Published on 24 Dec 2025

Partnership Accounting in Australia: Tax, Profit Sharing, And Compliance Made Simple helps business partners understand how a partnership works without getting lost in technical details. A partnership is a business structure where two or more people carry on a business together and share profits, risks, and responsibility. With a clear written partnership agreement, good records, and the right support, business partnerships can manage income tax, Goods and Services Tax, and reporting with confidence.

A partnership is not a separate legal entity for income tax purposes, but it is treated as a separate entity for GST. The ATO still requires partnerships to have their own TFN and ABN, and to lodge an annual partnership tax return. The firm itself does not pay income tax on the partnership income, but it must lodge a partnership tax return and show how the partnership’s profits are shared. Each partner pays tax in their own tax return on their partners share of the net income, based on their own tax rate.

What Is a Partnership Structure in Australia?

A partnership structure is a business arrangement where two or more individuals carry on a business as business partners with a view to profit. In a general partnership or general law partnership, partners are equally responsible for the partnership’s debts and may be personally liable with unlimited liability. This means partners personal assets can be used to pay the partnership’s debts if the business cannot pay.

Partnerships are common law jurisdictions business structures and are often used by professionals, family partnership businesses, and small firms. The maximum number of partners in a standard partnership is usually twenty, although some professions have specific rules. An incorporated limited partnership or limited partnership can offer limited liability to limited partners, but general partners in those structures can still be personally liable.

Worried about getting your partnership tax returns right?

Schedule a complimentary consultation with us today to review your partnership profit allocations and ATO reporting obligations.

How Does Partnership Tax Work in Australia?

A partnership must apply for its own Tax File Number and an Australian Business Number (ABN) if it is carrying on a business. The partnership tax return shows total income, allowable deductions, and the partnership’s profits or loss for the year. It also shows how the firm will distribute income between individual partners, including equity partners, salaried partners, and any silent partner.

The partnership itself does not pay income tax on the partnership income. Instead, one or more partners include their partners share of the net income in their own tax return. Each partner pays tax on that income according to their own tax file number record and rate, even if the partnership does not actually pay out all of the cash in that year.

What Registrations Does a Partnership Need?

A partnership carrying on a business needs its own Tax File Number and Australian Business Number. It also needs a business name registration if it trades under something other than the personal names of the partners. Where annual turnover meets the $75,000 GST registration threshold (or $150,000 for non-profits), the partnership must register for Goods and Services Tax and lodge regular BAS returns.

Each partner still needs their own tax file number for their own tax return and other forms of personal tax reporting. The partnership may also need to register for pay as you go obligations if it has employees. These obligations sit alongside the need to keep accurate records so that the partners can show the Australian Taxation Office how amounts were calculated.

How Does Profit Sharing and Income Allocation Work?

The partnership agreement sets out how the firm will share profits and losses between partners. If there is no written partnership agreement, the general law partnership default is often that profits and partnership income are shared equally between two or more people, even if one partner does more work. This can cause tension between business partners if the partners share does not feel fair.

A clear written partnership agreement can set out different methods of sharing profits and losses, such as fixed percentages, capital-based splits, or performance-based amounts. It can also describe how the firm will treat drawings, partner “salaries”, and any special rights for equity partners, salaried partners, or other partners. This helps individual partners understand their obligations and what they can expect from the partnership’s profits.

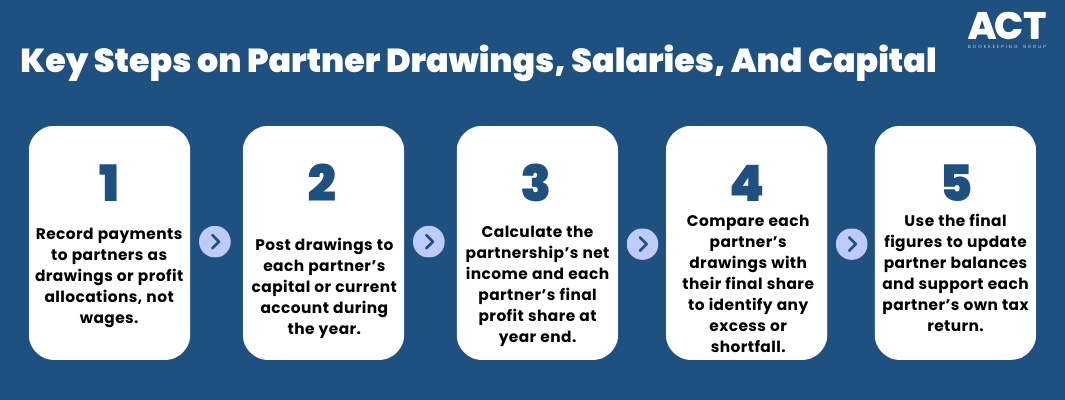

How Are Drawings, Salaries, And Capital Treated?

