Published on 15 Oct 2025

Learning how to estimate your business tax return accurately is crucial for Small and Medium-sized Entities (SMEs) planning their finances in Australia. This guide provides clear steps to calculate your tax payable, understand your potential tax refund, and use helpful tools like a tax calculator to forecast your obligations. You’ll discover practical methods to determine your taxable income, claim appropriate deductions, and understand the current financial year with confidence.

Understanding Your Tax Obligations and Calculator Results

Before diving into calculations, it’s important to understand what affects your tax bill and how different circumstances impact the amount of tax you need to pay. Your residency status, business structure, and income sources all influence your final tax payable.

Every business must report income and expenses to determine their tax position. The ATO provides various tools, including online calculators, to help estimate your tax liability. These calculator results give you a starting point for planning, though your actual tax return may differ based on specific details and deductions you’re entitled to claim.

Your employer may withhold tax from wages if you’re also an employee elsewhere. Understanding what’s been withheld helps you calculate whether you’ll receive a refund or need to pay when you lodge.

Struggling to reconcile your income data across tax and BAS reports?

Schedule a complimentary consultation with us today to align your reporting and prevent ATO audit triggers.

Step-by-Step Process to Calculate Your Estimated Tax

This section breaks down the estimation process into manageable steps. Each component builds to give you a complete picture of your tax position.

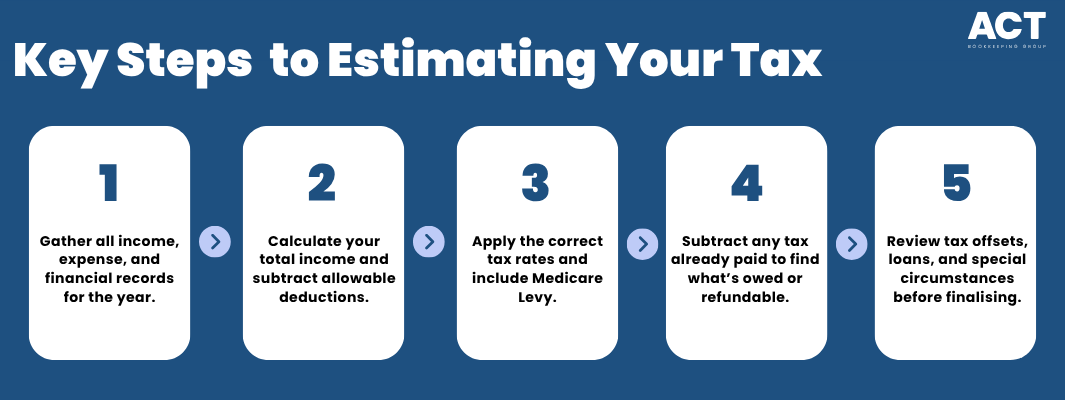

Gather Your Financial Details and Account Records

Start by collecting all relevant financial information from the current financial year. This includes bank account statements, invoices, receipts, and records of payments received. Having complete details ensures your estimate reflects your actual circumstances.

Your records should cover all income sources, not just primary business revenue. Include other income such as interest earned, dividends, rental income, or government payments. These amounts contribute to your total assessable income for tax purposes.

Document all business expenses throughout the year. Regular record-keeping makes the estimation process smoother.

Calculate Your Total Income and Taxable Income

Begin with your gross income from all sources during the financial year. This includes business revenue, wages if you’re employed elsewhere, investment returns, and any other income you’ve received.

From this total, subtract allowable deductions to arrive at your taxable income. Business deductions might include office rent, equipment costs, vehicle expenses, professional development, and marketing costs. Each deduction must be directly related to earning your income.

Remember that some expenses have specific rules. For example, vehicle costs can be calculated using either the cents per kilometre or logbook method.

Apply Tax Rates and Calculate Tax Payable

Once you know your taxable income, apply the relevant tax rates. Sole traders use individual income tax rates, while companies typically pay a flat rate of 25% for eligible businesses. Your tax agent can help determine which rates apply to your circumstances.

