Published on 22 Oct 2025

If you’re a small business owner looking to pay less tax while building your retirement savings, salary sacrifice for super is one of the smartest ways to do it. This simple tax strategy can help reduce your taxable income, boost your superannuation fund, and improve your long-term financial wellbeing.

Understanding How Salary Sacrifice Works

Salary sacrifice, sometimes called salary packaging, is when an employee agrees to receive less take-home pay in exchange for their employer paying the same amount into their superannuation fund or towards certain benefits. For small business owners who pay themselves a salary, this strategy allows you to direct pre-tax salary into super and reduce your assessable income.

Worried about exceeding super contribution caps?

Schedule a complimentary consultation with us today to track and improve your super contributions under ATO rules.

What Happens in Practice

Here’s how salary sacrifice work: you choose to give up part of your before-tax salary, known as pre-tax dollars, and this amount is paid into your complying super fund as an additional employer contribution. These contributions are generally taxed at 15% inside your super, which is often less than your marginal tax rate. This means you pay less income tax while saving more for retirement.

For example, if your total salary is $100,000 and you salary sacrifice $10,000 into your super, you’ll only pay income tax on $90,000. The $10,000 is taxed at the concessional rate within your super instead of your standard rate, helping you pay less tax overall.

Why It’s Useful for Small Business Owners

As a small business owner, you often manage irregular income and multiple priorities. Salary sacrificing super gives you flexibility — you can make larger before-tax contributions when business performance allows or scale back during quieter months. It also helps keep personal and business finances separate while growing your retirement savings in a tax-effective way.

The Tax Benefits of Salary Sacrificed Super Contributions

Salary sacrifice contributions deliver two main advantages: reducing your taxable income and growing your super through concessional contributions.

Pay Less Income Tax

By directing part of your pre-tax salary into your super account, you immediately reduce your taxable income. Because your super fund pays only 15% tax on concessional contributions, this is usually less than the tax you’d pay on your salary. It’s particularly beneficial if your marginal tax rate is higher than 15%.

Over time, this can translate into thousands of dollars in tax savings and a stronger retirement balance, making salary sacrifice a reliable way to pay less tax while preparing for the future.

Claiming Employer Contributions and Deductions

Under a valid salary sacrifice arrangement, the employer contributions you make to your super fund are tax deductible to your business. This means your business benefits as well. As a small business owner, you can treat sacrificed salary as part of total remuneration packaging and record it in the employee’s payment summary.

You can also combine salary sacrifice with additional voluntary super contributions or employer super contributions through the Super Guarantee (SG) system to build further savings.

Contribution Limits and ATO Compliance

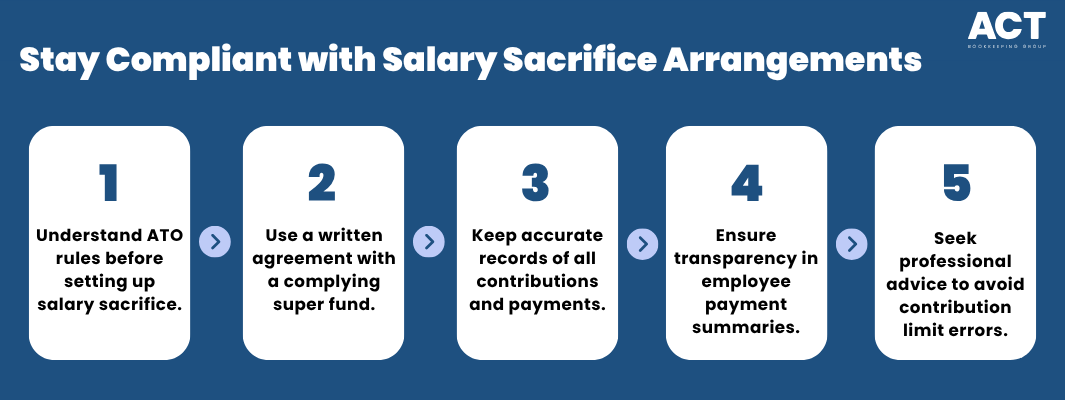

Salary sacrificing super is flexible, but there are rules to follow to ensure you stay within the law and avoid extra tax.

Understanding the Contribution Caps

For the 2025–26 financial year, the concessional contributions cap is $30,000. This cap includes super guarantee contributions, salary sacrificed super contributions, and any other before-tax contributions.

If you’ve contributed less than the maximum cap in previous financial years, you might be able to use your unused concessional cap amounts for up to five years, provided your total super balance is under $500,000. Exceeding the cap can lead to additional tax being applied to the excess amount.

Keep Your Arrangement in Writing

The ATO requires that all salary sacrifice arrangements be formalised before contributions are made. This written agreement between the employer and employee should clearly state the amount or percentage to be sacrificed from the before-tax salary. This ensures each payment to your super fund is considered a legitimate salary sacrifice contribution, compliant with tax rules.

Maximising the Benefits of Salary Sacrifice

Salary sacrificing super isn’t just for big companies — it’s one of the most tax-effective options available to small business owners too.

Start Small and Build Gradually

If your business has variable income, begin with a modest amount of salary sacrifice. Even steady, smaller before-tax contributions can deliver significant benefits over time. As business performance improves, you can increase your contributions within your concession caps.

Combine with Other Tax Strategies

Salary sacrifice can work alongside other superannuation and tax planning opportunities, such as making after-tax voluntary contributions, claiming a government co-contribution, or making contributions for your spouse. These can help you take advantage of every available benefit while keeping your taxable income lower.

Understand Fringe Benefits Tax Implications

While most salary sacrifice contributions to super are exempt benefits and won’t trigger Fringe Benefits Tax (FBT), other forms of salary packaging such as school fees, childcare costs, or loan repayments can attract FBT. Business owners should be cautious about these types of benefits and seek advice before offering them to employees or claiming them as deductions.

We’re more than bookkeeping experts

As part of ACT Tax Group, we offer complete accounting and business advisory services tailored to your needs.

Staying Compliant and Informed

A clear understanding of how salary sacrifice works helps you stay compliant with ATO guidelines and avoid unintended costs. Contributions to a complying super fund under a written salary sacrifice agreement generally qualify for a tax deduction for your business while not affecting your super guarantee contributions.

Record-Keeping and Transparency

Always keep detailed records of sacrificed salary amounts, employer contributions, and any employee contributions made to your super fund. This ensures accuracy for reporting, income tax assessments, and payroll audits.

Your employee’s payment summary should clearly show the reduced salary and any employer super contributions made on their behalf. Transparency not only helps maintain compliance but also builds better financial management habits.

Get Professional Help

Before starting or adjusting a salary sacrifice arrangement, seek financial advice from a qualified accountant or bookkeeper. They can ensure your strategy stays within contribution limits, meets ATO requirements, and supports your retirement goals.

Final Thoughts

Salary sacrificing super is one of the simplest and most effective tax strategies for small business owners. By contributing part of your pre-tax salary to your super fund, you can reduce your taxable income, pay less tax, and secure a more comfortable retirement.

When set up properly, salary sacrifice work allows your business to grow while your super grows alongside it. Just remember to monitor your contribution caps, finalise your arrangement in writing, and ensure your super fund is compliant.

At ACT Bookkeeping, we work with small business owners across the ACT to make salary packaging, super contributions, and tax management simple and rewarding. Our team can help you create a tax-effective plan that balances your cash flow, business success, and future performance.