Published on 25 Jun 2026

How Accurate Bookkeeping Changes How Much Tax Refund You Get Back as a Sole Trader starts with one simple point: your refund depends on the quality of the income, expenses, and deductions recorded for tax purposes. For sole traders, the question “how much tax refund will I get” is really about your total assessable income, allowable deductions, tax offsets, Medicare levy, tax already paid, and any final tax payable or debt. The ATO’s income tax calculator can estimate a refund or debt for supported income years, but accurate bookkeeping gives the details needed for a more reliable estimate.

How Does Bookkeeping Affect a Sole Trader Tax Refund?

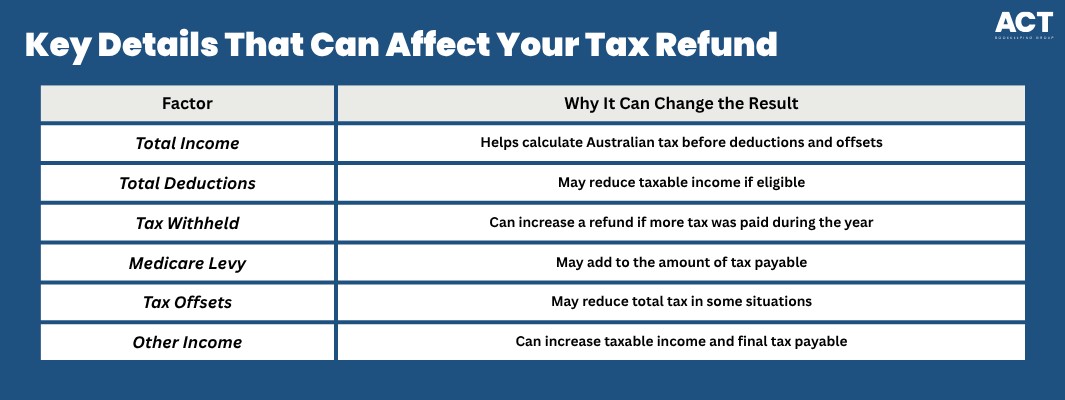

Bookkeeping affects your tax refund by showing what income you earned and what eligible expenses you can claim. Your income tax position is based on your gross annual income, other income, deductions, tax paid, and other factors that apply to your situation.

An ATO calculator may ask for details such as taxable income, tax withheld, private health insurance, Medicare levy information, tax offsets, and other information that affects your assessment. Good bookkeeping helps you enter the right amounts instead of guessing from bank deposits, old receipts, or memory.

Unsure if your records are accurate for tax time?

Schedule a complimentary consultation with us today to review your bookkeeping for ATO compliance.

Accurate Records Support Better Tax Deduction Claims

Accurate records help you claim deductions with more confidence because they show what the expense was, when it was paid, and how it relates to earning business income. For tax purposes, this can reduce taxable income where the expense is for business use, is not private, and you have records to prove the claim.

This matters because many sole trader expenses are easy to miss when they are paid from different accounts or collected across emails, paper receipts, and software platforms. Regular bookkeeping helps bring those details together so your registered tax agent can review the total amount before lodging your individual tax return with the business and professional items schedule.

Why Your Refund Is Not Based on Income Alone

Your refund is not based only on how much you earn. Australian income tax uses tax rates and marginal tax rate bands, but the final result also depends on tax deductions, tax offsets, Medicare levy, tax payable, tax withheld, and any debts or adjustments on your account.

This is why two taxpayers with the same annual income may receive different refund amounts. One may have more deductions, one may have private health cover, one may have other income, and one may have had more tax withheld by an employer. If the Medicare levy surcharge applies, the ATO works it out from information in the tax return and includes it with the Medicare levy on the notice of assessment.

Bookkeeping Gives You a Better Estimated Tax Refund

A tax refund estimate is only as reliable as the information entered. A calculator can help calculate an estimated tax refund, but it cannot check whether your bookkeeping is complete, whether expenses are eligible, or whether your records support the claim. For each financial year, sole traders should keep clear records of income, expenses, Goods and Services Tax (GST) if registered, bank activity, and supporting documents. Keeping records in order throughout the tax year gives you a clearer view of tax paid, estimated tax, taxable income, and possible refund or debt outcomes before lodgement time arrives.

Separating Business and Personal Costs Protects Your Tax Return

Sole traders often use one account for wages, business income, private spending, and tax payments. This can make it harder to identify what is business related and what should stay out of the tax return. Accurate bookkeeping separates business expenses from personal costs and helps your tax agent review the details properly. It also reduces the chance of claiming private expenses by mistake or missing business costs because they were paid from the wrong card.

