Published on 11 Feb 2026

Does Your Business Pass The PSI Results Test is a key question if most of your income comes from your own personal efforts rather than selling goods. If your income is considered Personal Services Income, the PSI rules can limit some tax deductions and affect how income is reported. This article gives you a practical checklist to self assess where you stand and what to change in your business contracts.

What Is Personal Services Income and Why Does It Matter?

Personal Services Income (PSI) is income mainly earned from your own personal skills and the work you perform, rather than from business assets or selling goods. This usually applies where an individual generating PSI is paid to provide services and most of the income received is for their labour. When income is considered PSI, the PSI rules can have a significant impact on how your income and deductions are treated.

You have personal services income if more than 50% of income from a contract is for your personal skills or labour. PSI can be earned through a company, trust, partnership, or as a sole trader, but the focus is still on the individual generating PSI. Many professionals, contractors, consultants, and tradies fall into this category without realising it. Knowing whether your income is personal services income PSI is the first step before you look at the several tests used to work out if PSI rules apply.

Unsure if your contracts pass the PSI Results Test?

Schedule a complimentary consultation with us today to review your PSI arrangements and strengthen ATO compliance.

How Does a Personal Services Business Change the PSI Outcome?

If you pass one of the PSB tests, the income is treated as coming from a Personal Services Business (PSB) instead of being caught under the PSI rules. When you are running a personal services business PSB, you can usually claim normal business tax deductions and have more flexibility in how income is shared within your business structure. This is why many professionals focus on whether they can pass the Results Test or one of the other tests.

There are four tests in total: the Results Test, the Unrelated Clients Test, the Employment Test, and the Business Premises Test. You generally start by asking whether you pass the Results Test, because it is the most direct result based test. If you cannot pass the Results Test, you then look at the other tests and, in some cases, a personal services business determination from the ATO.

How Does the PSI Results Test Actually Work?

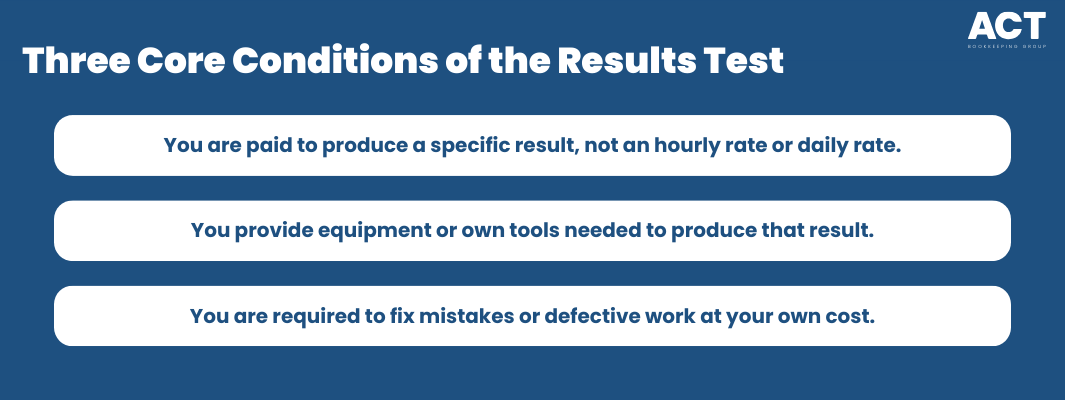

The PSI Results Test looks at whether you are in business to produce a specific result, not just to work a certain number of hours. To pass the Results Test, you must meet three tests for at least 75% of your PSI in an income year. These three tests are about how you are paid, whether you provide equipment, and whether you are required to fix mistakes at your own cost.

If you pass the Results Test, you usually do not need to look at the other tests, and the PSI rules do not apply to that income. If you do not pass the Results Test, it does not automatically mean PSI rules apply, but you must then consider the unrelated clients test, employment test, and business premises test. This is where many professionals benefit from a clear flow chart or checklist to see which path applies.

What Are the Three Tests Inside the Results Test?

Inside the Results Test there are three tests you must satisfy for most of your PSI. First, you must be paid to produce a specific result rather than simply an hourly rate or daily rate for hours worked. Second, you must provide equipment or own tools needed to produce that result where relevant, not rely on the client for everything.

Third, you are required to fix mistakes or defective work at your own cost, which shows you bear real business risk. All three tests must be met for at least 75% of your PSI in the income year for you to pass the Results Test. If one of the following conditions is not met for a large part of your income, you may need to adjust business contracts or consider other tests.

Are You Paid to Produce a Specific Result or Just Hours?

Under the Results Test, a key question is whether you are paid to produce a specific outcome or just for hours worked. If your contract says you are paid an hourly or daily rate under close direction of a client, the income is more likely to be considered PSI that fails the Results Test. In contrast, if you are paid to produce a specific result or completed items, this supports a personal services business position.

A practical way to strengthen your position is to use fixed price quotes or fees tied to a direct result instead of only an hourly rate. For example, you may charge a fixed price for a website build, a project report, or a completed set of services with clear deliverables. You still need to make sure the fixed price reflects the market value of the work performed and that your contracts back this up.

Do Your Business Contracts Show You Provide Equipment and Own Tools?

The second part of the Results Test looks at whether you provide equipment, tools, or other items needed to do the work. If a client provides all tools needed and you simply use their systems, your arrangement looks more like employment. When you supply your own tools and equipment and build those costs into your pricing, it helps show you are operating a business, not another employee.

