Published on 14 May 2026

What is a business trust and how does it affect your bookkeeping is a question many Australian owners ask when they are choosing the right business structure. When you use a trust for your business, it changes how you set up your books, how you track income and distributions, and how you stay on top of tax and reporting.

This structure matters because a trust is not a company in the traditional sense, even though many people think of it as a separate legal entity. Instead, the trust relationship sits behind the scenes while the trustee is legally responsible for day‑to‑day decisions and for meeting all tax and reporting rules. Getting your bookkeeping right is what links this trust structure to practical outcomes like asset protection, tax planning and peace of mind.

What is a Trust in Business

A trust in business is a legal arrangement where a trustee holds trust property such as cash, equipment or other assets on behalf of beneficiaries. The trustee can be a person or a company, and they operate the business and manage trust assets for the benefit of others under a formal trust deed. Unlike shareholders in a company, beneficiaries do not usually own the business assets directly, even though they may receive income from the profits.

Many small businesses use a trust structure because it can be tax effective, help protect assets and support family members over time. A corporate trustee is often chosen so that the company, not an individual, is primarily responsible for the business debts. This can help reduce the risk that a single person is personally liable for liabilities if the business incurs debt.

Confused about trust bookkeeping and ATO rules?

Schedule a complimentary consultation with us today to set up compliant trust accounts and records.

How a Business Trust Structure Operates

In a business trust, the formal trust deed sets out the rules about who the beneficiaries are, what rights they have, and how the trustee decides on distributions. The trustee holds and manages the trust property, including business assets and investment assets, in line with these rules and must act in the best interests of the beneficiaries. Profits from the business are not simply the trustee’s income; they belong to the trust and must be distributed or retained according to the trust deed.

There are different types of trust structure, including discretionary trust, fixed trust, fixed or unit trust, unit trust, family trusts, testamentary trust, charitable trusts and special disability trusts. In a discretionary trust or family trust, the trustee decides each year which beneficiaries receive income or capital and how much each one gets. In a fixed trust or unit trust, each beneficiary has a defined entitlement, often through units, similar to the way shareholders have defined rights in a company, and the taxation of unit trusts in Australia includes specific rules for income distributions and capital gains that you need to understand for compliance and planning.

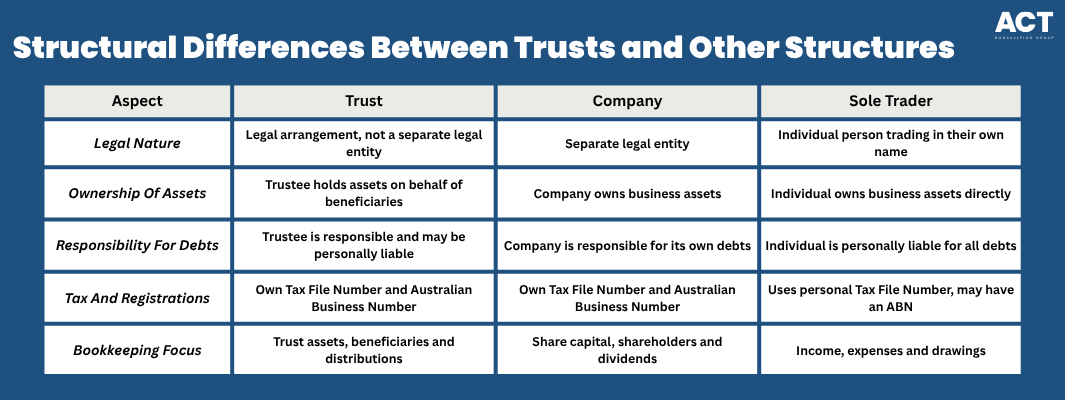

Key Differences Between Trusts and Other Structures

A trust is not a separate legal entity in the same way as a company, even though it has its own tax file number and Australian business number for tax and reporting purposes. A company is a legal entity that owns the assets and is responsible for its own debts, while a trust is a structure where the trustee is responsible and holds assets on behalf of others. A sole trader or a person trading under a personal name owns the business assets directly and is personally liable for debts, and their tax obligations as sole traders compared with companies in Australia differ from those applying to trusts.

