Published on 16 Apr 2026

Bookkeeping tasks you must complete before your business goes into liquidation help you stay in control when your company is unable to pay its debts and the winding up process becomes unavoidable. Liquidation is the process of closing a company’s business, selling assets and using the cash received to pay creditors as far as possible. When your records are clear, you give the person appointed as liquidator a better chance to deal with your company’s affairs quickly and help you avoid personal liability where the law allows.

Understanding Liquidation and Your Business

In simple terms, liquidation of a company happens when a company fails and can no longer pay its debts as they fall due, so the company is wound up and eventually dissolved. In most cases this is a creditors’ voluntary liquidation, but a company can also be wound up by the court in a court-ordered liquidation. Court-ordered liquidation often follows action by a creditor, including after non-compliance with a statutory demand, although other applicants may also seek a winding-up order in some circumstances. In all such cases, bookkeeping is central to showing what the company owns, who it owes money to and how the liquidation process should move forward.

If your business is in financial distress or you are seeing clear warning signs, this is the time to get your books in order, not when liquidation begins. Good bookkeeping helps company directors prevent insolvent trading, meet legal obligations under the Corporations Act and work more smoothly with a registered liquidator or other external administrator. Our aim in this article is to guide you through the bookkeeping work you should complete before company liquidation so you can protect yourself and support a fair outcome for your company’s creditors, while also helping you understand the different types of bookkeeping and services available.

Struggling to keep your BAS, PAYG and ATO records up to date before liquidation?

Schedule a complimentary consultation with us today to get all lodgements current and ATO-ready.

What Does Liquidation Mean for Your Bookkeeping and Company Records?

For bookkeeping purposes, liquidation is the process of closing your company, stopping normal trading, and preparing to distribute any remaining assets to creditors. Once a liquidator is appointed, the registered liquidator takes control of the company’s business, books and records and becomes responsible for dealing with the company’s affairs. From that point, company directors lose control of the company’s assets and must support the liquidator with accurate information.

Liquidation can be started in a few different ways. A creditors’ voluntary liquidation is usually started when the company’s shareholders resolve to wind up the company and appoint a liquidator, often after the directors determine the company is insolvent or likely to become insolvent. A court-ordered liquidation starts when an application is made to the court to wind up the company, commonly by a creditor. In some cases, a provisional liquidator may be appointed before the final winding-up order.

Why Must Core Financial Records Be Ready Before Liquidation Begins?

Before liquidation begins, you should make sure your core financial records are complete, so the liquidator can understand your company’s debts and cash position, and consider whether shifting to cloud bookkeeping for small business owners could make maintaining accurate records easier. If your books are incomplete, the liquidator may have trouble tracing transactions, and you could be personally liable for failing to keep proper records. Clean books also support fair treatment of individual creditors and reduce the risk of disputes.

Your records should clearly show the company’s assets, liabilities and equity, along with a history of trading. This matters regardless of whether your company goes into a creditors’ voluntary liquidation, a court-ordered liquidation, or a simplified liquidation where the company meets the eligibility criteria. In all cases, the liquidator reports will rely on your bookkeeping to explain what happened to the company’s affairs over time.

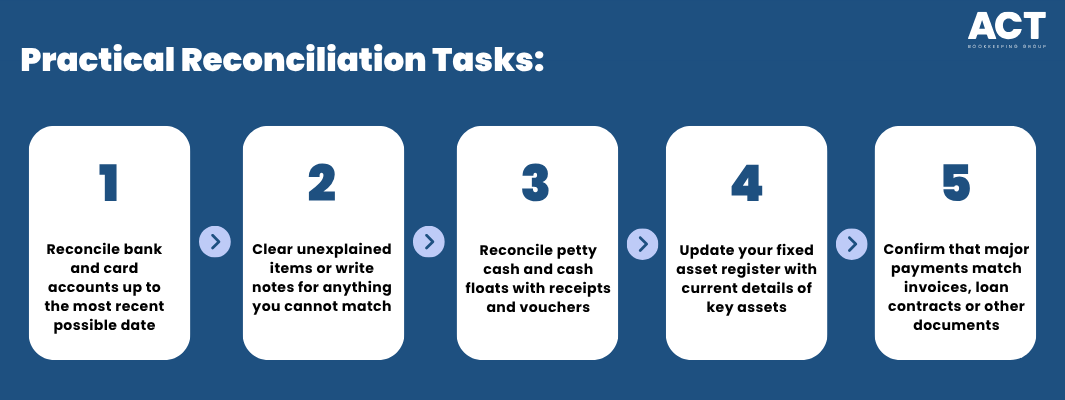

How Should You Reconcile Bank Accounts, Cash and Other Assets?