This does not mean you need heavy machinery in every case. For many professionals, own tools might mean laptops, software, medical equipment, or trade tools that are essential to provide services. Make sure your business contracts meet this test by clearly stating that you provide equipment where required and that your fee takes this cost into account.

Are You Required To Fix Mistakes And Defective Work At Your Own Cost?

The third part of the Results Test looks at whether you are required to fix mistakes at your own cost. If you make an error and the client simply pays you more hours to fix defects, then you may not be taking on true business risk. When you are required to fix mistakes and defective work without extra payment, you are more clearly running a business that stands behind its work.

This is often shown in the contract through warranty or rectification clauses that say you must fix defects or defective work for no further fee. In practice, this might mean returning to fix defects in a renovation or updating a report until it meets the agreed standard. Keeping records when you fix mistakes without extra payment can also help support that your work is paid for a direct result, not just time.

How Do the Other PSI Tests Work If You Do Not Pass The Results Test?

If you do not pass the Results Test, you next look at the other tests to see if the PSI rules apply. These include the Unrelated Clients Test, the Employment Test, and the Business Premises Test. Each of these looks at different outcomes in how you obtain work, who does the principal work, and where the business operates.

The Unrelated Clients Test looks at whether you provide services to two or more unrelated clients and obtain work as a direct result of making offers or advertising to the public. Word-of-mouth referrals alone generally do not satisfy this test. The Employment Test considers whether others perform at least 20% of the principal work, or you employ one or more apprentices for at least half the income year. The Business Premises Test looks at whether you maintain business premises that are physically separate from your home and your client’s premises, used exclusively by you, and used mainly for earning your PSI.

To self-assess using any of these three tests, you must also meet the 80% rule, which means no more than 80% of your PSI can come from one client and their associates in that income year.

What Is a Personal Services Business Determination?

In some cases, you may fail the Results Test and other tests because of unusual circumstances in a particular income year. If most of your income in that year comes from one client due to a one‑off contract, you might not meet the unrelated clients test even though your business is usually more diverse. In these situations, you can ask the ATO for a personal services business determination.

A personal services business determination is a decision from the ATO that your business is a PSB even though strict test conditions are not met for that year. You generally need to show that your business contracts meet the spirit of the rules over a longer period and that any failure is temporary and out of the ordinary. This is a step where professional advice is particularly useful, because the application must clearly explain the background and provide examples.

Practical PSI Results Test Checklist for Your Business

A simple checklist helps you self-assess whether you pass the Results Test across your income year. Go through each contract and ask whether you are paid to produce a specific result, whether you provide tools needed, and whether you are required to fix mistakes at your own cost. Then work out what percentage of your total PSI comes from contracts that meet all three tests.

If you answer “yes” to all of these for most of your income received, you are more likely to pass the Results Test. If not, you may need to adjust how you price your services, how contracts are worded, and how you document your business practices. You can also map these steps in a simple flow chart to help your team follow the same approach each year.

What Happens If PSI Rules Apply And How Do Deductions Change?

When PSI rules apply and you do not pass any PSB tests, some deductions that a business would normally claim may be limited. You may still claim deductions that relate directly to the income and work performed, such as tools, equipment, and costs needed to provide services. However, some other deductions, such as payments to associates for non‑principal work or some business premises costs, may be restricted.

This can have a significant impact on your tax bill if you have set up a company or other business structure expecting to share income or claim broader deductions. It is important to review how PSI rules affect the deductions you claim for each income year, not just once at the start. A clear summary of your deductions and contracts helps you explain your position if questions arise.

It is also worth noting the ATO released PCG 2025/5 in December 2025, which confirms that even if you pass a PSB test, Part IVA anti-avoidance rules may still apply if your arrangement involves income splitting or retaining profits in a company or trust. The ATO expects higher-risk arrangements to move to lower-risk positions by 30 June 2027, so this is something to discuss with your adviser now.

We’re more than bookkeeping experts

As part of ACT Tax Group, we offer complete accounting and business advisory services tailored to your needs.

How Can You Use This Checklist With Professional Advice?

The PSI rules, the four tests, and the way they apply to different outcomes can be complex, especially when you work through several tests at once. Using a clear checklist or simple flow chart helps you self assess before you sit down with your accountant or tax adviser. You can bring copies of your business contracts, invoices, and notes on how you obtain work and who does the principal work.

A trusted adviser can then review whether your business contracts meet the Results Test and other tests, and help you adjust terms where needed. They can also help you confirm whether your income is considered PSI, whether PSI rules apply, and whether a personal services business determination is worth considering. In many cases, a few changes to how you receive payment, how you document cost and equipment, and how you fix defects can make a real difference.

Conclusion: Next Steps to See If You Pass the Results Test

If you are asking “Does Your Business Pass The PSI Results Test,” start by checking whether you are paid to produce a specific result rather than just an hourly or daily rate. Then look at whether you provide equipment or own tools and whether you are required to fix mistakes at your own cost under your contracts. If at least 75% of your PSI for the income year meets these three tests, you are more likely to pass the Results Test and be treated as a personal services business.

If you are unsure, work through the simple checklist, review the other tests like the unrelated clients test, employment test, and business premises test, and gather your documents. Then talk with a professional adviser who understands PSI, PSB tests, and small business tax so they can review your situation in detail. Taking these steps now can help you avoid surprises, protect your deductions, and give you more confidence that your business is on the right track.