Because of these differences, your bookkeeping and reporting need to match the structure. For example, in a company the focus is often on share capital, shareholders and dividends, while in a trust the focus is on trust assets, beneficiaries and distributions. Understanding which structure you use helps you code transactions correctly and avoid mixing personal and business funds.

Registrations Required for a Business Trust

A business trust should have its own tax file number. If the trust is carrying on an enterprise or business activities, the trustee should apply for an Australian business number for the trust in their capacity as trustee. If the trust’s annual GST turnover is $75,000 or more, or $150,000 or more for not-for-profit organisations, it must register for goods and services tax. Some activities, including taxi, limousine or ride-sourcing services, require GST registration regardless of turnover. These registrations sit under the trust’s name or business name, not the individual person, and your bookkeeping must clearly link each transaction to the right entity.

When a corporate trustee is used, the company will also be registered with the corporate regulator, but that does not replace the need to register the trust itself for tax. Your accounting system should clearly show which entity you are recording transactions for so that income tax and other obligations are reported correctly. This helps you avoid the confusion that can happen when multiple entities share bank accounts or use the same software file.

Day-To-Day Bookkeeping Under a Trust

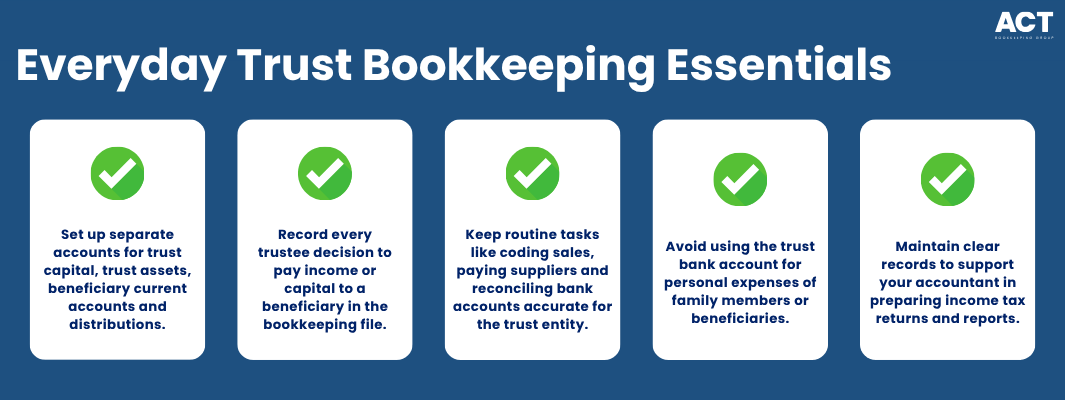

Because the trustee operates the business on behalf of beneficiaries, the way you set up your chart of accounts and track money becomes more complex than for a sole trader. You will usually have separate accounts for trust capital, trust assets, beneficiary current accounts and distributions rather than just an owner’s drawings account. Every time the trustee decides to pay income or capital to a beneficiary, this should be reflected in the bookkeeping file, not just on paper.

Routine tasks like coding sales, paying suppliers, and reconciling bank accounts still apply, but you must always remember you are recording transactions for the trust entity. Payments for personal expenses of family members or beneficiaries should not be made from the trust bank account unless they are properly treated as drawings or distributions under the trust rules. Clear bookkeeping makes it easier for your accountant to prepare income tax returns and other reports without guesswork.

Record-Keeping Requirements for Business Trusts

A trust needs to keep all the usual business records plus extra detail to show how profits and capital have been dealt with. This includes the formal trust deed, any variations, trustee resolutions, and detailed ledgers showing how much each beneficiary has received or is still owed. These records help show how the trustee has followed the rules in the deed and how the trust assets have been used over time.

Because a trust structure can be complex, it is important to record not just the amounts but also the reasons behind key decisions. For example, if the trustee decides to retain income in the trust or no beneficiary is presently entitled to that income, there should be clear supporting notes and entries, and the trustee should consider whether trustee tax applies and whether section 100A rules on trust distributions could affect the arrangement. Good records support asset protection, help minimise tax within the law, and make it easier to explain the trust’s position if questions arise later.

