Published on 25 Mar 2026

Cash flow vs profit: why your bookkeeping might show profit, but your business is actually insolvent is one of the most common and dangerous blind spots for Australian company directors and owners of incorporated businesses. When the profit on your reports looks healthy, it is easy to overlook that the business may not actually be able to pay its debts on time. Under the Corporations Act, a company is insolvent when it cannot pay its debts as and when they become due and payable.

How Can a Profitable Business Still Be Insolvent?

A company is insolvent when it cannot pay its debts as and when they fall due, even if it looks profitable on paper. This means that even if your profit and loss report shows a surplus, your company may still be in financial difficulties if there is not enough actual cash to cover wages, rent, supplier bills and tax liabilities. Insolvent trading occurs when a company incurs debts at a time when it is insolvent or when there are reasonable grounds to suspect insolvency.

In practice, a company’s financial position can look fine while its cash flow is under severe pressure because too much money is tied up in unpaid invoices or stock. When this happens, the business may rely on delaying payments, taking on new debt or using personal funds just to keep going. If directors allow the company to keep incurring debts it cannot pay, they may face insolvent trading proceedings and a court may order compensation or other consequences, depending on the facts.

Struggling to pay ATO and suppliers even though your reports show profit?

Schedule a complimentary consultation with us today to review your cash flow, BAS obligations and avoid insolvent trading.

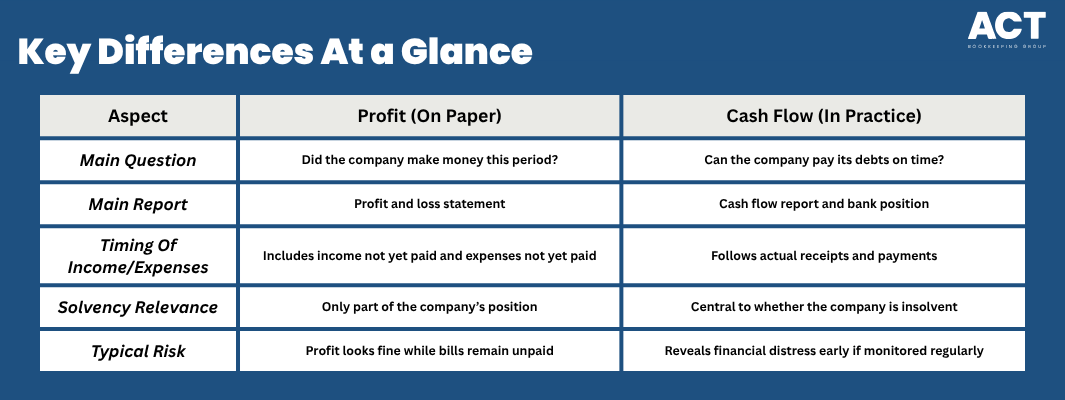

What Is the Difference Between Cash Flow and Profit?

Profit is the amount left after you subtract your expenses from your income over a period, usually shown on your profit and loss report. Cash flow tracks the actual movement of money in and out of the bank, which is what really determines whether your company can pay its debts when they fall due. A business can show a profit while still having serious cash flow issues if most of its income is tied up in unpaid debts or stock rather than cash in the bank.

In Australia, the law makes directors responsible for monitoring whether the company can pay its debts as they fall due. That means understanding the difference between profit and cash flow is not just a “nice to have” but part of managing corporations and meeting your duties. Looking at a single report in isolation can give a misleading view of the company’s financial position, so you need to look beyond profit and consider cash flow, aged payables and receivables, overdue liabilities, access to funding, and the accuracy of your records. Asset values may matter, but a balance-sheet surplus on its own does not prove solvency.

How Can Bookkeeping Choices Hide Cash Flow Problems?

The way your bookkeeping is set up and maintained can unintentionally hide the gap between cash flow vs profit and why your bookkeeping might show profit, but your business is actually insolvent. For example, accrual accounting can show strong sales and profit while your bank account is under pressure because customers have not yet paid. If your reports are not up to date, it becomes even harder to see that the company is incurring debts it may not be able to pay.

