Published on 26 Feb 2026

Setting Up Your Depreciation Schedule and Asset Register for ATO Compliance helps you stay aligned with Australian Taxation Office expectations while making the most of your depreciation deductions. When you have a clear system to track your depreciating assets and how you claim depreciation, you reduce tax-time stress and the risk of errors in your tax return. For a small business owner, this can also mean a lower tax bill and better visibility over future equipment needs.

Why Simplified Depreciation Rules Matter for Small Businesses

This matters because the Australian Taxation Office expects you to keep accurate records for all business assets, from purchase price through to disposal. If your details are incomplete, you can miss an immediate deduction that you are entitled to or run into questions later. A simple, well-structured asset register, and depreciation schedule give you a clear story of what you bought, when it was installed ready for use, and how you calculated each claim.

For small businesses (turnover < $10M), assets up to $20,000 can be immediately written off (for assets first used by 30 June 2026), with larger assets added to the small business pool (15% deduction in the first year, 30% thereafter). Temporary full expensing (100% write-off) was only available until 30 June 2023 This guide walks you through how to set up your records so that whatever rules apply in a given income year, you have the right information ready to go.

Missing assets or dates in your register?

Schedule a complimentary consultation with us today to set up an ATO-ready asset register.

What Is a Depreciation Schedule and Why Does It Matter for ATO Compliance?

A depreciation schedule is a structured list that shows how you claim depreciation on your business assets over several years. It records the opening value, depreciation method, yearly deductions, and closing value for each item or pool. This is where you apply general depreciation rules or the simplified depreciation regime, depending on which rules you use.

For a small business, the schedule matters because it links every deduction in your tax return back to a specific asset, such as office equipment, coffee machines, or tablets office furniture. It also helps you track which assets were immediately deducted under instant asset write off and which are being claimed over time. When you keep this schedule updated each income year, it becomes much easier to calculate your taxable income and avoid mistakes.

How Does an Asset Register Support ATO Compliance?

An asset register is your master list of all business assets, including purchase price, date, description, location, and business purpose. It sits behind your depreciation schedule and gives the detail you need to show how and why you decided to claim depreciation the way you did. Think of it as your central record for everything from laptops to electric sanders and an entire set of tools.

The register also records business portion versus personal use, so you only claim the correct share of each asset. For example, a sole trader might use a car partly for personal trips and partly for business, so they would only claim the business portion. When set up well, the asset register makes any Australian Taxation Office review far less stressful because every figure in your schedule can be traced back to clear records.

What ATO Depreciation Rules Apply to Small Businesses?

For most assets, the general depreciation rules spread deductions over their effective life using set rates. From 1 July 2023 the small business turnover threshold is $10M, meaning businesses below this can use simplified depreciation. Assets that cost under $20,000 (excl. GST) and are first used by 30 June 2026 may be immediately written off; assets above that go into the small business pool.

For qualifying small businesses, assets above the write-off threshold enter a small business pool. In that pool, you deduct 15% of the opening balance (plus additions) in the first year, and 30% of the closing balance in later years. This accelerates deductions compared to the general depreciation rules. For certain periods, temporary full expensing and other expensing rules have allowed you to immediately write off the full cost of many new assets, but the key is always to match your claims to the rules that apply in that income year.

