Published on 23 Apr 2026

The tax‑free threshold affects PAYG withholding setup for new employees because it changes how much tax is withheld from each pay cycle and how soon they start paying tax on their income. When you get this right from a new job, your employee’s take home pay better matches their actual tax obligations across the financial year. When it is set up incorrectly, employees can face an unexpected tax bill or even a nasty surprise tax bill at tax time, which often feels unfair and creates stress for both staff and employers.

What Does the Tax‑Free Threshold Mean for New Employees?

The tax-free threshold is the amount of annual income an Australian resident can earn before they start paying income tax. Put simply, the tax-free threshold means there is a free threshold of income where they do not pay tax, and then normal tax rates apply above that level. In practice, it is built into the way income tax is calculated for tax purposes generally, and it affects how much an employer withholds from each pay packet.

For a new employee, this directly affects how much tax is taken out of their pay before it lands in their bank account. If they claim the tax-free threshold with your business, you use the ATO withholding rates that factor the threshold into each pay cycle. In practice, this usually means less tax is withheld from weekly, fortnightly or monthly pay. If they do not claim the tax-free threshold, your payroll should apply the ‘no tax-free threshold’ withholding rate from the first dollar of taxable earnings.

Incorrect tax‑free threshold in payroll?

Schedule a complimentary consultation with us today to fix PAYG withholding setup.

How Does the Tax‑Free Threshold Affect PAYG Withholding in Practice?

When you set up a new employee, the decision to claim tax-free threshold or not tells your payroll which tax rates to use and how much tax to withhold each pay. If they claim the tax-free threshold with you, the employer withholds less tax during each pay cycle, because the tax-free portion of their income is spread across the year. If they do not claim it, you withhold tax as though they are already using their free threshold with another employer, which is a core part of how PAYG withholding works for employers.

This difference can be significant, even when two employees earn the same entire income and have the same tax situation. One may see more money in their pay packet each week because they have used their tax-free threshold with that employer, while the other may be essentially pre paying some of their total tax to avoid a large tax bill later. Your role is not to give personal advice, but to make sure the choice they make is correctly captured in your system so their total tax across the year lines up with their tax return.

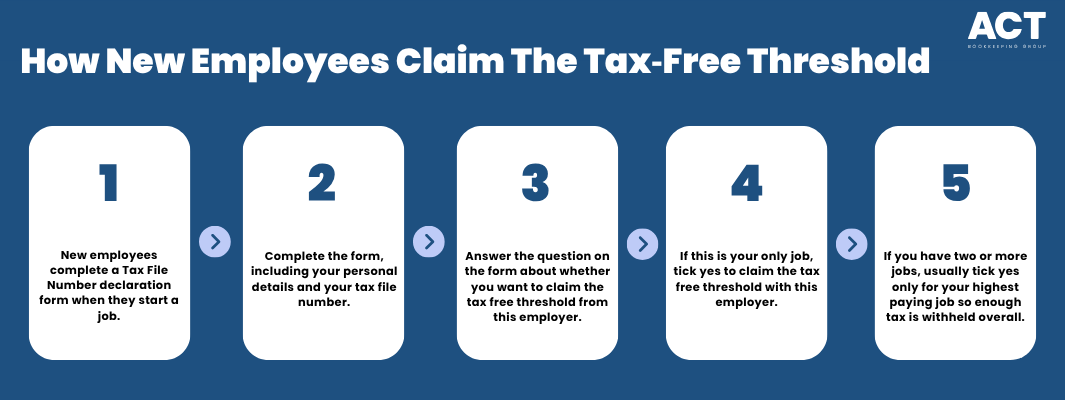

How Do New Employees Claim the Tax‑Free Threshold with an Employer?

New employees tell you how they want the tax-free threshold treated by completing a TFN declaration when they start. This can be done on paper or through ATO online services via myGov, depending on your onboarding process. On this declaration form, they answer a key question that asks whether they want to claim the tax-free threshold from this employer. This is what triggers your payroll software to either use the full tax-free threshold scale or the “no threshold” scale.

