Published on 19 Nov 2025

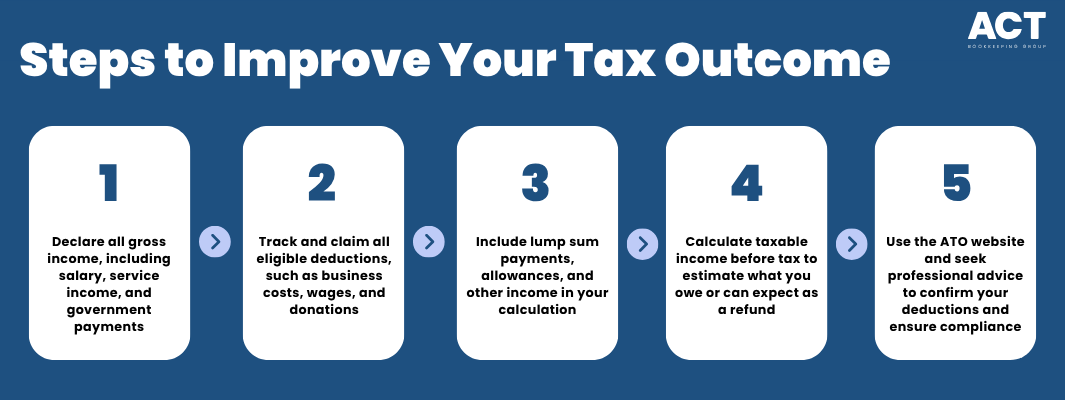

Understanding taxable income for small businesses in Australia begins with this: taxable income is the amount before you pay tax or the income tax is applied. It is calculated by taking your gross income, including wages, salaries, business services, and other money received during the income year, and then subtracting allowable deductions such as business expenses incurred to earn this income. For tax purposes, this is the crucial number that determines how much tax you owe and what you can expect when you lodge your tax return or pay income tax for your business.

This matters for Australian residents and business owners because it affects everything from hhow much tax you pay, your eligibility for the tax-free threshold if you are an individual, the impact of lump sum payments, and whether your taxable income means you need to pay the Medicare Levy or the Medicare Levy Surcharge, which apply only if you exceed certain income thresholds. Most taxpayers in Australia, especially small business owners, want clarity on how to calculate taxable income, what counts as a deduction, which payments to declare, which expenses directly reduce taxable income, and whether they can claim benefits like tax offsets or tax-free amounts.

Is Taxable Income Before or After Tax in Australia?

Taxable income is always calculated before you pay income tax. It is not your take-home pay, but rather the figure used to work out how much tax, including the Medicare Levy, will apply. The Australian Taxation Office uses this number as the starting point when assessing tax returns for most people in Australia.

It covers all your gross income, such as salary, other income, or business payments, less any allowable deductions for expenses incurred. This means your taxable income determines how much tax is payable and whether you’re entitled to any tax offsets or rebates. Lump sum payments, government payments, and allowances may have special rules—check how each should be reported for your situation.

Do you know which business expenses reduce your taxable income?

Schedule a complimentary consultation with us today to maximise your deductions and lower your tax bill.

Why Is Understanding Taxable Income Important for Small Business Owners?

Comprehending taxable income provides small business owners in Australia with control over how much tax they pay, gives access to rebates and benefits, and avoids unexpected bills from the Australian Taxation Office. This insight assists people to claim all allowable deductions and maximise their tax refunds, and for eligible taxpayers, helps to reduce what is payable.

If you don’t understand how to calculate taxable income, you risk missing out on deductions, not declaring necessary amounts, or making costly mistakes in your tax return. Most taxpayers rely on the correct calculation for both compliance and for estimating what they may owe or be entitled to receive.

How Do You Calculate Taxable Income For Small Business?

To calculate taxable income, add up all your gross income for the financial year – including salary, money from business activities, investments, lump sum payments, and any allowances. Subtract all allowable deductions, such as the cost of goods sold, expenses incurred running your business, and eligible donations or rebates.

The calculation is straightforward:

Taxable Income = Gross Income − Allowable Deductions

What Types of Income Should Be Included in Taxable Income?

For small businesses, taxable income should include sales income, payments for services, investment returns, and for unincorporated businesses like sole traders or partnerships, all net profits after expenses (not ‘salary’ which is your own drawings). Depending on your employment and business structure, you’d also need to declare professional fees, service payments, allowances, and other forms of compensation.

Do not forget to include income derived from overseas services if you are an Australian resident for tax purposes. Individuals must include bonuses, lump sum payments, and any benefits in their income; for businesses, check whether lump sums require separate reporting under ATO guidelines.

What Deductions Can Reduce Your Taxable Income?

Allowable deductions are costs you incur to earn your income, such as business expenses, professional advice fees, wages paid to staff, charitable donations, and the cost of maintaining employment-related assets. These deductions directly reduce your taxable income and therefore cut down how much tax or Medicare Levy you pay.

Eligible expenses can include accounting costs, office rent, depreciation of equipment, certain government payments, and interest on loans taken for business purposes. For each dollar you deduct, your taxable income and ultimately your tax payable drop by the corresponding amount.

Business-related expenses

Depreciation on vehicles and equipment

Employee salaries and wages

Professional advice, accounting, or legal fees

Eligible donations to approved charities

Expert tip: Always keep receipts and detailed records of all costs and deductions you claim, as the ATO may require evidence during a review. For assets acquired and first used or installed ready for use from 1 July 2024 to 30 June 2025, eligible small businesses can claim an instant asset write-off up to $20,000 per asset.

We’re more than bookkeeping experts

As part of ACT Tax Group, we offer complete accounting and business advisory services tailored to your needs.

How Does Taxable Income Affect Tax Rates, Medicare Levy, and Offsets?

The taxable income you report determines the tax rates that apply, how much tax and medicare levy you need to pay, and whether you can access tax offsets or rebates. Individuals in Australia pay tax on a sliding scale, with the Medicare Levy and Medicare Levy Surcharge added if their income exceeds set thresholds; companies pay a flat tax rate, currently 25% for small businesses.

Some individuals and businesses qualify for reduced rates, government offsets, or rebates if their taxable income is below specific limits. Claiming allowable deductions and offsets can directly reduce the tax you pay, and for some, increase the potential for a tax refund at the end of the income year.

Conclusion

Understanding taxable income as the amount before tax is applied lets you manage your tax, grab every allowable deduction, and meet your obligations to the Australian Taxation Office. Accurately calculating your income ensures your tax refund or payment matches what you owe and supports your business’s financial stability.

If you want support, review your account, or get the most you’re entitled to, seek professional advice or consult the ATO website for current rates. With the right knowledge, your business can benefit from smarter planning, fewer surprises, and real peace of mind at tax time.