When company directors do not receive regular bank reconciliations, aged debtor and creditor reports and clear cash flow summaries through reliable cloud bookkeeping systems, they can underestimate the level of financial difficulties the business is facing. Incomplete or late records can also make it harder for an external administrator or liquidator to understand the company’s affairs if formal external administration is later needed. Good bookkeeping is not just about tax; understanding the different types of bookkeeping services available is a key tool to prevent insolvent trading.

What Does Australian Law Say about Cash Flow and Insolvency?

Under the Corporations Act, insolvent trading occurs when a company incurs debts while it is insolvent or becomes insolvent because of those debts. The law makes directors responsible for taking reasonable steps to stay informed about their company’s financial position and to prevent insolvent trading. If a company is insolvent and continues trading, the consequences of insolvent trading can include civil penalties, compensation proceedings and, in serious dishonest cases, criminal charges.

Civil penalties can include orders that company directors pay compensation for losses linked to insolvent trading debts and, in serious cases, possible criminal prosecution. Directors can be held personally liable for company debts if they allow the company to continue trading while insolvent and do not take reasonable steps to address the company’s insolvency. In serious dishonest cases under subsection 588G(3), an individual may face up to 5 years imprisonment, 2,000 penalty units, or both.

How Do Delayed Payments and Tax Debts Impact Cash Flow?

Even when your sales are strong, delayed customer payments can cause serious cash flow problems that push the company towards insolvency. When customers pay late, you are effectively lending them money, which can leave you short when wages, rent and suppliers need to be paid. If the company is always chasing money rather than being effectively chasing money through clear terms and regular follow‑up, the risk to the company’s finances grows.

Unpaid tax debts and poorly managed ATO payment plans are another major risk area for small businesses. When tax, super and other obligations remain unpaid or you are struggling to manage ATO payment plans for overdue BAS statements, this can be a sign that the company’s financial position is under strain. Using unpaid GST, PAYG withholding or Super Guarantee Charge (SGC) as short-term working capital can quickly increase risk, including personal exposure under the director penalty regime. From 1 July 2026, employers generally need to pay super on payday.

We’re more than bookkeeping experts

As part of ACT Tax Group, we offer complete accounting and business advisory services tailored to your needs.

Why Are Cash Flow Forecasts Essential for Proving Solvency?

A practical way to understand cash flow vs profit and why your bookkeeping might show profit but your business is actually insolvent is to prepare a simple cash flow forecast. This forecast shows when money is expected to come in and when it needs to go out, helping you see whether the company can pay its debts over the coming weeks and months. It also helps company directors avoid new debt that may not be sustainable.

If a cash flow forecast shows a period where the company is unlikely to pay its debts on time, directors need to consider options such as cost reductions, renegotiating terms or seeking professional advice. When reasonable steps cannot restore the company’s position, it may be necessary to consider formal options such as small business restructuring (if eligible), voluntary administration, a DOCA, or liquidation. Having a forecast ready also helps a formally appointed external administrator quickly understand the company’s finances if that step becomes necessary.

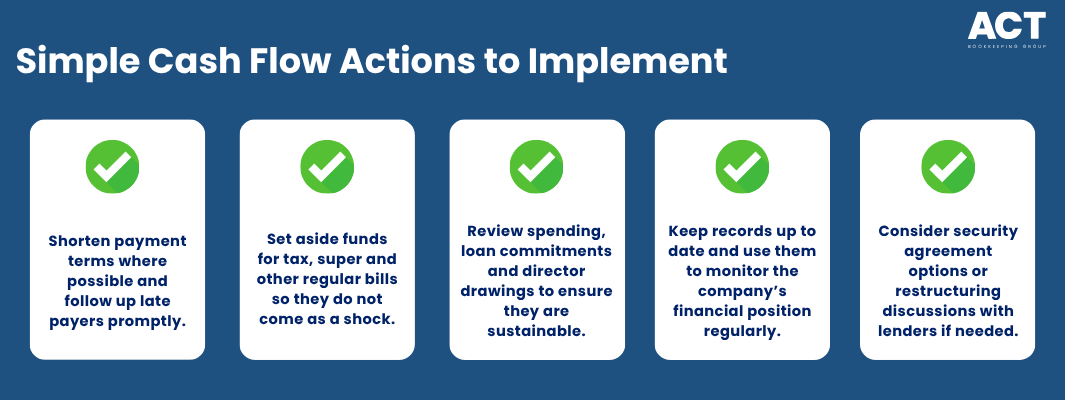

What Practical Steps Can You Take to Protect Your Cash Flow?