For someone whose only job is with your business, the choice to claim tax-free threshold is usually straightforward. Where it becomes more complex is when they have two or more jobs, a second job, or multiple jobs with more than one employer. In those cases, they might choose to claim the tax-free from their highest paying job, and not from the others, so that enough tax is withheld across all their income sources.

What Should Employers Look for on the TFN Declaration Form?

When you receive a TFN declaration form, you need to check the boxes relating to tax purposes, tax-free threshold, and whether they are an Australian resident or a foreign resident for tax purposes. Foreign residents cannot claim the tax-free threshold and are subject to special withholding rates, so your payroll settings must reflect that status accurately. You should also record their TFN, start date, and any study or training support loan withholding details provided through the employee tax details summary or a withholding declaration, as these affect how much tax you withhold.

Your duty is to enter this information accurately and keep it on file for your records. If the employee does not provide a valid TFN declaration, you generally need to withhold at the top rate from payments and complete/send the TFN declaration to the ATO with the details you have within 14 days of the employment start. Having a clear PAYG withholding process for business owners and getting this step right for each new job helps avoid mis‑matched total income figures and tax debt issues when the employee later lodges their tax return.

How Does the Tax‑Free Threshold Work When an Employee Has Multiple Jobs?

Employees with multiple jobs or multiple employers are where tax-free threshold decisions can become tricky. The general idea is that they should normally claim tax-free threshold from just one employer, usually the one where they earn their highest paying job income. If they try to use the tax-free threshold at more than one income stream when their combined income is above the threshold, they may not have enough tax withheld overall.

This can lead to owing money at tax time and ending up with a nasty tax bill. In effect, they may feel like they have had an interest free loan from the tax system during the year and then have to give it back at once. A better approach is often to claim the tax-free from their main job, and not from the second job, so that the employer withholds an appropriate amount of tax across all their income sources and avoids a substantial tax debt, much like using PAYG instalments to smooth income tax payments across the year.

How Do Tax Offsets and Low-Income Tax Affect New Employees?

For lower-paid staff, the low income tax offset can reduce tax when they lodge their return. It is generally applied on assessment rather than through ordinary payroll withholding, unless a specific withholding declaration applies for an eligible offset, and it interacts with the broader income tax calculation rules for Australians.

However, understanding that low-income tax settings and offsets exist can help you reassure staff who worry about paying income tax and whether they will get a tax refund or a larger tax refund. Someone with a modest annual income may still see some tax withheld during the year but receive a bigger tax refund once all offsets and the tax-free threshold are applied at tax time. Your role is to collect and report accurate payroll data so the Australian Taxation Office can apply these rules correctly.

What Are the Risks of Getting the Tax‑Free Threshold Wrong for New Staff?

If the tax-free threshold is set up incorrectly, employees can end up with too much tax or not enough tax withheld during the year. Withholding too much means they have less cash flow during the year, even though they might get a larger tax refund later. Withholding too little can lead to owing money and facing a nasty surprise tax bill or even a substantial tax debt when their tax return is processed.

For employers, repeated errors can raise questions about payroll processes and your handling of tax obligations. If your system treats a foreign resident as an Australian resident or shows a full tax-free threshold where the employee meant “no threshold”, you risk incorrect total tax collection and potential tax debt that may require an ATO payment plan to manage outstanding liabilities. A simple check of each TFN declaration form against your payroll settings for every new job is an easy way to reduce these risks and avoid stress for everyone.

How Does Claiming the Tax‑Free Threshold Affect Cash Flow and Tax Time Outcomes?