You should reconcile every bank account, credit card and petty cash fund before the company is wound up. This means matching all transactions to entries in your accounting system so the liquidator can see how much cash received is still in the business and how much has been spent. If the company can no longer pay its debts but the bank reconciliations are not up to date, it becomes harder to track where money has gone.

It is just as important to list other assets, not only bank balances. This includes vehicles, equipment, stock and any other items that can be sold to pay creditors. When the liquidator takes control, they will compare your books with what they actually find, so your bookkeeping should reflect reality as closely as possible.

What Debtor and Creditor Bookkeeping Tasks Should You Complete?

Before liquidation, you should tidy your debtor and creditor ledgers, so they show exactly who owes money to the company and who the company owes money to. This is vital for the liquidation process because creditors are paid from any remaining assets in a set order. Secured creditors generally have rights over secured assets, but distributions in a liquidation are subject to the rules in the Corporations Act, including liquidation costs and priority claims. Employees are priority creditors ahead of ordinary unsecured creditors.

You should prepare a clear aged receivables report and aged payables report. This will help the liquidator understand your company’s creditors, any individual creditor with a large exposure, and whether some debts are unlikely to be collected. It is also important to identify any related‑party balances, such as amounts owed to or from directors in their own name.

Why Is Updating Tax, BAS and ATO Records Essential Before Company Liquidation?

Before company liquidation, you should bring your tax and BAS records up to date, even if you cannot pay the full amounts due, and make sure you understand your key business tax obligations in Australia. Many companies in financial difficulty carry tax debts such as GST, PAYG withholding and income tax, and these must be clearly recorded in your books. Having accurate figures helps the liquidator and the ATO understand the size of your company’s debts and where the company stands.

If your company has missed lodgements, this can create serious consequences, including estimates and extra charges, especially when your BAS preparation and lodgements have fallen behind. It is better to work with your bookkeeper to prepare and lodge overdue BAS and returns before liquidation than to leave gaps in your records. Doing so also shows you are doing what you can to meet your legal obligations as a director.

Important tax‑related tasks:

Reconcile GST, PAYG and other tax accounts to your BAS and ATO statements

Prepare and lodge any outstanding BAS, IAS and company tax returns, understanding the difference between IAS and BAS obligations

Gather all ATO letters, payment plans and notices relating to tax debts

Make sure your accounting system reflects all tax instalments already paid

Check that your business name, ABN and other details are correct and current

How Should You Prepare Payroll, Unpaid Wages and Other Entitlements?

Employee records are a major focus in any company liquidation, especially when there are unpaid wages or other entitlements. Your bookkeeping should clearly show what each employee is owed, including wages, super, annual leave, long service leave and any redundancy or notice pay. If the company enters liquidation, some employee claims may rank as priority claims, and unpaid super may involve separate ATO and insolvency processes. For many distressed businesses, outsourcing bookkeeping services to a specialist team can help keep payroll and entitlement records accurate before issues escalate.

This information helps the liquidator work out outstanding employee entitlements and whether eligible workers may be able to seek assistance under the Fair Entitlements Guarantee (FEG) for certain unpaid entitlements.

If payroll records are messy or incomplete, employees may miss out on amounts they are due, or the process of working it out may take much longer. As company directors, you also need to show that you have taken reasonable steps to keep accurate payroll and super records. Clear records are especially important where the company cannot pay all wages before liquidation begins.

Payroll bookkeeping tasks:

Reconcile wage, super and PAYG totals to bank payments and ATO records

Prepare a list of unpaid wages, leave balances and other entitlements for each employee

Check that Single Touch Payroll reports match your payroll ledger

Identify any personal guarantees given by directors, shareholders or related parties on company borrowings, leases or trade accounts

Keep copies of contracts, awards and policies that affect entitlements

What Does Liquidation Mean for Inventory, Selling Assets and Distributing Assets?

