Published on 21 May 2026

What Is HECS-HELP and How Should It Appear in Your Payroll and Bookkeeping System? It is a practical payroll and bookkeeping question for Australian employers because Higher Education Contribution Scheme Higher Education Loan Program (HECS-HELP) debts affect Pay As You Go (PAYG) withholding, but they should not be recorded as a normal business loan, staff deduction, or separate bookkeeping liability.

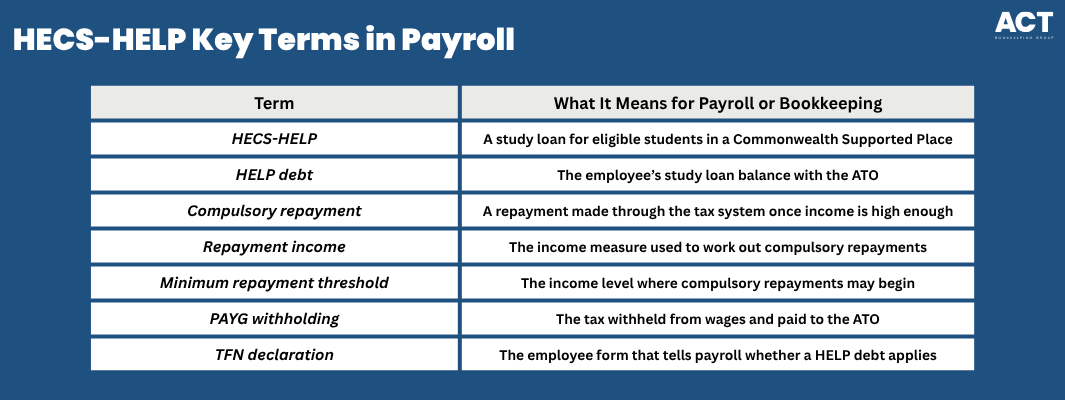

HECS-HELP is a government loan that helps eligible students defer payment of their student contribution amount for higher education. For employers, the important point is simple: the employee’s HECS debt is managed through the Australian tax system, while your payroll system must apply the correct withholding once the employee tells you they have a Higher Education Loan Program (HELP) debt.

Understanding What is HECS-HELP

HECS-HELP is financial support from the Australian Government for eligible students in a Commonwealth Supported Place (CSP). The government pays part of the tuition fees directly to the education provider, and the student can either make an upfront payment or defer payment of their student contribution through a HECS-HELP loan. This means most students do not start repaying the loan immediately. A compulsory repayment applies through the tax system once the employee’s repayment income is above the minimum repayment threshold for the relevant financial year.

For 2025–26, the threshold is $67,000, and repayments are calculated using marginal rates within the broader PAYG withholding framework for Australian employers.

Is HECS-HELP set up correctly in your payroll?

Schedule a complimentary consultation with us today to review your PAYG withholding setup.

HECS-HELP Belongs in Payroll, not as a Separate Bookkeeping Loan

HECS-HELP should appear in payroll as part of PAYG withholding when an employee has declared a HELP debt. It should not usually appear as a separate HECS loan account, employee loan account, or expense account in your bookkeeping system. Your business is not paying off the employee’s loan from the Australian Government. You are withholding tax based on the employee’s Tax File Number (TFN) declaration and payroll settings, then reporting and paying PAYG withholding to the Australian Taxation Office (ATO).

HECS-HELP Works Through Employee Declarations and Payroll Withholding

HECS-HELP allows eligible students to defer their student contribution amount and repay later through the Australian tax system when their repayment income is above the compulsory repayment threshold. The repayment amount is calculated through the Australian tax system using repayment income, which includes taxable income, reportable fringe benefits, total net investment losses, reportable super contributions, and exempt foreign employment income.

For employers, the role is not to calculate the employee’s final HECS debt or decide how much HECS they should repay for the year. Your role is to apply the correct PAYG withholding based on the employee’s declaration and current study and training support loan withholding tables. For 2025–26, updated withholding rates apply from 24 September 2025.

Employees Declare HECS-HELP Through Payroll Forms

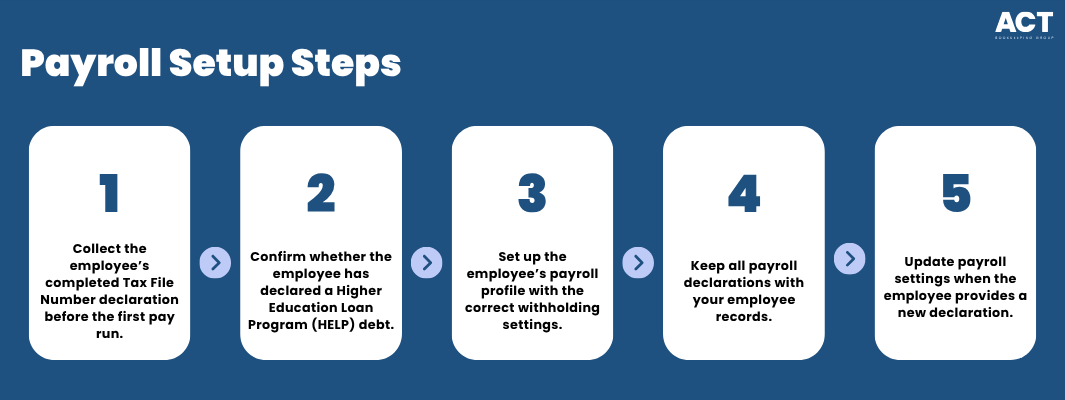

Employees usually tell their employer they have a HECS-HELP loan, FEE-HELP loan, or other HELP loan through a TFN declaration or withholding declaration. These forms help payroll apply the right tax treatment without the employer needing to know the full loan balance. You should not guess whether an employee has a HELP debt, even if they are a recent graduate or work in a higher education field. A simple onboarding process helps you collect the right form, update payroll settings, and keep the record ready for future payroll checks.

