Published on 11 Mar 2026

Record Keeping and Documentation Requirements for the Small Business Retirement Exemption Claim can make the difference between a smooth outcome and a stressful review. When you sell a CGT asset and want to use the small business retirement exemption, you need clear records to show your eligibility and how you calculated the exempt amount. Without a good written record, you risk losing the concession, paying more capital gains tax (CGT) and delaying your business retirement plans.

For many small business owners, paperwork becomes urgent only when a CGT event happens, such as selling a commercial property, goodwill or shares in a company. The small business CGT concessions, including the retirement exemption, 50% active asset reduction and rollover exemption, can reduce or even fully disregard capital gains if you meet the eligibility criteria. Because these concessions can change your assessable income, the ATO expects your business to keep a strong audit trail for each sale or restructure.

What Is the Small Business Retirement Exemption and Why Do Records Matter?

The small business retirement exemption lets you disregard all or part of a capital gain on certain business assets up to a lifetime limit of 500,000 per individual. This business retirement exemption is part of the small business CGT concessions and sits alongside the 15‑year exemption, 50 active asset reduction and rollover exemption. When you use this exemption, your records need to clearly show the exempt amount and how it fits within your personal lifetime limit.

To qualify, you must meet basic eligibility requirements, such as being a small business entity or satisfying the maximum net asset value test. You also need to show the asset is an active asset used in your business and, in some cases, that there are other stakeholders who are eligible to share in the retirement exemption payment. Each of these points must be backed by consistent documents that can be produced quickly if the ATO asks questions.

Worried your retirement exemption records won’t satisfy the ATO?

Schedule a complimentary consultation with us today to review your CGT working papers and plug any record‑keeping gaps.

What Are the Core Record Keeping Requirements for the Retirement Exemption?

The ATO expects you to keep a written record of the exempt amount you choose to apply to the retirement exemption for each CGT event. If a company or trust is making the claim, it also needs a written record showing each CGT concession stakeholder’s percentage so that payments are equal to the recorded shares. These records sit with your usual CGT working papers so that you can show exactly how you reached the final figures.

In practice, your file for each sale should include a summary that explains the capital proceeds, cost base, capital gain or capital losses, and which other concessions you used before the retirement exemption. Where you also applied the cgt discount, 50% active asset reduction or rollover exemption, your notes should show the order and calculations. This makes it clear why the final exempt amount is correct and why that part of the gain is disregarded rather than included in assessable income.

How Does Age and Superannuation Affect Documentation Requirements?

If you are under 55 just before choosing the retirement exemption, the exempt amount must be contributed to a complying superannuation fund or retirement savings account (RSA). In this case, you need documents that show the payments, the fund details, the date of each contribution and any specific form you lodge to have it counted under the CGT cap instead of as a non concessional contribution. These records link your super contributions back to the retirement exemption payment.

If you are 55 or older just before choosing the retirement exemption or before receiving a retirement exemption payment from a company or trust, you do not have to contribute the exempt amount to a super fund. You still need a written record of your choice to use the retirement exemption and any payments to other stakeholders. Clear documentation helps you track how much of your lifetime limit you have used and gives you flexibility with how you access funds for your future.

What Supporting Records Do You Need to Prove Eligibility and CGT Calculations?

Beyond the retirement exemption records, you must keep documents that show how you worked out your capital gain or capital losses. This usually includes purchase contracts, capital proceeds statements, settlement sheets, legal bills, and invoices for improvements that affect the cost base. Together, these papers support the figures you enter in your income tax return and show how you reduced the original gain.

You also need records that prove you met the eligibility criteria for the small business concessions at the time of the CGT event. These might include financial statements to show maximum net asset values, turnover tests for small business status and evidence that the asset was an active asset used in your business. For interposed entities, such as trusts and companies, you should also keep share registers, trust deeds and minutes that explain how interests are owned and how other stakeholders are linked to the asset.

What Specific Documents Should Small Businesses Keep for a Retirement Exemption Claim?

It helps to create a dedicated CGT and business retirement exemption file for each asset that might trigger a capital gain. This file becomes your single reference point for every step, from purchase through to sale and any later rollover exemption or replacement asset. Having everything together reduces stress if the ATO asks for more detail in a later year.

How Long Do You Need to Keep Records for a Retirement Exemption Claim?

CGT record keeping often runs over many years because the tax outcome depends on events from purchase to final sale. As a guide, you should keep key records for at least five years after you dispose of the asset. If you keep a certified CGT asset register, you may be able to discard source records five years after the entry is certified. If you create an asset register that meets ATO standards, you may be able to store details there and safely dispose of some older documents while still staying compliant.

