Published on 02 Jul 2026

How Your Business Remuneration Strategy Affects Medicare Levy Surcharge Exposure matters because the way you pay yourself can affect whether you pay the Medicare Levy Surcharge. For business owners, the issue is often not just taxable income, but the mix of salary, reportable benefits, family income, investment losses, and other amounts counted for Medicare Levy Surcharge purposes.

The Medicare Levy Surcharge, often called Medicare Levy Surcharge (MLS), is an extra tax that can apply when your income for MLS purposes is above the relevant income thresholds and you, your spouse, or your dependants do not have an appropriate level of private patient hospital cover. It is separate from the Medicare levy that most Australian taxpayers pay in addition to tax on taxable income.

Medicare Levy Surcharge Exposure for Business Owners

Medicare Levy Surcharge exposure is the risk that your income for MLS purposes places you in one of the MLS income tiers when you do not have an appropriate level of private patient hospital cover. This can affect individuals, families, single parents, and de facto couples, depending on their personal circumstances and whether they have a dependant child or MLS dependent child. For many business owners, the challenge is that Medicare Levy Surcharge purposes use a special definition called income for MLS purposes. Your tax return may show taxable income, but your income for MLS purposes may also include other amounts that change whether you are liable for the surcharge.

Confused about your MLS income calculation?

Schedule a complimentary consultation with us today to clarify income for MLS purposes.

Remuneration Strategy Can Shift Your MLS Position

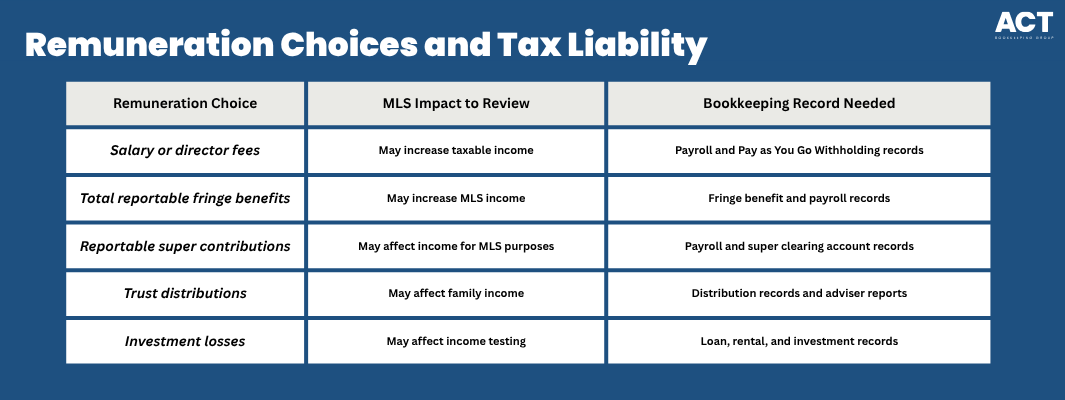

Your remuneration strategy can shift your MLS position because business income may reach you in more than one way. Salary, director fees, reportable fringe benefits, trust distributions, total net investment losses, and reportable super contributions can all affect your combined income or family income threshold.

Business owners should watch more than wages when reviewing whether they may pay the MLS. Income for Medicare Levy Surcharge purposes can include taxable income, total reportable fringe benefits, total net investment losses, reportable super contributions, and family income where your spouse or dependants are relevant.

Private Hospital Cover and MLS Outcomes

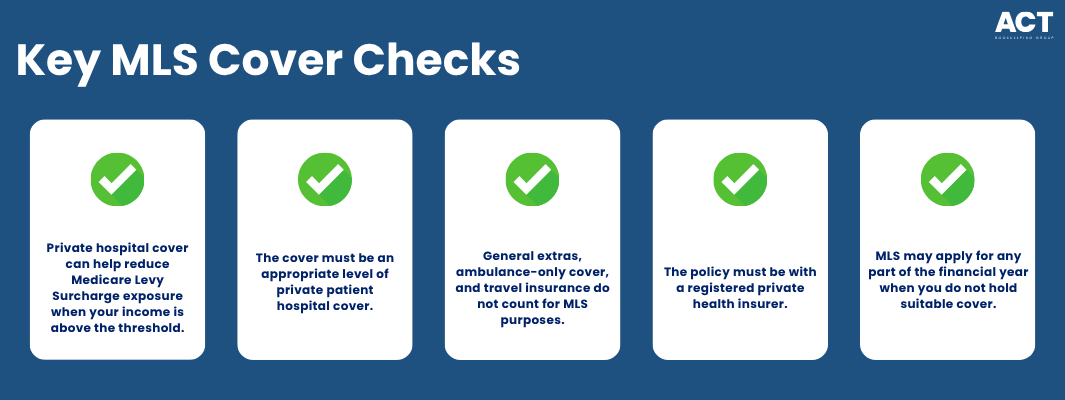

Private hospital cover matters because the surcharge is designed to encourage people who can afford private health insurance to use the private system. If your income for MLS purposes is above the threshold and you, your spouse, or your dependants do not have an appropriate level of private patient hospital cover for all or part of the financial year, you may have to pay the MLS for the relevant period.

The cover must be an appropriate level of private patient hospital cover provided by a registered private health insurer for hospital treatment in Australia, with an excess of $750 or less for a policy covering one person or $1,500 or less for all other policies. General extras cover, ambulance-only cover, travel insurance, and cover provided by an overseas fund do not count as private patient hospital cover for MLS purposes, so check your policy details rather than relying on the health fund name.

Remuneration Choices and Tax Liability

Different remuneration choices can affect tax liability because they change the income figure used to assess the levy surcharge. A business owner may avoid paying the MLS only where their personal circumstances, income for MLS purposes, and private hospital cover position meet the ATO rules, so it is sensible to review income, cover, and timing before the financial year ends rather than waiting until the tax return is prepared.

How ACT Bookkeeping Can Help with Remuneration Records and MLS Visibility

ACT Bookkeeping can help keep your payroll, superannuation, Business Activity Statement records, Goods and Services Tax records, and bookkeeping files organised so your adviser has cleaner information to assess Medicare Levy Surcharge exposure. We do not provide personal insurance advice or independent financial advice, but we can help make sure your business records are accurate, current, and ready for tax time.

We’re more than bookkeeping experts

As part of ACT Tax Group, we offer complete accounting and business advisory services tailored to your needs.

You can arrange a consultation with our team to review your bookkeeping processes, payroll setup, and reporting rhythm, including how you set up and manage ATO payment plans where tax debts are affecting cash flow. We help small to medium-sized Australian businesses stay organised, maintain practical compliance, and keep clear records that support your accountant, tax adviser, or financial planner.

Building a Remuneration Strategy with Better Visibility

A strong remuneration strategy should be reviewed before the end of the financial year, not after your tax return is being prepared. When your bookkeeping is up to date, you can give your accountant clearer numbers and discuss income thresholds, private health cover, family tiers, tax liability, Australian tax residency status, and whether you should seek your own independent financial advice based on your personal circumstances.