Once you understand the gap between cash flow vs profit and why your bookkeeping might show profit, but your business is actually insolvent, you can start tightening your cash flow management. Practical, consistent action now can reduce the risk of insolvent trading and help avoid personal liability later. This applies to directors of small companies and corporate groups, but group structures and holding companies can raise separate issues, so entity-by-entity advice is important.

Focusing on debtor management, realistic payment terms and keeping your bookkeeping up to date, including considering outsourced bookkeeping services, can make a major difference. It also helps you stay informed about your company’s position and make decisions that align with the best interests of the company and, where the company is insolvent or at real risk of insolvency, with proper regard to creditors, including employees with outstanding entitlements. If you suspect insolvency or see ongoing warning signs, it is important to seek professional advice rather than waiting.

Conclusion

Understanding cash flow vs profit and why your bookkeeping might show profit, but your business is actually insolvent is essential if you want a business that is both busy and financially sound. The focus must be on whether your company can pay debts when they fall due, including all the person’s debts and any debts incurred, not just whether it records a profit on paper. Regular reports, cash flow forecasts and early action when you suspect insolvency can make all the difference.

By staying informed about your company’s financial position, acting on warning signs and seeking professional advice early, you can prevent insolvent trading and protect yourself from being personally liable for company debts and all the person’s debts linked to the business. If you are concerned about your company’s position, the debts incurred, or want help building stronger cash flow habits, now is the time to reach out for support so you can move forward with clarity and confidence.

Frequently Asked Questions

How Can I Tell If My Business is Cash Flow Insolvent?

You may be facing cash flow insolvency if your company cannot pay its debts as they fall due and you cannot see a realistic way to fix this in the short term. This might show up as ongoing unpaid debts, constant pressure from creditors, and using further debt just to stay afloat. If you suspect insolvency, you should immediately seek professional advice to understand your options and avoid trading insolvent.

Does Making a Profit Mean I Am Safe from Insolvent Trading?

No, making a profit does not automatically mean your company is safe from insolvent trading. If your cash flow is weak and you cannot pay its debts on time, your company may still be insolvent. The key question is whether the company can meet its commitments when they fall due, not just whether the profit and loss report looks positive.

What Happens If I Keep Trading While Insolvent?

If you keep trading while insolvent, you may face an insolvent trading claim and be personally liable for some company debts. Insolvent trading leaves both the company and its unsecured creditors in a worse position, and you may face civil penalties or, in severe cases, a criminal offence and possibly criminal penalties. Taking reasonable steps early, including seeking professional advice and considering options like voluntary administration or a Deed of Company Arrangement (DOCA), can help avoid these outcomes.

How Can a Bookkeeper or Accountant Help You Stay Solvent?

A proactive bookkeeping and advisory team can help you bridge the gap between cash flow vs profit and why your bookkeeping might show profit, but your business is actually insolvent. With accurate, timely records, regular reports and rolling cash flow forecasts, you can see issues early instead of being surprised by sudden financial distress. This support also helps you stay informed and make decisions that protect both the company and your own debts and obligations, reinforcing that choosing quality bookkeeping services over cheap options can significantly reduce the risk of insolvent trading.

A competent and reliable manager or adviser can help you assess whether your company is incurring debts it can realistically pay and what steps are available if the company’s insolvency risk is rising. They can also help you understand formal options such as external administration, employee entitlements issues, or Fair Entitlements Guarantee (FEG) claims where relevant, and how to protect the market value of the company’s assets where possible. Having the right guidance makes it much easier to manage the company’s business in line with insolvent trading laws and avoid being personally liable.