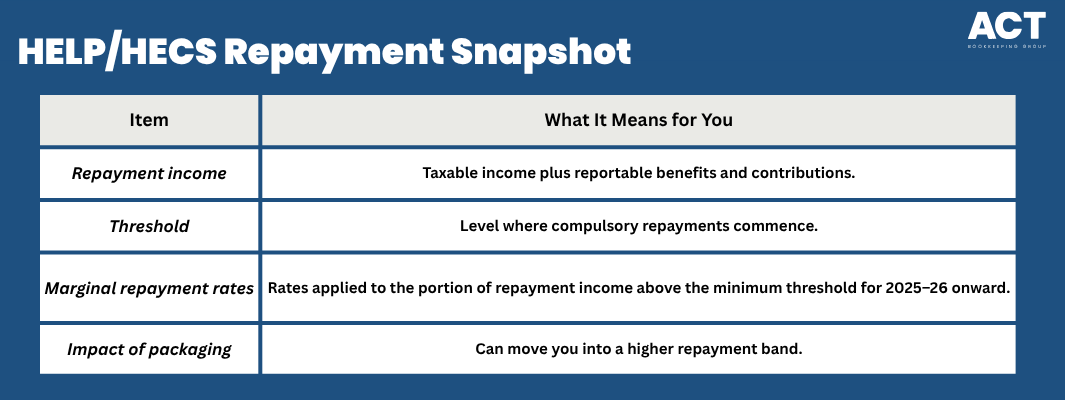

For HELP and HECS, the picture is different because repayments are based on a broader measure of tax income, not just the reduced taxable income that appears on your income statement. For HELP, the ATO uses repayment income, which includes taxable income, reportable fringe benefits, reportable super contributions, total net investment loss, and exempt foreign employment income. That means salary packaging work that reduces tax salary can still increase the income used to work out your compulsory HELP repayment.

How Have HELP/HECS Thresholds and Rates Changed?

From the 2025–26 income year, the minimum repayment threshold for HELP and other study loans is $67,000. Compulsory repayments are now calculated using marginal rates, so the repayment applies only to the portion of repayment income above the threshold, not a flat rate on the whole amount. This means some employees with less income tax on their payslips may still cross the new repayment threshold once packaged benefits are added back. When that happens, the Australian Taxation Office calculates a percentage of your repayment income and applies that to your HELP or HECS balance.

For 2025–26 and later, HELP compulsory repayments use a marginal repayment system. Higher income still means higher repayments, but the calculation method is no longer the older flat-rate percentage applied to total repayment income. This can have a real impact when salary packaging boosts your repayment income even though your after-tax income feels comfortable. Knowing where you sit on the scale helps you decide how far to take a salary sacrifice arrangement.

Why Can Salary Sacrifice Increase Your HELP/HECS Repayment?

Even though salary sacrifice is designed to help you pay less income tax, it can also increase the income used for HELP and HECS. When you salary package items that attract fringe benefits tax FBT or create reportable superannuation contributions, those amounts are added back to calculate repayment income. In other words, you may pay less tax on your wages but still pay more towards student loans.

This becomes important when packaged benefits like cars or living expenses create reportable fringe benefits. If reportable fringe benefits exceed the reporting threshold, the employer reports the grossed-up taxable value on the employee’s income statement, and that amount can increase repayment income for HELP purposes. If you have not asked your employer to withhold extra for HELP, you may face a bill when your tax return is processed.

What Should Employers Watch Out for with Salary Sacrifice and HELP/HECS?

Employers must make sure PAYG withholding and reporting match each employee’s tax and HELP situation. If you help staff commence salary packaging without understanding their HELP or HECS status, you may withhold less tax than needed. This can damage trust when employees receive unexpected tax and HELP bills.

Employers must correctly report salary sacrifice and other required amounts through STP income statements, including reportable fringe benefits where applicable, leave entitlements such as annual leave loading calculations, and reportable employer super contributions. When benefits attract fringe benefits tax, you must pay fringe benefits tax where required and show the taxable value or other reportable amounts clearly. Working with a bookkeeping team and following a clear PAYG withholding guide for business owners helps you keep payroll, tax, and salary sacrifice arrangements aligned.

Employer Checks to Put in Place

Make sure new employees complete a TFN declaration and answer the study-loan question correctly. Existing employees can update this using a Withholding declaration.

Explain how salary packaging work may affect tax income and HELP repayments.

Make it easy for employees to tell payroll they have a study loan, so the correct additional withholding can be applied. Employees with multiple income sources may still need to review whether withholding will fully cover their year-end compulsory repayment.

Keep clear records of fringe benefits, exempt benefits and employee contributions, including accurate treatment of minor fringe benefits for FBT purposes.

What Should Employees With HELP/HECS Check Before Salary Sacrificing?