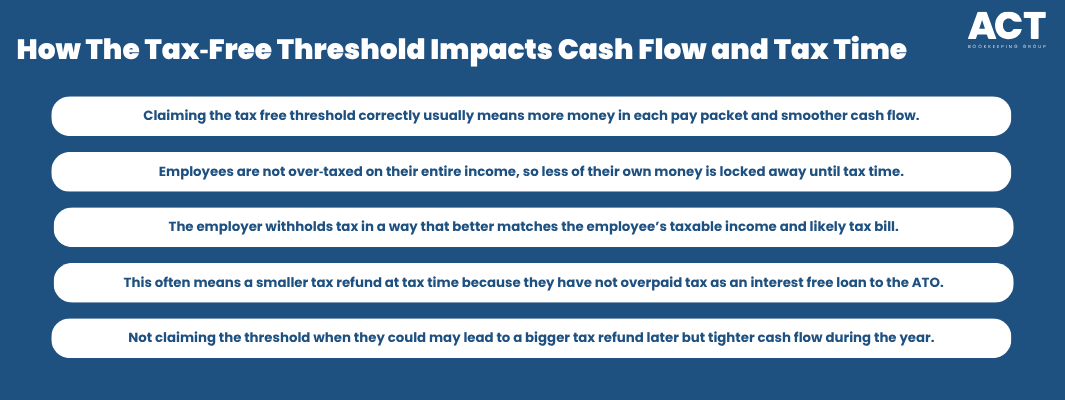

When an employee correctly claims the tax-free threshold from the right employer, it often means more money in each pay packet and more stable cash flow for day‑to‑day living. They are not over‑taxed on their entire income, so they do not feel like too much of their own money is locked away until tax time. Instead, the employer withholds an amount that better lines up with their actual taxable income and likely tax bill.

The trade‑off is that this may reduce the size of their tax refund at tax time, because they have not effectively used the ATO as an interest free loan provider by overpaying tax during the year. In contrast, if they choose not to claim tax-free threshold anywhere when they could, they may see a bigger tax refund later but struggle with cash flow now, and if they are also in the PAYG instalment system they need to avoid penalties for missed PAYG instalment payments. Helping employees understand how the tax-free threshold works can make their expectations about tax refund and tax bill more realistic.

Practical PAYG Setup Steps for ACT Employers

To keep your PAYG withholding setup clean and compliant for each new job, it helps to follow a simple checklist. First, always collect a completed TFN declaration form before the first full pay cycle where you withhold tax. Next, check how they have answered the tax-free threshold question, and whether they are an Australian resident or foreign resident for tax purposes.

Then, enter those details into your payroll system so that it knows whether to use the full tax-free threshold or no threshold scale when calculating how much tax to withhold. Make sure this aligns with whether this is their only job or one of two or more jobs, and remind them to update their details if their tax situation or combined income changes. Using robust systems also helps you stay on top of payroll tax obligations for your business. This simple process supports accurate total tax collection and reduces the chance of a surprise tax bill or large tax bill later.

We’re more than bookkeeping experts

As part of ACT Tax Group, we offer complete accounting and business advisory services tailored to your needs.

How ACT Bookkeeping Can Support Your PAYG and Tax‑Free Threshold Setup

At ACT Bookkeeping, we know that most business owners would rather focus on serving customers than navigating the finer points of tax and PAYG withholding or other business tax obligations in Australia. We help you build clear onboarding steps so every new job is set up with the right tax-free threshold choice, tax file number, and tax purposes details from day one, alongside guidance on related areas such as choosing the right FBT calculation method. This keeps your payroll tidy, gives your staff confidence in how their tax is handled, and helps you avoid avoidable issues with the Australian Taxation Office.

Conclusion

The tax-free threshold affects PAYG withholding setup for new employees by deciding whether you withhold tax from the very first dollar or after a free threshold of tax-free income. When staff claim tax-free threshold correctly with the right employer, it improves their cash flow, supports realistic expectations about tax refund and tax bill, and helps them avoid a nasty surprise tax bill at the end of the financial year. By using each TFN declaration form carefully and understanding how the tax-free threshold works across multiple jobs, you can protect your employees from owing money and keep your business aligned with the expectations of the Australian Taxation Office.

If you would like support checking your current PAYG setup or refining your onboarding process, our team at ACT Bookkeeping is ready to help you make this part of your payroll simple, clear, and reliable. Let us know if you have any other questions about the tax-free threshold, PAYG, or onboarding new employees.