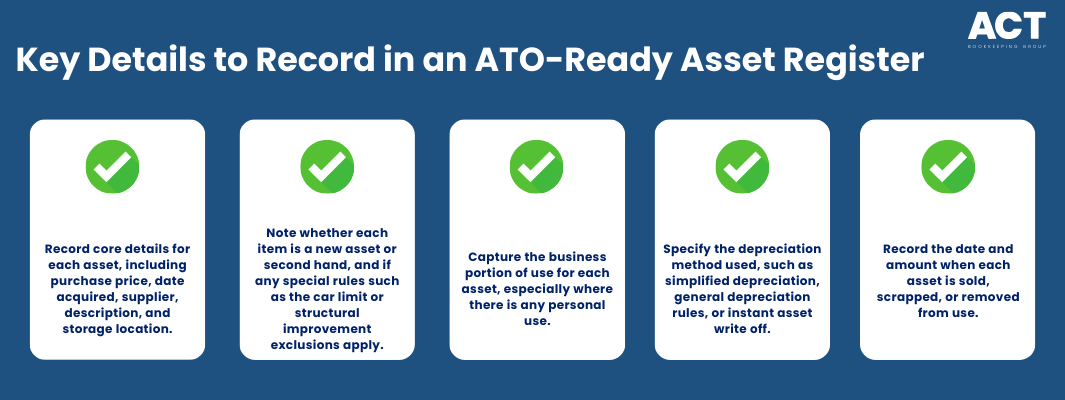

What Information Should You Capture in an ATO-Ready Asset Register?

To keep your asset register aligned with Australian Taxation Office expectations, you should record the core details for every asset you buy. This includes purchase price, date acquired, supplier, description, and where the asset is kept. Record if an asset is new or secondhand and note any special rules (e.g. the car limit for vehicles). Note that capital works (e.g. building or structural improvements) are excluded from immediate write-off and must be depreciated over time, or other rules that affect how you organise expenses for bigger tax deductions.

You also need to record the business portion of use, especially where there is personal use as well. For example, if you use a laptop 80% for business and 20% for personal use, only 80% of the depreciation will be claimed. Finally, your register should include the depreciation method, whether you use simplified depreciation, general depreciation rules, or instant asset write off, and the date and amount when the asset is sold, scrapped, or removed.

How Do You Structure a Practical Depreciation Schedule for Small Business?

A practical depreciation schedule for small business starts by grouping assets based on which rules apply. You might have one section for eligible assets immediately deducted under instant asset write off, another for assets in the small business pool, and another for items using general depreciation. Within each group, you list each asset, its opening value, any additions, and the depreciation deduction for the year.

For assets in the small business pool, you track the opening pool balance, add the cost of new assets, deduct the correct percentage each income year, and show the closing balance. When the pool balance drops below the instant asset write off threshold, you may be able to deduct the full remaining amount in one go. For assets under general depreciation, you follow the effective life and method you have chosen, making sure to calculate the claim correctly each year.

What Is the Difference Between an Asset Register and a Depreciation Schedule?

Your asset register and depreciation schedule are closely linked but serve different roles. The asset register is the detailed record of all assets, including descriptions, locations, purchase price, and business purpose. It is the place you can see every piece of equipment your business owns, from office furniture to coffee machines and structural improvements.

The depreciation schedule, on the other hand, focuses on how those assets affect your tax. It shows how you calculate depreciation deductions under the rules you use, whether that is simplified depreciation, the small business pool, or general depreciation rules. You can think of the register as the data source and the schedule as the calculation summary you rely on when you prepare your tax return.

How Do You Set Up Your Asset Register Step-by-Step?

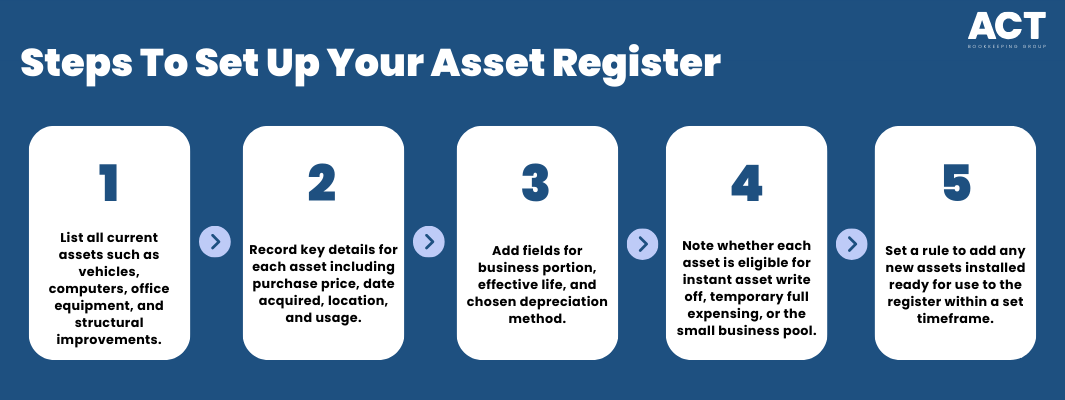

The easiest way to set up your asset register is to begin with your current assets and work backwards. Start by listing all major assets such as vehicles, computers, office equipment, electric sanders, and any structural improvements. Include the purchase price, date acquired, where they are located, and whether they are used only for business or partly for personal use.