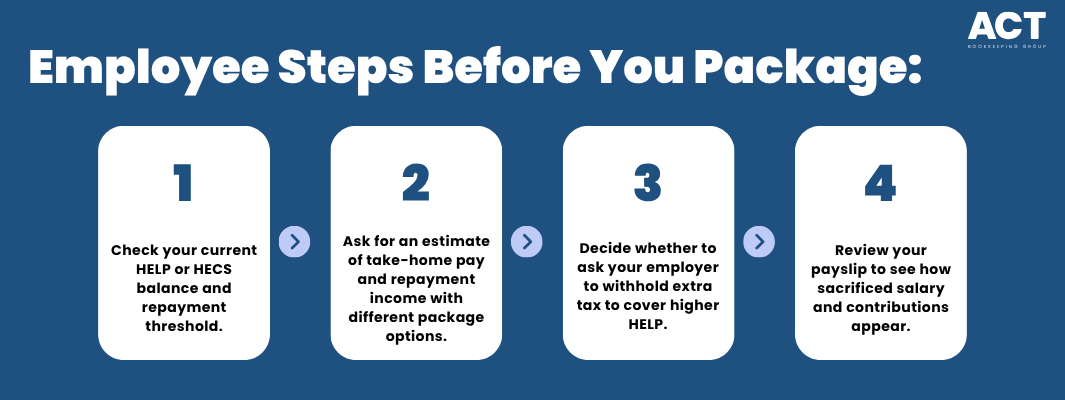

If you have a HELP or HECS balance, it is important to understand how a salary sacrifice arrangement will affect both take-home pay and your student loan. Packaging certain expenses can bring less tax and more home pay but may also push your repayment income above the threshold. You need to decide whether that trade still feels right once you factor in the higher compulsory repayment.

Before signing an agreement with a salary packaging provider or your employer, take the time to compare your situation with and without packaging. Look at your total remuneration packaging, not just the wages component. It often helps to ask your payroll or adviser to estimate how much HELP you will pay under each option.

What Salary Sacrifice Options May Have Less Impact on HELP Repayment Income?

Common salary sacrifice benefits include additional employer super contributions, a novated lease, and some other employer-approved benefits. School fees, mortgage repayments and everyday living expenses are not generally standard salary sacrifice items for most private-sector employees; they are usually only available where specific FBT concessions or exempt-employer rules apply, such as for some not-for-profit or public hospital arrangements. Some not for profit organisations can offer more generous exempt benefits that give strong tax savings. However, many of these benefits still show up in the income used for HELP or HECS.

Some employees, particularly in eligible not-for-profit or similar concessionally treated organisations, may be able to package certain personal expenses under employer-specific salary packaging arrangements. For most employees, these items are not broadly available and should be checked carefully before being described as standard salary sacrifice options. While this can mean less tax and more value from your pre-tax salary, it does not always reduce repayment income. The key is to understand whether a benefit is exempt, taxable, or reportable for student loan purposes.

How Do Fringe Benefits and FBT Affect HELP/HECS?

Fringe benefits are non‑cash benefits provided in place of wages and may attract fringe benefits tax FBT. When benefits attract fringe benefits tax, the taxable value is used to determine how much FBT the employer must pay. If the total taxable value of certain fringe benefits exceeds $2,000 in the FBT year, the employer reports the grossed-up taxable value as a reportable fringe benefits amount on the employee’s income statement.

For HELP and HECS, these reportable fringe benefit amounts are added back to your taxable income to calculate repayment income. This means the more fringe benefits you receive, the higher your repayment income may be, even if you pay less tax on wages. Employers need to understand which benefits are exempt benefits and which attract fringe benefits tax, including choosing the right FBT calculation method, so they can manage costs and reporting.

We’re more than bookkeeping experts

As part of ACT Tax Group, we offer complete accounting and business advisory services tailored to your needs.

How Do Superannuation Contributions Fit into Salary Sacrifice and HELP/HECS?

Superannuation contributions are one of the most common benefits in a salary sacrifice arrangement. When structured properly, extra employer contributions into a superannuation fund can reduce taxable income and help you build long‑term savings. These contributions usually come from pre-tax dollars and can mean less tax right now.

However, many of these employer contributions are still counted as reportable contributions when working out repayment income. You also need to watch superannuation contribution caps so that total contributions do not create extra tax. A balanced approach looks at both tax savings and the impact on HELP or HECS, as well as your broader retirement goals.

How Can Salary Packaging Providers and Bookkeepers Help?

A salary packaging provider or experienced bookkeeper can help you design an arrangement that fits your goals without creating unexpected tax or HELP issues. They can explain how pre-tax, after-tax income and fringe benefits interact. This support helps both employers and employees make decisions confidently.

For employers, having a clear agreement with any packaging provider means you know which benefits may attract fringe benefits tax and what records you need. For employees, professional help can show how different packages change your take home pay and your HELP repayments. The aim is always to use these tools to save costs, not to add confusion.

What Are Your Next Steps If You’re Considering Salary Sacrifice and Have a HELP/HECS Debt?

If you are thinking about packaging certain expenses or benefits, start by listing your current salary, HELP balance and the benefits you are considering. Then, ask your employer, bookkeeper or packaging provider to show you the effect on tax, take home pay and repayment income. This will help you see whether the savings outweigh any increase in HELP repayments and how they interact with your PAYG instalments obligations.

From there, you can decide whether to move more of your income into pre-tax dollars, keep some expenses after tax, or adjust the mix of benefits and contributions. You can also choose to increase your PAYG withholding so that your tax and HELP are covered across the year instead of at tax time. The right balance will look different for every person and every business, which is why it helps to talk it through before you sign any agreement.