Published on 02 Apr 2026

Tax Reporting Obligations for Different Types of Trusts and Required ATO Documentation matter for anyone using trusts in Australia to protect assets, manage family finances or hold business assets. Trustees must balance the tax benefits of different trust structures with clear reporting to the Australian Taxation Office, while keeping documentation strong enough to withstand review. Getting this right helps manage tax liabilities, support family members and protect trust assets over the long term.

Why Trust Structures and Documentation Matter in Australia

In Australia, every trust is a legal arrangement where a trustee holds assets for one or more beneficiaries under a trust deed. That deed sets out how trust income and capital can be used and how the trustee decides to distribute income or capital each year. A good trust structure, supported by the right documentation, can offer asset protection benefits, tax advantages and flexibility in managing family finances or retirement savings.

Our team works with family trusts, unit trusts, hybrid trusts, testamentary trusts and Self-Managed Superannuation Fund structures that involve trusts in Australia. Many clients feel unsure whether their records, trust law compliance and tax obligations for different types of trust would hold up if the Australian Taxation Office reviewed them. When trustees understand tax reporting obligations for different types of trusts and required ATO documentation, they can better manage tax liabilities, protect assets and manage intergenerational wealth with confidence.

Are you confident your trust records would satisfy an ATO review?

Schedule a complimentary consultation with us today to review your deed, minutes and ATO trust return obligations.

What Are the Core Tax Reporting Obligations for Trusts in Australia?

All resident trusts in Australia that earn trust income generally need their own tax file number and must lodge an annual trust tax return. That return reports both the income and capital of the trust, deductions, and how both the income and any capital gains are allocated between beneficiaries and, in some cases, the trustee. The trustee must also ensure that each legally competent beneficiary reports their share of trust income and capital gains in their own tax return for tax purposes.

A trust carrying on a business or enterprise generally needs an Australian Business Number (ABN). It must register for Goods and Services Tax (GST) if its current or projected GST turnover reaches $75,000 ($150,000 for not-for-profits), although ordinary residential rent is usually input taxed and does not itself attract GST.

Self-Managed Super Funds (SMSFs) are trust structures, but they sit under a separate superannuation regime and generally lodge an SMSF annual return, together with audit and record-keeping obligations, rather than an ordinary trust tax return. While a trust is not a separate legal entity in the same way as a company, it does have separate tax obligations, and the trustee is responsible for meeting them and managing the tax implications.

How Do Tax Reporting Obligations Differ Between Discretionary and Fixed Trusts?

Discretionary trusts, often called family trusts, give the trustee power to decide which beneficiaries receive income or capital and in what amounts each year. In contrast, fixed trusts and unit trusts usually give certain beneficiaries fixed entitlements, meaning those beneficiaries are entitled to a set share of both the income and capital based on units or other fixed interests. These differences affect how the trustee records income and capital distributions and how they manage tax obligations.

In a discretionary trust, the trustee must make a valid resolution by the time required under the trust deed, usually no later than 30 June, and should take extra care where capital gains or franked distributions are being specifically dealt with. If the trustee does not make effective discretionary distributions on time or the trust deed is not followed, there can be serious tax consequences and loss of tax concessions. In a fixed or unit trust, the trustee must show how income and capital have been allocated according to fixed entitlements, often supported by a unitholder register and clear records of unit holdings.

What Documentation Does Every Trustee Need to Keep On File?

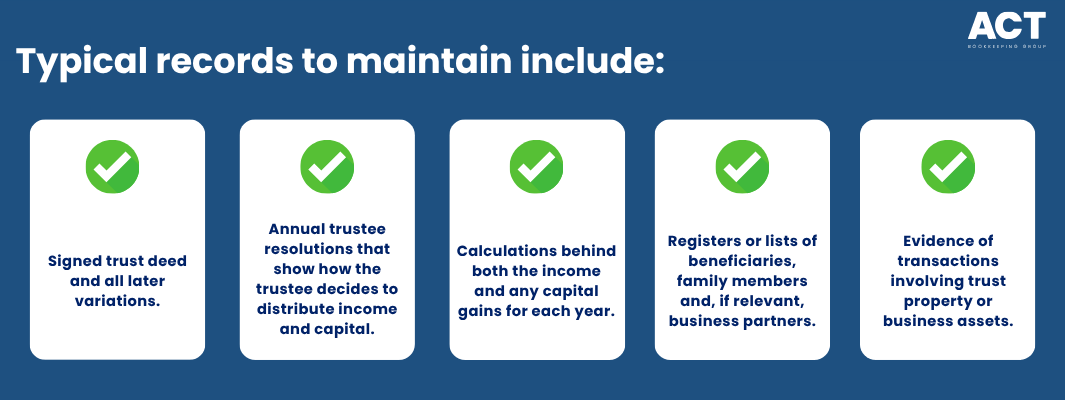

Every trust should have an executed trust deed that sets out the trust structure, beneficiaries, rules on income or capital, and any powers around discretionary distributions. Trustees must also retain any later variations to the trust deed so they can show how the legal relationship between trustee and beneficiaries has changed over time. Without these core documents, it becomes difficult to show who the beneficiaries are, what their rights are, and how the trustee’s discretion should be exercised.