Next, add fields for business portion, effective life, and depreciation method, so you can link the register to your schedule and support record keeping as a sole trader. You may also want to include notes on whether each asset is eligible for instant asset write off, temporary full expensing, or needs to go into the small business pool. Once your existing assets are in the register, set a simple rule that any new assets installed ready for use are added within a set number of days, so your records stay current.

How Do You Build a Depreciation Schedule that Matches ATO Rules?

To build your depreciation schedule, you first decide whether you will use the simplified depreciation regime or stick with general depreciation rules. If you use simplified depreciation, you separate eligible assets that can be immediately deducted under instant asset write off from those that must go into the small business pool. For each asset, note the business portion of the cost, so you only claim the correct share.

You then apply the following formula in practice: opening balance plus new additions, minus disposals, multiplied by the correct rate for that pool or asset, which flows through to your overall income tax calculation. For assets that follow general depreciation, you apply the rate based on effective life and method, and you repeat this process across several years. This approach helps you calculate each year’s deductions in a way that lines up with Australian Taxation Office expectations without needing complex calculations every time.

We’re more than bookkeeping experts

As part of ACT Tax Group, we offer complete accounting and business advisory services tailored to your needs.

What Common Mistakes Put Your ATO Compliance at Risk?

Some of the most common issues come from missing or incorrect information rather than the depreciation rules themselves. Business owners sometimes forget to record assets that seem small at the time, such as tablets or office furniture, but these items can add up over several years. Others may immediately write off assets that are not eligible, or forget that the car limit and other special rules can cap the amount they can claim.

Another frequent problem is failing to adjust for personal use, especially for assets like cars, phones, and computers, or misunderstanding how your Australian resident for tax purposes status affects what needs to be reported. If you do not separate the business portion, you can unintentionally over-claim and increase your risk in a review. Inconsistent use of rules is also a trap, such as re-entering assets into the small business pool incorrectly or switching methods without understanding how those changes should be handled, and the same applies to timing-based concessions like the CGT 6-year rule for main residences.

How Can You Keep Your Depreciation and Asset Records Up to Date?

Keeping your records up to date is much easier if you treat asset tracking as an ongoing habit rather than a once-a-year job, supported by practical resources such as our bookkeeping and payroll blog for Australian small businesses. Many business entities set a simple rule that any new assets installed ready for use above a set cost must be added to the register immediately. This includes new assets, second hand assets, and complete sets, such as an entire set of office furniture or a new batch of coffee machines and equipment.

It also helps to review your register and schedule at least once each income year before you finalise your tax return. During this review, check for assets that have been sold, scrapped, or replaced and make sure the value and balance in your small business pool still match your records, particularly where related-party arrangements or Division 7A loans might be involved. By doing this, small business owners with aggregated turnover under the threshold can continue to use simplified rules with confidence, manage related obligations like ATO payment plans for overdue BAS, and claim the right deductions each year.

What Are Your Next Steps to Stay ATO-Compliant?

Setting Up Your Depreciation Schedule and Asset Register for ATO Compliance is really about building a simple, steady process that works for your business size and business turnover. When your asset register is complete and your depreciation schedule correctly applies the rules to asset depreciation, you can claim depreciation with confidence and keep your tax bill under control. This is true whether you are a sole trader running a local service or a growing small business with multiple sites and larger equipment.

Your next steps are to list your current assets, decide whether you will use simplified depreciation or general depreciation, and set up templates that capture the details you need each year. From there, you can decide how to handle instant asset write off, the small business pool, any special rules that apply to your industry and assets, and how you will deal with any future tax debts using ATO payment plans. If you would like friendly, expert support in putting this system in place, our team at ACT Bookkeeping can help you review your current records, calculate your opening pool balance where needed, and design a clear process so you get the full advantage of the rules without extra stress.