Don’t forget to include the Medicare Levy in your calculations. Most Australian residents pay this additional amount based on their taxable income. Some people may also need to pay the Medicare Levy Surcharge if they don’t have private health insurance and earn above thresholds.

Calculate your total tax liability, then subtract any tax already withheld or paid through instalments. The result shows whether you’ll receive an estimated tax refund or need to pay additional amounts.

Consider Tax Offsets and Special Circumstances

Tax offsets directly reduce the amount of tax you need to pay, dollar for dollar. Common offsets for small businesses include the small business income tax offset and various industry-specific concessions.

If you have Higher Education Loan Program (HELP) or Trade Support Loan debts, these may affect your final tax bill. The ATO calculates additional amounts based on your income level, which reduces any refund or increases the amount you need to pay.

Review your circumstances for changes during the year. Starting or selling a business or capital gains from asset sales can impact your tax position.

Tools and Resources to Simplify Your Tax Estimation

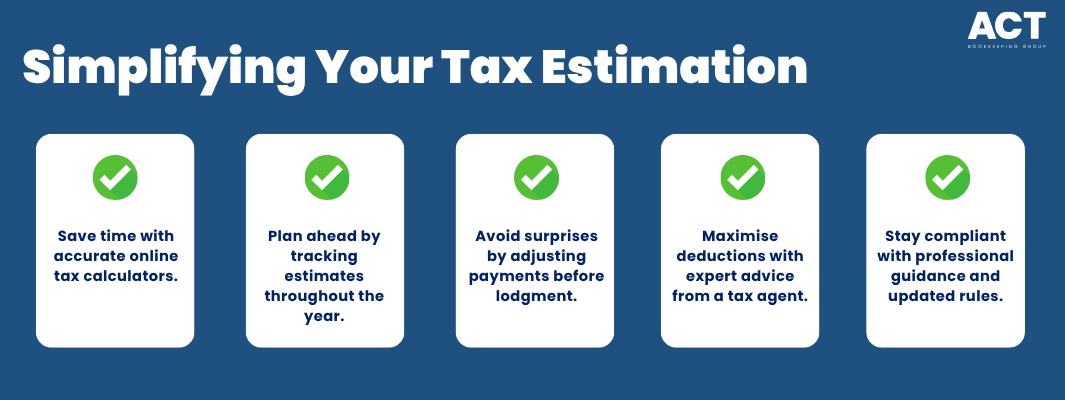

The ATO offers several online tools to help with tax calculations. Their tax return calculator provides estimates based on the information you enter, while the tax refund calculator helps you understand whether you’re entitled to money back.

Using these tools throughout the year, rather than waiting until lodgment time, helps you plan better. You can adjust your payments if needed or set aside funds for any additional amounts you’ll need to pay.

Keep your calculator results and revisit them quarterly.

Working with a Tax Agent

A qualified tax agent brings expertise to help you estimate your tax return accurately. They understand complex rules around deductions, offsets, and special circumstances that might apply to your situation. Tax agents can also help you lodge your tax return and provide advice on tax planning strategies.

We’re more than bookkeeping experts

As part of ACT Tax Group, we offer complete accounting and business advisory services tailored to your needs.

Planning for Your Tax Payments and Refunds

Once you have your estimated tax results, plan how you’ll handle the payment or refund. If you expect to owe money, start setting aside funds now rather than scrambling at lodgment time.

Open a separate account specifically for tax payments. Transfer a percentage of each payment you receive into this account throughout the year. This ensures you have funds available when your tax bill arrives.

Conclusion

Estimating your business tax return doesn’t have to be overwhelming when you follow a systematic approach. By gathering complete financial details, calculating your taxable income accurately, and applying the correct tax rates, you can forecast your tax position with confidence. Using ATO tools and working with professionals makes the process reliable.

Regular estimation throughout the financial year gives you better control over your cash flow and reduces stress. You’ll know whether to expect a refund or prepare for additional payments, allowing you to make informed business decisions.

Ready to take control of your tax planning? Start implementing these estimation techniques today and consider how professional support could enhance your tax outcomes. What steps will you take to improve your tax estimation process for the upcoming financial year?