What Information Should Sole Traders Keep for Tax Time?

Sole traders should keep records that explain their income, deductions, and tax obligations. This includes receipts, invoices, bank statements, income statement details, loan interest records, private health information, and any additional information needed by a tax agent. The most useful records are the ones that clearly show the date, amount, supplier, business purpose, and payment method. You must generally keep business records for 5 years, including records that support income tax, Business Activity Statement (BAS), GST, and deduction claims.

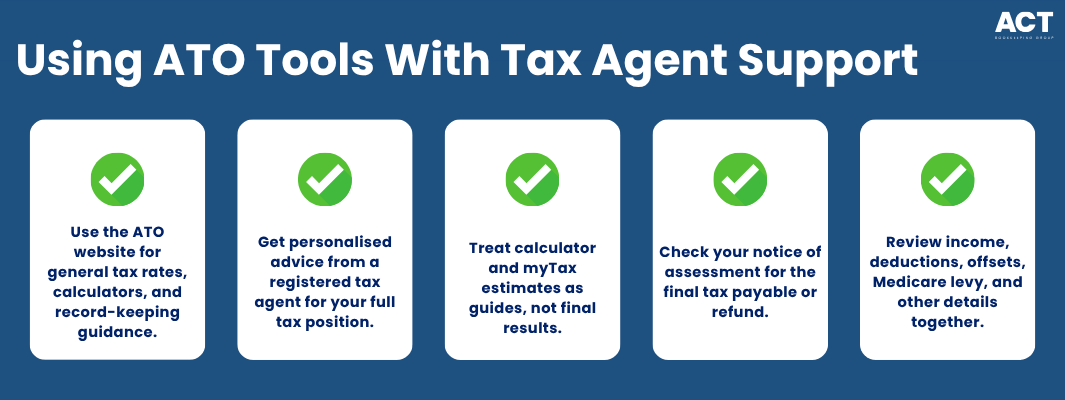

Why The ATO Website and Tax Agent Advice Still Matter

The ATO website provides tax rates, calculators, record-keeping guidance, and information to help Australian residents understand their tax obligations. However, general ATO information does not replace personalised advice from a registered tax agent who understands your employment income, business income, deductions, private health insurance details, debts, and other tax details.

A calculator or myTax estimate may give an estimate based on the figures entered, but the final result may differ after the ATO processes the return and issues a notice of assessment. Your final tax payable or refund may change when employment income, business income, other income, reportable fringe benefits, Medicare levy surcharge, tax offsets, and total deductions are reviewed together.

Common Bookkeeping Gaps That Can Affect Your Refund

Small bookkeeping gaps can affect your refund because they change the information used to calculate tax. Missing receipts, unreconciled bank transactions, duplicated income, incorrect expense categories, or unrecorded interest can all affect the final result, and in some cases may even lead to tax debts that need to be managed through an ATO payment plan. These gaps do not always mean something is seriously wrong, but they can make tax time slower and less certain. A consistent bookkeeping process helps keep your money records cleaner, which supports a smoother tax return and a more reliable refund estimate.

How Accurate Bookkeeping Supports Tax Planning

Accurate bookkeeping does more than prepare records after the financial year ends. It helps you understand your income, expenses, tax payable, and possible cash flow needs while there is still time to make informed decisions, including planning for major asset sales where small business CGT savings may apply. For sole traders, this can be especially useful when income changes during the year. If your pay, business income, fees, or expenses increase, your bookkeeping can help you discuss estimated tax, tax obligations, and possible planning steps with your registered tax agent before lodgement.

We’re more than bookkeeping experts

As part of ACT Tax Group, we offer complete accounting and business advisory services tailored to your needs.

How ACT Bookkeeping Can Help with Sole Trader Bookkeeping and Tax-Ready Records

We support practical bookkeeping, GST records, BAS support where relevant, receipt capture, software processes, and ATO-ready records that help reduce stress. You can book a meeting with our team to review your bookkeeping setup, identify missing details, and create a simple process for staying on top of your records across the tax year.

Final Thoughts on Accurate Bookkeeping and Your Tax Refund

Accurate bookkeeping can change how much tax refund you get back as a sole trader because it improves the information behind your tax return. It helps capture eligible deductions, report income correctly, support tax paid records, and give your tax agent clearer details to review. A calculator can estimate your refund, but bookkeeping helps make that estimate more reliable. The best next step is to keep records monthly, separate business and personal spending, and arrange support before tax time becomes stressful.