Beyond the deed, trustees need clear records that support each year’s trust tax return. This usually includes distribution minutes or resolutions, working papers showing calculations of trust income, capital gains and franking credits, and records of how trust property and trust assets are used. Bank statements, invoices, loan agreements and records for the trust bank account are also important, especially when the trust holds business assets, investment property, managed funds or stock exchange investments.

How Do Trustees Report Income and Capital Distributions to Beneficiaries?

Each year, the trustee calculates the trust income for tax purposes, which may differ from accounting profit under trust law or the trust deed. They then determine which beneficiaries will receive trust income and whether any income or capital gains will be allocated to the trustee. Once decisions are made, trustees should provide beneficiaries with distribution information that aligns with the trust statement of distribution. Since the ATO’s reporting changes from 1 July 2024, beneficiaries who receive trust income generally need the information required to complete the Trust income schedule lodged with their own return.

For discretionary and unit trusts, it is vital that the trustee’s decisions match the trust deed and any rules about who can receive distributions. A minor can be presently entitled to trust income even if payment is made later, but special tax rules often apply to minors and higher rates can apply to non-excepted trust income. For testamentary trusts, concessional treatment for minors does not extend to income from assets injected on or after 1 July 2019 that are unrelated to the deceased estate.

In joint business ventures or family businesses using trusts, it is especially important to document how income and capital are split, so that each party understands the tax implications and can manage tax liabilities.

We’re more than bookkeeping experts

As part of ACT Tax Group, we offer complete accounting and business advisory services tailored to your needs.

What Extra Reporting Applies to Closely Held Trusts and Family Trusts?

Many family trusts are closely held, meaning they have a small number of family members or related entities as beneficiaries. These trusts often enjoy tax advantages and asset protection benefits, but they can also attract more attention from the Australian Taxation Office. For closely held trusts, trustees should check both the Tax File Number (TFN) withholding rules and the Trustee Beneficiary (TB) reporting rules. If applicable, they may need to withhold from certain beneficiaries who do not quote a TFN and complete TB reporting through the trust tax return.

Where a Family Trust Election (FTE) or Interposed Entity Election (IEE) is in place, trustees must make sure distributions stay within the relevant family group or they may trigger family trust distribution tax. If trust income is distributed in ways that are not supported by commercial reasons or the trust deed, there may be legal consequences and additional tax liabilities. In these situations, the trustee needs strong records to show that each legally competent beneficiary has correctly received and reported their share.

How Do Trusts Help Manage Assets, Asset Protection and Tax Planning?

Many people use discretionary and fixed trusts to manage assets for family members, protect assets from legal claims and support long‑term tax planning. The fact that legal ownership of trust property sits with the trustee, while beneficiaries hold beneficial interests, can provide asset protection benefits in some situations. This is particularly relevant for business partners, professionals and family businesses who want to separate their personal assets from business assets.

Trusts can also help manage intergenerational wealth and retirement savings by holding investment property, managed funds, business interests and superannuation‑related investments over time. Testamentary trusts can still offer concessional outcomes for some minor beneficiaries, but that treatment does not extend to income from assets injected on or after 1 July 2019 that are unrelated to the deceased estate. However, these tax benefits depend on following strict rules, and the trustee must keep documentation that shows the trust has been used for genuine trust law purposes and not just short‑term tax advantages.

How Can Professional Support Make Trust Reporting Easier?

Trust reporting and documentation can feel complex, especially for discretionary and unit trusts, hybrid trusts and structures involving Self-Managed Superannuation Fund investments. Trustees often juggle managing assets, running businesses and supporting family finances, while trying to keep up with changing tax obligations and strict rules from the Australian Taxation Office. Working with an accountant or financial advisor who understands trust law, tax implications and practical record‑keeping can take much of this pressure away.

Our team helps trustees review their trust deed, clarify their trust structure, and set up simple systems for documenting trust income, capital gains and distributions. We also assist with annual trust tax returns, distribution statements, tax file number reporting for closely held trusts and planning ahead for managing intergenerational wealth. This support makes it easier to meet tax obligations, protect assets and use the full range of tax benefits that Australian trust law allows, without getting lost in complex wording or unclear paperwork.

If you are unsure whether your trust documentation is strong enough, or if your current trust structure still suits your family finances or business assets, now is a good time to review. A practical review can highlight any gaps in how the trustee holds assets, how income or capital is distributed, and whether changes to your trust structure could better support your goals. Reaching out for advice today can help you protect assets, manage tax liabilities and keep your trust working smoothly for your family members and business partners in the years ahead.