Published on 18 Feb 2026

Fringe Benefits Tax (FBT) returns: A bookkeeper’s step-by-step guide to accurate FBT reporting helps you connect an employer’s FBT liability with an employee’s reportable fringe benefits amount (RFBA) when reporting is required. Fringe benefits (for example, a company car) can create an FBT liability for the employer and may also create an RFBA for the employee if the employee’s reportable benefits exceed the reporting threshold. As bookkeepers, we help employers calculate taxable values for the FBT year (1 April to 31 March) and ensure RFBA details are reported correctly via Single Touch Payroll (income statements) or, where STP doesn’t apply, PAYG payment summaries.

What Is Fringe Benefits Tax and Why Does It Matter for Bookkeepers?

Fringe Benefits Tax (FBT) is a tax that an employer pays on certain benefits provided to an employee in respect of their job, rather than being taxed directly in the employee’s wages. These benefits can include a company car available for personal use, expense payments, occasional travel, or other non‑cash perks that have a clear value. While the employee does not pay cash tax on the value of the benefit, the employer is liable for FBT based on the taxable value of the fringe benefits provided.

FBT matters because it directly affects the cost of hiring and retaining staff and the total value of benefits provided over the FBT year. If the employer does not report or calculate the taxable value correctly, they can face penalties and interest, while employees may receive incorrect reportable fringe benefits details on their income statement or employee’s payment summary. For bookkeepers, understanding how FBT interacts with taxable income, assessable income, and tax return reporting is central to managing compliance obligations smoothly.

Struggling to track which benefits are actually reportable for FBT?

Schedule a complimentary consultation with us today to clarify taxable vs exempt benefits and avoid ATO reporting errors.

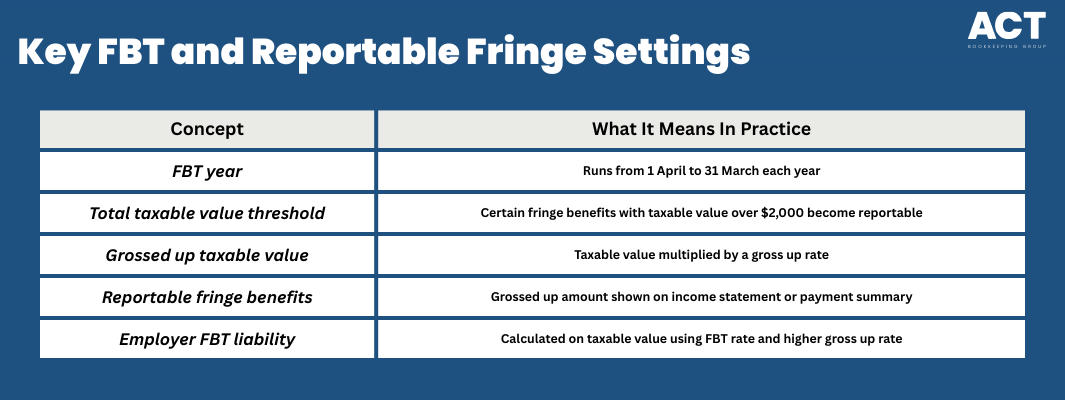

How Does the FBT Year, Gross Up Rate, and Threshold Work?

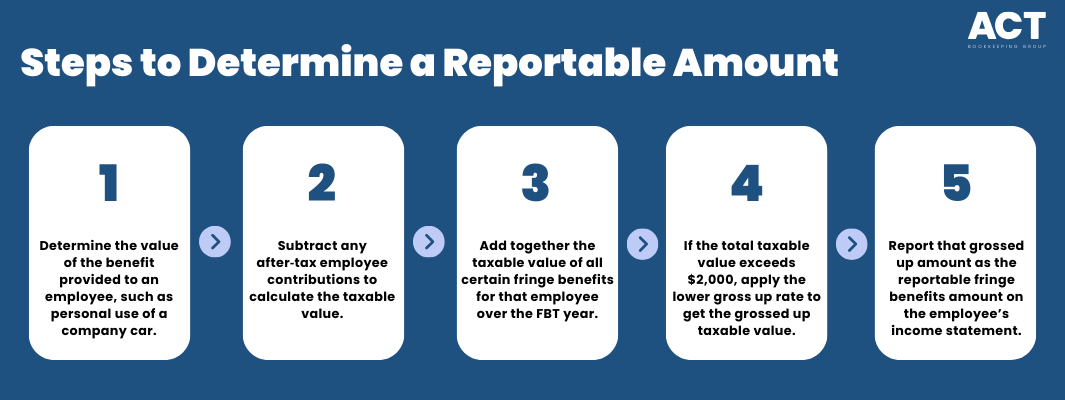

The FBT year runs from 1 April to 31 March, which is different from the standard financial year that runs from 1 July to 30 June. During each FBT year, you measure the total taxable value of fringe benefits provided to each employee or their family member. If certain fringe benefits exceed a total taxable value of $2,000 for an employee in that FBT year, the employer reports the grossed up taxable value as a reportable fringe benefits amount.

To convert taxable value into the employee’s reportable fringe benefits amount (RFBA), you gross up using the Type 2 (lower) gross-up rate. For calculating the employer’s FBT payable, you use Type 1 (higher) for GST-creditable benefits and Type 2 (lower) for other benefits, then apply the FBT rate.

Which Fringe Benefits Become Reportable Fringe Benefits?