HECS-HELP Eligibility Stays Separate from Employer Payroll Duties

HECS-HELP eligibility requirements matter for students, but employers do not need to test whether an employee was eligible for the original loan. Eligibility criteria can include citizenship and residency requirements, enrolment in a Commonwealth Supported Place, being academically suitable, having a valid TFN, meeting genuine student requirements, and submitting the right Commonwealth assistance form by the census date.

Some students may qualify because they meet the relevant citizenship and residency requirements, such as being an Australian citizen, certain permanent humanitarian visa holders, eligible Pacific Engagement Visa holders, or other eligible visa holders. These rules affect the student’s application process with their education provider, not how you record payroll once the employee declares a HELP debt.

HECS-HELP Appears Through PAYG Withholding on Payroll Records

HECS-HELP usually appears through total PAYG withholding rather than as a separate after-tax deduction. The employee’s gross wages are calculated first, then the payroll system applies withholding based on income, tax settings, and any declared HELP debt. Some payroll systems may show a study loan component in reports, while others include it inside total PAYG withholding. Either approach can be workable if the payroll reports, Single Touch Payroll (STP) reporting, payslips, bank payments, PAYG instalments for business or investment income, and ATO records all reconcile clearly.

HECS-HELP Belongs in the PAYG Withholding Account

HECS-HELP generally belongs inside the PAYG withholding payable account, because the employer is withholding tax and paying it to the ATO. It should not sit in a separate liability account for the employee’s HECS loan, because the business does not owe the employee’s study debt. A clean chart of accounts helps your Business Activity Statement (BAS), payroll reports, and balance sheet remain easier to review. It also reduces confusion when reconciling wages, superannuation, net pay, and PAYG withholding obligations at month-end or quarter-end.

HECS-HELP and FEE-HELP Have Different Study Rules but Similar Payroll Treatment

HECS-HELP generally relates to eligible students in a Commonwealth Supported Place, where the Australian Government pays part of the tuition fees and the student pays or defers the student contribution. FEE-HELP can apply to eligible students in a full fee-paying place, where the student may use a FEE-HELP loan for tuition fees up to the applicable HELP loan limit. For payroll, the difference between HECS-HELP and FEE-HELP usually does not change the bookkeeping treatment. If the employee has a HELP debt and declares it, payroll applies the relevant withholding through PAYG withholding.

Employees Start Paying HECS When Income Reaches the Threshold

Employees generally start making compulsory repayments when their repayment income is above the compulsory repayment threshold for the financial year. For 2025–26, no compulsory repayment applies at $67,000 or below. The exact repayment amount is worked out through the employee’s tax return, not by the employer estimating the entire course cost or maximum amount borrowed. Employees can also make voluntary repayments directly to the ATO if they choose. Employers should be careful not to advise employees on whether to make voluntary repayments, because personal income, debt level, indexation, and cash flow can affect that decision.

HECS-HELP Affects BAS and STP Through PAYG Withholding

HECS-HELP affects BAS through total PAYG withholding, not as a separate BAS label or Goods and Services Tax (GST) item. Your BAS should match the PAYG withholding reported from payroll records for the period. For STP, your payroll software reports wage and withholding information to the ATO. Good bookkeeping keeps gross wages, net wages, PAYG withholding, superannuation guarantee obligations, and ATO payments consistent so your records are easier to check.

We’re more than bookkeeping experts

As part of ACT Tax Group, we offer complete accounting and business advisory services tailored to your needs.

Paid-Off HECS-HELP Debts Need Updated Payroll Declarations

Employers should update payroll when the employee provides the correct updated declaration. You should not remove HECS-HELP withholding only because the employee believes the debt is nearly paid off or because a payslip estimate looks high. The employee’s tax return determines their final compulsory repayment for the year. Your bookkeeping responsibility is to keep the payroll record accurate, apply the declaration properly, and retain the paperwork that supports the change.

How ACT Bookkeeping Can Help with HECS-HELP Payroll and Bookkeeping Systems

We help ACT businesses keep payroll, and bookkeeping systems organised, accurate, and easier to reconcile. Our team can review your payroll setup, check that HECS-HELP is handled within PAYG withholding, support BAS preparation, and help keep employee declarations, STP records, and ATO payments aligned. If you are unsure whether HECS-HELP is set up correctly in your payroll software, you can arrange a consultation with our team. We can help you identify practical fixes, improve your bookkeeping process, and reduce the stress that often comes with payroll, BAS, and ATO reporting.

Final Thoughts on HECS-HELP in Payroll and Bookkeeping

HECS-HELP starts as higher education financial support for eligible students, but it becomes a payroll issue once an employee declares a HELP debt. In your bookkeeping system, it should usually be handled through PAYG withholding rather than as a separate loan, deduction expense, or business liability. The safest next step is to review your payroll settings, confirm employee declarations are current, and check that your bookkeeping reports match payroll and ATO records. With the right setup, your BAS, STP, payroll reports, and employee records will be much easier to manage.