For companies with stock or other trading assets, the bookkeeping around inventory is critical. Your stock records should show what is on hand, what has already been sold, and what is obsolete or damaged. This helps the liquidator decide the best way of selling assets to raise money and pay creditors.

Any plan to liquidate money tied up in assets should be handled carefully at this stage. Selling assets too quickly or at under value before a formal process may raise questions, especially if certain creditors or related parties seem to be favoured. In well‑run cases, the liquidator will manage distributing assets and the proceeds in line with the Corporations Act, using your records as a starting point.

How Do Director Duties, Insolvent Trading and Personal Liability Link to Bookkeeping?

Under the Corporations Act, company directors must not allow a company to keep trading when it is an insolvent company that cannot pay its debts when due. If they do, they may be personally liable for certain debts due to insolvent trading. Good bookkeeping helps you monitor your company’s financial difficulty and make informed decisions before things reach that point.

Accurate records give you and your advisers a clear view of whether the company can pay its debts and what options exist, such as voluntary administration or some form of voluntary liquidation. If you ignore warning signs and fail to keep proper records, you increase the risk of being personally liable and facing serious consequences when a liquidator reviews the company’s affairs.

We’re more than bookkeeping experts

As part of ACT Tax Group, we offer complete accounting and business advisory services tailored to your needs.

How Long Do Business Records Need to Be Kept Around the Winding Up Process?

Record‑keeping rules do not disappear once the company winding up process starts. Even when a company is in liquidation, there are still minimum time frames for keeping business records. Directors, and later the liquidator, are expected to keep key documents for several years after the company is dissolved.

Tax records are commonly required to be kept for at least 5 years, while company financial records under the Corporations Act are generally required to be kept for 7 years. During and after an external administration, the last external administrator must generally keep the company’s books and records for 5 years from the end of the external administration. Your job as a director is to make sure everything is handed over in good order so those obligations can be met.

What Is the Difference Between Voluntary Liquidation, Court Liquidation and Other Options?

When your business is in financial distress, there are several formal paths that may be open, and good bookkeeping helps you and your advisers choose the right one, including whether voluntary administration for SMEs is more appropriate than immediate liquidation. A creditors’ voluntary liquidation is used when an insolvent company cannot pay its debts and directors and creditors agree to wind it up. A court-ordered liquidation happens when a creditor, often owed money under a statutory demand, applies to the court to have the company wound up.

There are also paths for solvent companies, such as members’ voluntary winding up, which requires a declaration of solvency by the directors. In other cases, voluntary administration or simplified liquidation may be options for certain small businesses. Whichever path you take, clean books make the process smoother and help directors assess risk early, but they do not remove existing personal exposure, including liabilities arising from insolvent trading, personal guarantees, or director penalty rules.

How Can a Bookkeeper Help You Avoid Personal Liability and Support a Smoother Process?

A skilled bookkeeper can help you organise the records and reporting needed to prepare for liquidation and help you understand issues that may affect personal liability. They can work with your accountant, solicitor and any appointed external administrator to bring your books up to date quickly. In many cases this includes cleaning up years of backlogs, reconciling key accounts and preparing tailored reports for a registered liquidator.

If your company is unable to pay its debts, you should not wait until a statutory demand arrives or a creditor starts court action before seeking help, or to explore options like setting up and managing an ATO payment plan to deal with tax arrears. Early support can give you more options, including the chance to save parts of the business or, if that is not possible, to close in an organised way that respects your company’s creditors and staff. For some directors, this may help them better understand and manage the flow-on risk created by personal guarantees.

Conclusion

If your business is in financial difficulty and you are worried you can no longer pay your debts, now is the time to act. Liquidation of a company is a serious step, but with the right bookkeeping support you can move through the process with clearer information and less stress. You cannot change the past, but you can choose to face the winding up process with organised, honest records and a clear understanding of your legal obligations.

Our team in the ACT works with small and medium businesses that are under pressure from creditors, tax debts or cash flow problems, including those needing support to manage ATO payment plans for overdue BAS. We help you get your books in order, explain what bookkeeping tasks you must complete before your business goes into liquidation, and connect you with trusted advisers when other steps, like voluntary administration or formal liquidation, are being considered. If you are ready to talk about your company’s situation, we are here to support you with calm, professional guidance.