Published on 02 Jul 2026

How To Calculate Capital Gains Tax: Bookkeeping Records to Keep When Selling Business Assets is about keeping the right records so Capital Gains Tax (CGT) can be reviewed properly when a business asset is sold. Clear bookkeeping helps your accountant check the capital proceeds, cost base, capital losses, taxable gain and possible net capital gain without relying on memory. This matters because selling assets can affect your tax return, taxable income and tax obligations for the financial year. The final result can vary depending on the asset, the purchase price, the sale price, the ownership structure, the assets held and your individual circumstances.

Capital Gains Tax Basics for Business Asset Sales

Capital Gains Tax is not a separate tax in Australia. A net capital gain is generally included in assessable income and can affect how much tax you pay, including your broader income tax position. A CGT event can happen when you sell, transfer or dispose of an asset. Business property, goodwill, investment property, selling shares, an investment portfolio, inherited assets and some other investments can all involve different rules, so it is important to get tax advice before assuming the outcome.

Struggling to track records for CGT on asset sales?

Schedule a complimentary consultation with us today to organise your asset records for accurate CGT reporting.

Bookkeeping Records That Support the CGT Calculation

Good bookkeeping gives your accountant the evidence needed to calculate capital gains and review any capital gain or loss. The key records usually include the original purchase price, purchase costs, stamp duty, improvement costs, sale documents, legal fees, agent fees and settlement records. They should also show what happened, when it happened, who was involved and how the transaction or cost is relevant to the capital gain or capital loss.

According to the Australian Small Business and Family Enterprise Ombudsman 2025 data portal, 97.3% of Australian businesses were small businesses in June 2025. Many business owners do not have an internal finance team, so a clear asset file can make tax time easier and reduce delays when expert advice is needed, particularly if they are already managing other obligations such as ATO payment plans for overdue BAS.

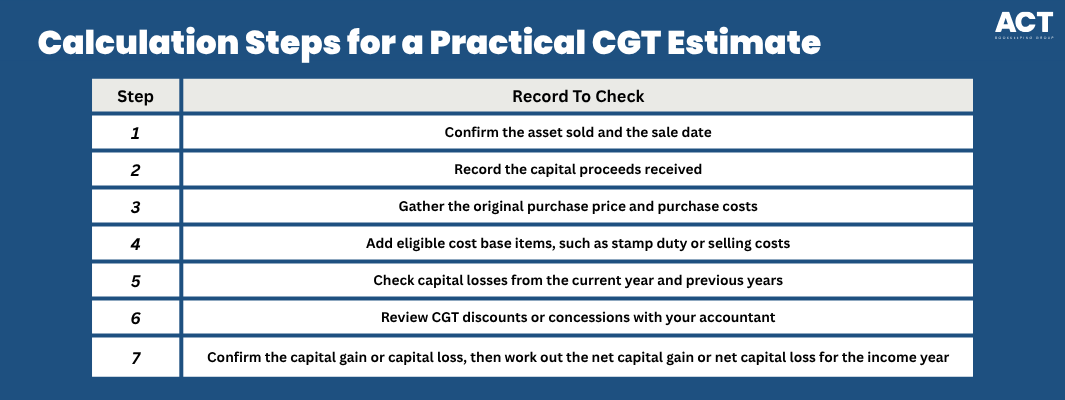

Calculation Steps for a Practical CGT Estimate

A basic CGT estimate starts with the capital proceeds from the sale and subtracts the cost base. The cost base may include the purchase price, purchase costs and some other costs linked to buying, holding or selling the asset, and it may also need to reflect past decisions such as using an instant asset write-off for small business. A capital gains tax calculator or free calculator may help you estimate capital gains tax, but it should not replace professional review. Online tools may not reflect your full financial situation, marginal tax rate, Medicare Levy Surcharge position, capital losses from previous years, or whether you can apply CGT discounts.

Tax Rules That Can Change the Final Outcome

The tax rules can vary depending on whether the asset was used in the business, held as an investment, partly used privately, or sold with other capital gains in the same year. Assets acquired or assets purchased at different times may also be treated differently for tax purposes. Instead of focusing on how to avoid capital gains tax, it is safer to focus on legitimate ways to reduce tax under the CGT rules. This may include applying capital losses before any CGT discount, reviewing whether a CGT discount is available, checking whether small business CGT concessions apply, or carrying forward a net capital loss to future years where the rules allow.

Depreciation, GST And BAS Records in the Sale File

Some business assets follow different rules because they are depreciating assets. A vehicle, equipment item, tool or machine used solely for business or other taxable purposes is generally dealt with under the capital allowance rules rather than CGT, while CGT may apply to the extent the asset was used for private or other non-taxable purposes. Goods and Services Tax (GST) and Business Activity Statement (BAS) records also matter when a business that is registered or required to be registered for GST sells a business asset, because errors in understanding the GST rate and GST rules in Australia can flow through to the CGT calculation. Your bookkeeping should show whether GST was included, how the sale was coded, and whether the sale was reported in the correct BAS period.

We’re more than bookkeeping experts

As part of ACT Tax Group, we offer complete accounting and business advisory services tailored to your needs.

Assets That Often Need Extra Care

Business property, investment property and mixed-use property often need extra care because the records may involve purchase costs, stamp duty, improvements, loan details and market value evidence. Property investors should also keep separate records for income, expenses and sale-related costs. A main residence is generally exempt from CGT, but a partial exemption or different calculation may apply if part of the property was used to earn income, especially where the 6-year main residence CGT rule could affect the outcome. Personal use assets may also have special treatment, so it is important not to assume that one rule applies to every asset.

How ACT Bookkeeping Can Help with Business Asset Sale Records

ACT Bookkeeping can help you prepare organised records before, during and after selling business assets. We can reconcile sale proceeds, update bookkeeping records, maintain asset details, organise GST and BAS information, and prepare clean reports for your accountant. If you are planning to sell equipment, vehicles, goodwill, property, shares or other business assets, arrange a consultation with our team before settlement. A short meeting can help identify missing records early and give your accountant the information needed to review the tax outcome.

Final Checks Before Selling a Business Asset

Before you sell, confirm what asset is being sold, when it was purchased, how it was used, what records support the cost base, and whether GST, depreciation, CGT or small business concessions may need review. Clear bookkeeping helps you understand the estimated capital gains tax position without relying on guesswork. The best time to organise records is before the contract is signed. With the right bookkeeping process, you can plan ahead, reduce last-minute stress and make informed decisions about the sale.