In a partnership, payments to partners are usually treated as drawings or profit allocations rather than wages paid on behalf of the firm. These amounts do not change the overall net income of the partnership, but they affect each partner’s current balance. Drawings are recorded against each partner’s capital or current account and compared with the final partners share at year end.

A partnership usually keeps separate records for each partner, showing capital introduced, drawings, share of profits, and closing balances. This helps the partners see whether one partner has taken more out of the firm than their share of the partnership income. It also supports the information that each partner uses in their own tax return.

What Is the Difference Between Partnership Types?

A general partnership or general law partnership is the most common structure, where all partners are equally responsible for management, profits, and liability for the debts. In this type of partnership structure, partners can be personally liable and face unlimited liability for the partnership’s debts. The law allows creditors to pursue one partner or more partners for the full amount if the firm cannot pay.

In a limited partnership or incorporated limited partnership, limited partners have liability limited to the amount they contribute and cannot take part in day-to-day management. At least one general partner must have unlimited liability and management control. General partners in that structure usually keep management control and may still be personally liable. Some partnerships also refer to equity partners, salaried partners, or silent partner roles to describe different rights to profits, management, and risk.

How Does Goods and Services Tax Apply to Partnerships?

If a partnership’s annual turnover is $75,000 or more (or $150,000 or more for non-profits), it must register for GST. Taxi and ride-sharing services must register regardless of turnover. The partnership then needs to collect services tax on taxable sales, lodge regular returns, and pay the net amount to the Australian Taxation Office. This applies whether the partnership has one partner receiving most of the income or many partners.

The partnership must keep records of GST collected and credits claimed on business expenses. These records help the firm work out its obligations and show that it has met its responsibilities. Good systems also make it easier for partners to understand how GST affects the cash flow of the business.

What Are the Main Risks and Liabilities in a Partnership?

In most partnerships, partners are equally responsible for the partnership’s debts and obligations, even where only one partner signed a contract. This shared responsibility is one of the biggest differences between a partnership and a company, which is a separate legal entity. If the partnership cannot meet its debts, creditors may look to the partners personal assets to recover what is owed.

This risk makes it important to think carefully about the partnership structure and the terms of the partnership agreement. Some business partners consider a company or other forms of structure if they want more protection and limited liability. Others use a family partnership or different combinations to balance control, tax benefits, and risk.

Why Is a Written Partnership Agreement Essential?

A written partnership agreement sets clear rules about how the firm will be run. It can cover management roles, how decisions are made, how profits are shared, and what happens if one partner wants to leave. Without a clear agreement, partners may end up relying on general law rules that do not match what they expected.

The agreement can also outline what happens if one partner dies, becomes ill, or stops working in the business. It should describe how to value the business, how to handle partners personal assets used in the firm, and how to deal with disputes. Having these points agreed in advance can protect both the business and the customer base.

We’re more than bookkeeping experts

As part of ACT Tax Group, we offer complete accounting and business advisory services tailored to your needs.

How Should Partnerships Handle Everyday Accounting and Tax?

Good bookkeeping helps business partnerships track income, expenses, and partners share of profits. Using simple systems and regular reports makes it easier to see how the business is performing and what tax may be due. This also supports the information that must go into the partnership tax return and each partner’s own tax return.

Regular checks of bank accounts, customer payments, and bills help make sure that the records match reality. Clear records also make it easier to show the Australian Taxation Office how figures were calculated if questions arise. With the right support, a partnership can handle its obligations without stress and focus on growing the business.

When Should a Partnership Seek Professional Support?

A partnership should seek professional help when setting up the structure, drafting a partnership agreement, or changing profit sharing. Support is also useful when deciding between a general partnership, limited partnership, or other forms of business structure. Lodgement deadlines vary: if you lodge through a registered tax agent, you may receive an extended deadline. Otherwise, the due date is generally 31 October but confirm your specific due date with the ATO or your agent. Getting advice early can help partners understand tax benefits, risks, and obligations before they commit.

Professional guidance is valuable before major changes, such as bringing in new partners, selling the business, or moving to a company structure. An adviser can also help review whether the firm is meeting all registration and reporting requirements, including Goods and Services Tax (GST). This reduces the chance of unexpected tax bills and issues later.

How Can ACT Bookkeeping Support Your Partnership?

ACT Bookkeeping helps business partnerships put practical systems in place so that day to day accounting and tax are easier to manage. Support can include setting up a simple chart of accounts, tracking each partners share, and preparing information for the partnership tax return. This gives partners a clear picture of income, debts, and obligations throughout the year.

Working with a local team familiar with partnerships and the law in the ACT means you do not have to understand the rules alone. With the right structure, agreement, and processes, your partnership can focus on building a strong customer base and growing profits. Partnership accounting in Australia really can be made simple when you have clear information and steady support.