For small business retirement exemption claims, it is often wise to keep crucial records for longer than the bare minimum, especially where there are interposed entities or multiple other stakeholders. Extended retention helps if there is an amended assessment or if you need to claim a related capital loss or make a later rollover exemption choice. Strong records give both you and your adviser confidence that your position remains well supported in any later year.

We’re more than bookkeeping experts

As part of ACT Tax Group, we offer complete accounting and business advisory services tailored to your needs.

How Do Record Keeping Needs Differ for Individuals, Companies and Trusts?

Individual small business owners need to show they personally meet the eligibility requirements, own or partly own the asset, and have correctly calculated and recorded the exempt amount. Where the following conditions apply and they are under 55, they must also show that the retirement exemption payment was contributed to a complying superannuation fund, super fund or retirement savings account. Their documentation is usually more direct but still needs to cover the full capital gains tax picture.

A company or trust claiming the business retirement exemption needs an extra layer of documentation. It must show how the asset is owned, how the gain was calculated, and how payments were made to CGT concession stakeholders. Clear records should show that each stakeholder’s share of the retirement exemption payment is equal to their documented percentage and that the company or trust has met all retirement exemption conditions.

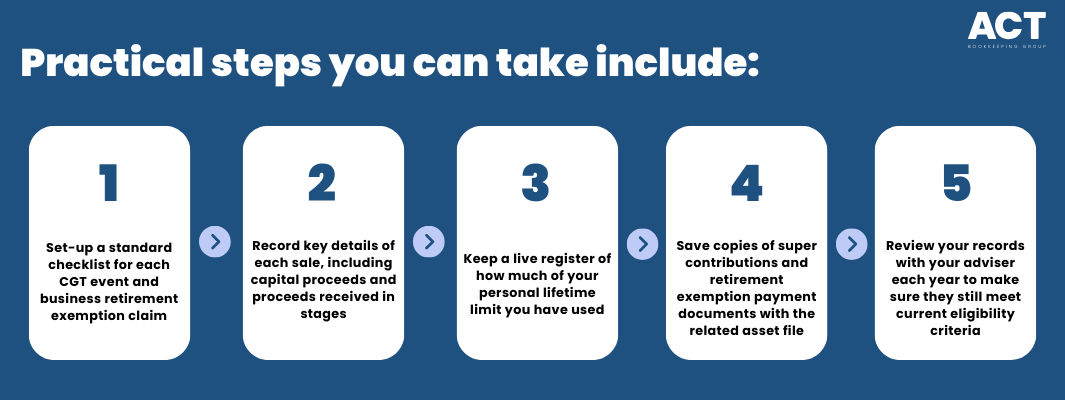

How Can You Build Practical Systems to Stay Compliant?

Instead of waiting until a major sale to gather documents, it is more effective to build CGT record keeping into your day‑to‑day systems. A simple digital folder structure for each asset and fund can keep contracts, invoices and contributions in one place. Using a CGT asset register helps track purchase dates, capital improvements and cost base adjustments over time.

What Are the Risks of Poor Documentation When Claiming the Retirement Exemption?

Weak or incomplete records can mean you cannot prove that you were eligible for the small business retirement exemption when the CGT event happened. In that situation, the ATO may treat the full capital gain as assessable income and tax it at your normal rate. This can be a shock when you expected the exempt amount to help build your nest egg or support your small business retirement plans.

Poor documentation can also affect your ability to defer a gain under a rollover exemption, or to use capital losses and other concessions effectively. If the ATO challenges your claim, you may face extra adviser costs and time spent trying to rebuild records from past years. By contrast, strong records let you show you qualify for the concessions you used and help protect you if the rules change in the future.

When Should You Involve a Professional Adviser?

Because small business CGT and retirement exemption conditions can be complex, it helps to speak to an adviser early, ideally before you commit to a sale or restructure. A tax and bookkeeping team can review your current records, check your eligibility criteria and help you plan how to access the concessions in a way that suits your future goals. Early advice often means you can shape the sale terms, superannuation fund strategy and timing of payments rather than trying to fix issues afterwards.

If you are thinking about selling a business, commercial property or other business assets, or want to know whether you will qualify for the small business retirement exemption, now is a good time to review your documents. Together, we can build a clear record keeping framework that supports your claim, protects you from unwanted tax surprises and helps you grow your retirement nest egg.