Treatment of Income and Distributions in a Trust

In a business trust, business income is earned by the trust but managed by the trustee. Before 30 June each year, or any earlier date required by the trust deed, the trustee should make valid resolutions about which beneficiaries are presently entitled to trust income or capital. If income is retained or no beneficiary is made presently entitled, the trustee should obtain advice on the tax treatment. These decisions should be documented through valid trustee resolutions or minutes that comply with the trust deed, are made on time, and clearly identify the beneficiaries and the income or capital being appointed.

Your bookkeeping needs to mirror these decisions through clear journal entries that move profits into the right beneficiary accounts. When cash is later paid to a beneficiary, it is recorded against their account rather than simply coded as a general expense. This makes it clear that the payment is for their benefit from trust profits, and not a wage or standard business cost.

Tax and Reporting Implications of a Trust

Even though a trust is not a company in the traditional sense, it still has important tax obligations. The trust usually needs to lodge a return for income tax each year and may also have goods and services tax reporting, payroll reporting and other tasks depending on the business. Beneficiaries generally pay tax on their share of trust income, but the trustee may be assessed in some circumstances, including where no beneficiary is presently entitled or where special rules apply to certain beneficiaries such as minors or non-residents.

Trusts may provide flexibility in how income is appointed to eligible beneficiaries, but distributions must comply with the trust deed, present entitlement rules and ATO guidance, and some structures use a bucket company to protect assets and manage tax on trust distributions within these rules. Arrangements where one beneficiary is made entitled but another person receives or uses the benefit may need to be reviewed under section 100A. To be genuinely tax effective and to minimise tax within the rules, the trust must meet certain criteria and the trustee must follow the deed and relevant laws. Reliable bookkeeping helps ensure the trust tax return, including the statement of how trust income was distributed, matches the trust deed, trustee resolutions, beneficiary accounts and actual business records.

Role of Trusts in Asset Protection

One of the key advantages of using a trust structure is asset protection. Because the trust assets are held by the trustee on behalf of beneficiaries, they are generally separate from the personal assets of the beneficiaries. When a corporate trustee is used, the company may also help limit the personal liability of individuals if the business incurs debt, as long as they have met their duties.

It is important to remember that protection is not absolute, and a trustee can still be personally liable in some situations, especially if they do not act properly or follow the trust deed. Careless mixing of personal and business funds or failing to keep records can weaken asset protection and give the impression that the trust is not being run as a genuine structure. Good bookkeeping, separate bank accounts and clear reporting are practical steps that support the overall goal to protect assets.

We’re more than bookkeeping experts

As part of ACT Tax Group, we offer complete accounting and business advisory services tailored to your needs.

Common Bookkeeping Issues In Trust Structures

Because trusts can feel abstract, one of the most common mistakes is treating the trust like any other business entity and ignoring the special rules. This might look like using one bank account for multiple entities, or letting family members use the trust account as if it were their personal wallet. Over time, this makes it hard to tell what belongs to the trust and what belongs to each person.

Another mistake is failing to keep beneficiary accounts and distribution records up to date, leaving large balances that no one can fully explain. Without clear records, it becomes difficult to see who has a defined entitlement and who has only received occasional payments. When the time comes to review profits, refinance, sell the business or support family members, these gaps can delay decisions and increase stress.

Value of Professional Support for Trust Bookkeeping

Because a trust can be complex, many trustees choose to work with a bookkeeping and accounting team that understands how trusts operate. They may also compare in-house bookkeeping with outsourcing to specialist bookkeepers when deciding how to manage trust accounts. A good adviser can help set up a chart of accounts that reflects the trust structure, separate bank accounts, and record transactions in line with the trust deed.

They can also help with yearly tasks, such as preparing distribution records, checking that trust rules are followed, and keeping records that support tax benefits where they are available under the law. Where a trust is connected with superannuation funds, accurate bookkeeping is also important so income, contributions, expenses and reporting records are kept separate and clearly documented.

With the right support, bookkeeping becomes a useful way to understand income, profits, capital and cash flow. You can see how funds have been used, what each beneficiary has received, and how the trust supports longer-term goals. This helps the business trust remain a practical structure for asset protection, family support, tax planning and business growth, rather than something reviewed only at tax time.