Not all fringe benefits are reportable fringe benefits, and this is where good bookkeeping makes a big difference. A benefit is reportable when the total taxable value of certain fringe benefits provided to an employee in an FBT year is more than $2,000 and those benefits are not exempt fringe benefits. Once this happens, the grossed up taxable value of those benefits is shown as the reportable fringe benefits amount on the employee’s income statement or employee’s payment summary.

Common reportable benefits include a company car available for private use and many expense payment benefits. Entertainment needs special care: recreation entertainment benefits can be reportable, but meal entertainment (food and drink) and hiring or leasing entertainment facilities are generally excluded from RFBA reporting when they are not provided through salary packaging. Exempt benefits (such as eligible work-related items and minor benefits) are not reportable.

How Do You Calculate the Taxable Value and Grossed Up Amount?

To calculate the taxable value of a fringe benefit, you start with the cost or value of the benefit provided to an employee and then adjust for any employee contributions. For example, if an employee uses a company car for personal use and makes after‑tax payments towards running costs, those employee contributions reduce the taxable value of that car fringe benefit. The value of the benefit after these adjustments is the taxable value you use for FBT and reporting.

Once you have the total taxable value of certain fringe benefits for an employee across the FBT year, you gross it up using the relevant gross up rate to determine the reportable fringe benefits amount. That grossed up figure is the reportable fringe benefits amount (often shown as the fringe benefits amount RFBA) on the income statement or payment summary. This grossed up amount does not form part of taxable income or assessable income, but it does feed into income tests that adjust things like Medicare levy surcharge, family tax benefit, and other tax offsets.

How Do Fringe Benefits Flow into Income, Tax Returns, and Income Tests?

When an employee receive fringe benefits above the threshold, the employer reports a reportable fringe benefits amount as part of the employee’s end‑of‑year information. This reportable amount shows on the income statement in Single Touch Payroll or on a PAYG payment summary, depending on the payroll system. The reportable amount does not add directly to income tax or taxable income, but it is included in adjusted taxable income used for many income tests.

Government benefits and obligations that rely on adjusted taxable income include family tax benefit, Medicare levy surcharge, child support assessments, and some tax offsets that depend on overall income. Many government income tests use adjusted taxable income (ATI), which includes an adjusted fringe benefits total derived from reportable fringe benefits amounts. This is why an RFBA can affect family assistance and other income-tested payments even though it isn’t taxed as salary. This means that even though reportable fringe benefits are not taxed as cash wages, they can still affect things like whether someone pays the Medicare levy surcharge or qualifies for a specific tax offset.

What Is the Bookkeeper’s Role in FBT, Reporting, and Payroll?

Bookkeepers sit in the middle of the data and play a direct role in correctly capturing fringe benefits and their cost in the accounting records. We ensure that wages, salary, and benefits provided are coded in a way that clearly separates taxable wages from fringe benefits subject to FBT. We also support employers by checking that the value of the benefit and the taxable value have been calculated correctly before the tax agent finalises the FBT return and the end‑of‑year reports.

At year‑end, we help reconcile the total taxable value of fringe benefits with the grossed-up amounts that need to be reported as reportable fringe benefits. We then make sure that the employer reports the correct FBT amounts through payroll, Single Touch Payroll, and any employee’s payment summary. By doing this, we help employees understand why a reportable fringe benefits amount appears on their income statement and how it may affect their tax return, private hospital cover choices, and overall obligations.

We’re more than bookkeeping experts

As part of ACT Tax Group, we offer complete accounting and business advisory services tailored to your needs.

How Do You Keep FBT and Reportable Fringe Benefits Accurate Each Year?

Accuracy starts with clear records of all benefits provided to employees and family members, including any personal use or occasional travel that needs to be counted. Regular reviews of ledger accounts that capture FBT‑related expenses help make sure no benefits are missed and that work related items and exempt fringe benefits are identified correctly. We also check that employee contributions are recorded so that the taxable value is not overstated.

Each financial year and each FBT year, it is important to match the reportable fringe benefits amount reported by the employer with the figures that will be used in income tests and adjusted taxable income. This makes it easier for employees to complete their tax return, understand why a fringe benefits amount RFBA is listed, and see how it may affect things like the Medicare levy, Medicare levy surcharge, or eligibility for certain tax offsets. When your systems reflect the correct total value of benefits and FBT, you reduce surprises and build confidence in your reporting.

How Can ACT Bookkeeping Help You Manage FBT and Reportable Fringe Benefits?

If you are an employer providing perks like a company car, meal benefits, or other fringe benefits, FBT can feel like one more tax you do not have time to manage. Our team can help you determine which benefits are taxable, which are exempt fringe benefits, and when your total taxable value makes certain fringe benefits reportable. We also help you calculate the grossed-up amount, review your FBT year from April to 31 March, and prepare clean data for your tax agent so your obligations are met without unnecessary stress.

We work with you to set up practical processes so that benefits, wages, and pay records reflect the true cost of employment and the value of the benefit provided to each employee. This helps you stay ahead of reportable fringe benefits, understand how they affect your employees’ adjusted taxable income and financial situation, and avoid unexpected impacts on things like private hospital cover decisions, tax offsets, or government benefits. If you want FBT and reportable fringe benefits handled in a straightforward, supportive way, our bookkeeping team in the ACT is ready to help you plan for your next FBT year and beyond.